If you are an operator of trade or business (T:mi), an agricultural/forestry operator, select Manage your tax matters in MyTax. When you start with Manage your tax matters, you can access all your tax affairs. Read more: New in MyTax

Buyer of a flat (housing company) – complete the return and pay the transfer tax

When you buy shares in a housing company and become the owner of a flat, apartment or terraced house, you must pay transfer tax and file the return to report it.

1

File the return

File the transfer tax return in 2 months from signing the contract. If a realtor (= real estate agent) helps you buy, it is the realtor’s responsibility to submit the transfer tax return to the Tax Administration.

- If you buy together with a co-buyer – typically your spouse – both of you must submit a transfer tax return.

- To complete the return, you should have the deed of sale or other contract on hand. You may need the building manager’s certificate as well.

- However, you generally do not have to add very many enclosures. In MyTax, a window will appear that tells you whether an additional enclosure must be attached or whether it is enough if you just complete the tax return.

How to file a transfer tax return in MyTax

The paper-printed form (6012e) can be used by individual taxpayers, general partnerships and limited partnerships. If the paper form is filed, you must enclose a photocopy of the contract.

2

Pay the tax

Pay the transfer tax in 2 months from signing the contract. If a realtor (real estate agent) assists you when you buy the shares, you must pay the tax when you sign the contract.

- If you use MyTax to send the payment, reference numbers and other bank details are automatically transferred to the template for processing by your e-banking service. MyTax calculates the amount of transfer tax.

- If you pay via your personal e-bank instead, you need the bank account number for the Tax Administration and the bank reference number for transfer tax. To get the bank account and reference numbers, you can:

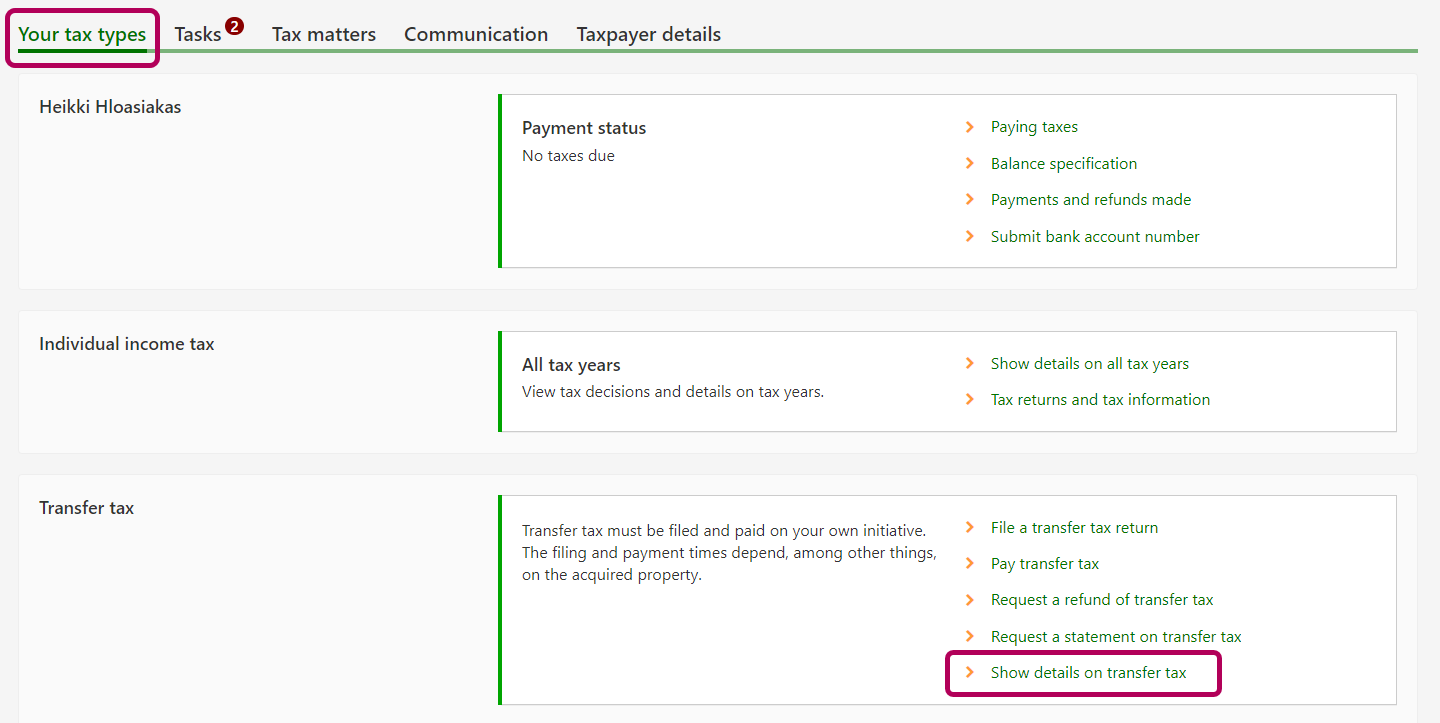

- Check them in MyTax: Click the Your tax types tab on the home page. Go to Payment status and click Paying taxes and payment details.

- Call the service telephone number +35829 497 026 (Payment transactions, limited service available in English, standard call rates)

The amount of tax to pay must have 2 decimal points. After you have made the necessary calculations to arrive at the right tax, round it out to the nearest cent as usual. Example: your calculation result is €345.67890. You must round out the result in order to pay €345.68 as your tax.

If there is more than one buyer – two spouses, for example – each must pay their own share of the transfer tax on a separate bank transfer and enter their personal reference numbers. The amount will be displayed as a paid tax in MyTax on the following business day or the day after that.

Buyers in foreign countries – requesting a bank reference number

3

You receive a certificate of transfer tax

You will receive a certificate on filed and paid transfer tax in MyTax or by post. Normally, after you have filed and paid, the certificate will appear in MyTax in 2 days. Finding the certificate in MyTax. If you file your return on paper, wait for the certificate of transfer tax to become available in MyTax a little later.

If a realtor assists you when you buy the housing-company shares, you get the certificate proving the payment of the transfer tax from the realtor (the estate agent’s office). MyTax does not contain the certificate if the realtor issued it.

4

Make sure that the transfer of title is recorded in your name

You can ask the manager whether the housing company’s information is in the new Property Information System. The National Land Survey maintains this system.

If the housing company’s information is recorded in the new Property Information System, you must submit an application for registration of your ownership to the National Land Survey. Your transfer-tax payment is recorded in the Property Information System automatically, so you do not have to present any certificate to the manager.

If the company’s lists of shares and shareholders are not recorded in the new system, show the building manager the certificate. It proves that you paid the tax. Taxpayers who have submitted the transfer tax return form before 1 November 2019 receive a stamped copy of the submitted return from the Tax Administration, and they can use it as their certificate. Ask the manager about any other documentation they might require for having your name entered in the list of shareholders.

Amount of transfer tax to be paid on a housing-company apartment

Transfer tax is 1,5% of the price (including any other consideration that had been agreed) and the unpaid part of any housing-company loan.

The “debt-free price” (velaton hinta; bostadens skuldfria pris) contains both the price of the flat itself and the part representing the housing-company loan, if any. In other words, transfer tax is collected on the debt-free amount. It is not important whether you pay up the specific part of the housing-company loan when you sign the contract or whether you pay it in small instalments every month.

You can use the transfer tax calculator to get help with your calculations.

Example: Sarah buys a flat for €60,000 (this is the price advertised as “myyntihinta”). There is a loan balance of €20,000 allocated by the housing company to Sarah’s shares. This means that Sarah’s “debt-free price” equals €80,000. The €80,000 is the base for transfer tax. The tax is 1,5% × €80,000 = €1,200. It makes no difference whether Sarah pays off her part of the company loan when buying the flat, or gradually as part of the monthly charge.

Frequently asked questions

After you have filed and paid transfer tax in MyTax, you will receive a certificate of the transfer tax in MyTax. This usually takes about 2 working days. You will also receive a certificate when you have bought your first home.

When the certificate is ready, you can open it through the details on the transfer tax or in the MyTax mailbox. If Your tax types tab does not show transfer tax, please log in to MyTax again. If you have filed your transfer tax return on paper, wait for the certificate of transfer tax to become available in MyTax.

Note: You cannot view the return in MyTax if you have submitted it before November 2019, with the old paper form. Read more: As I remember, I already submitted my transfer tax return. So why can’t I see my payment or transfer-tax form in MyTax?

Do as follows

Log in to MyTax (opens in a new window).

-

Open the tab Your tax types on the home page. Go to the Transfer tax section and click Show details on transfer tax. If Your tax types tab does not show transfer tax, please log in to MyTax again.

-

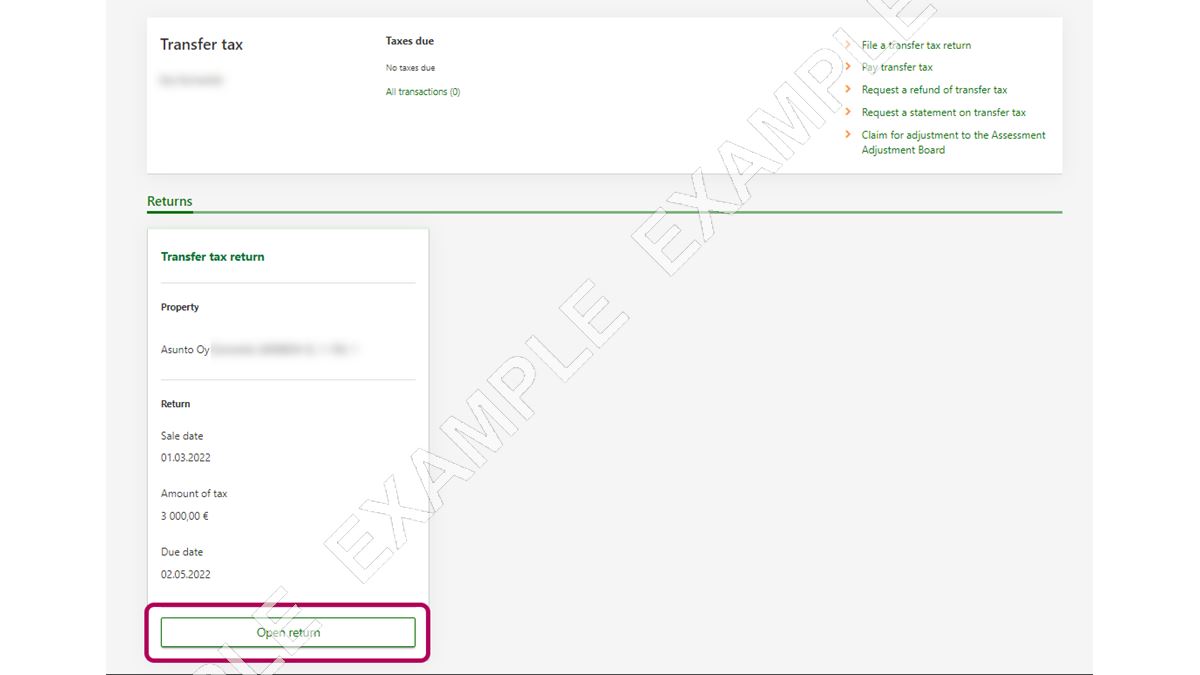

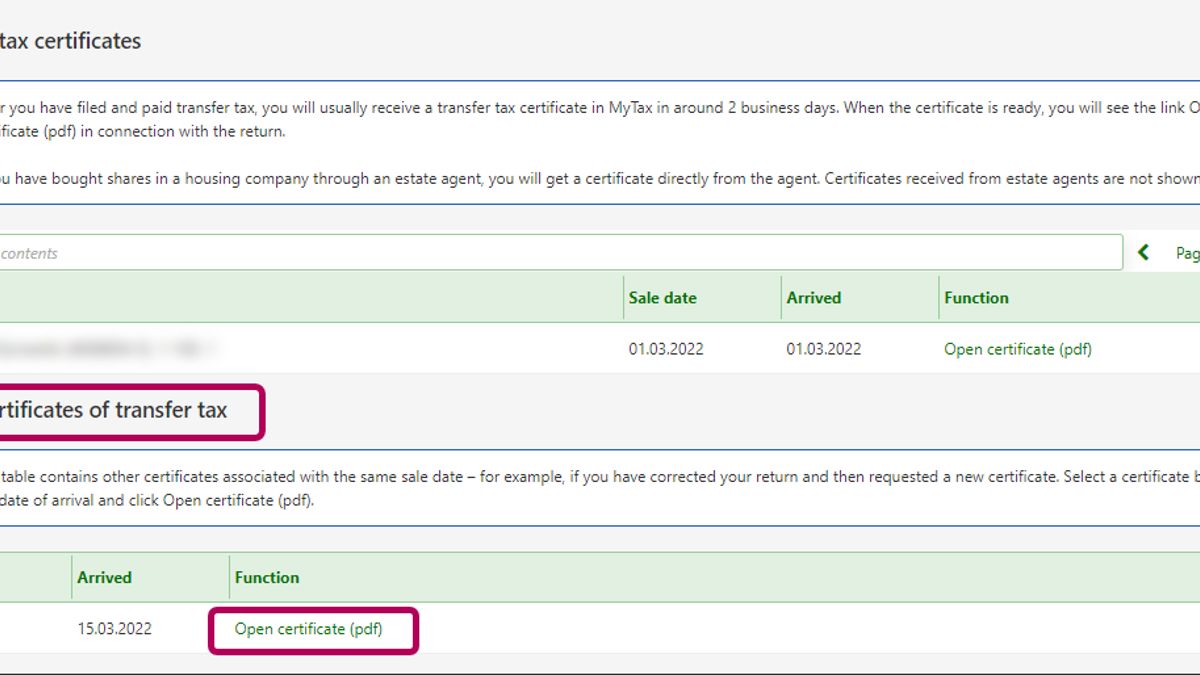

The Transfer tax page includes all the transfer tax returns you have filed. Select the return to which the certificate you need is related. Click the Open return button.

-

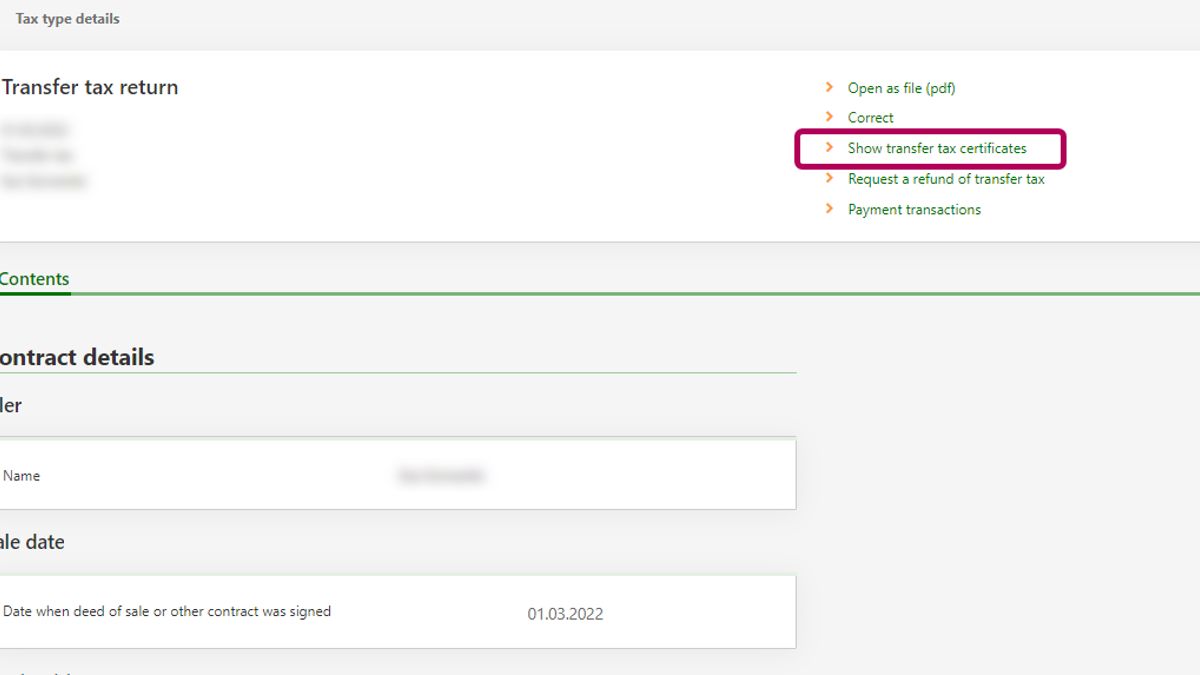

Select the Show transfer tax certificates link at the top of the page

-

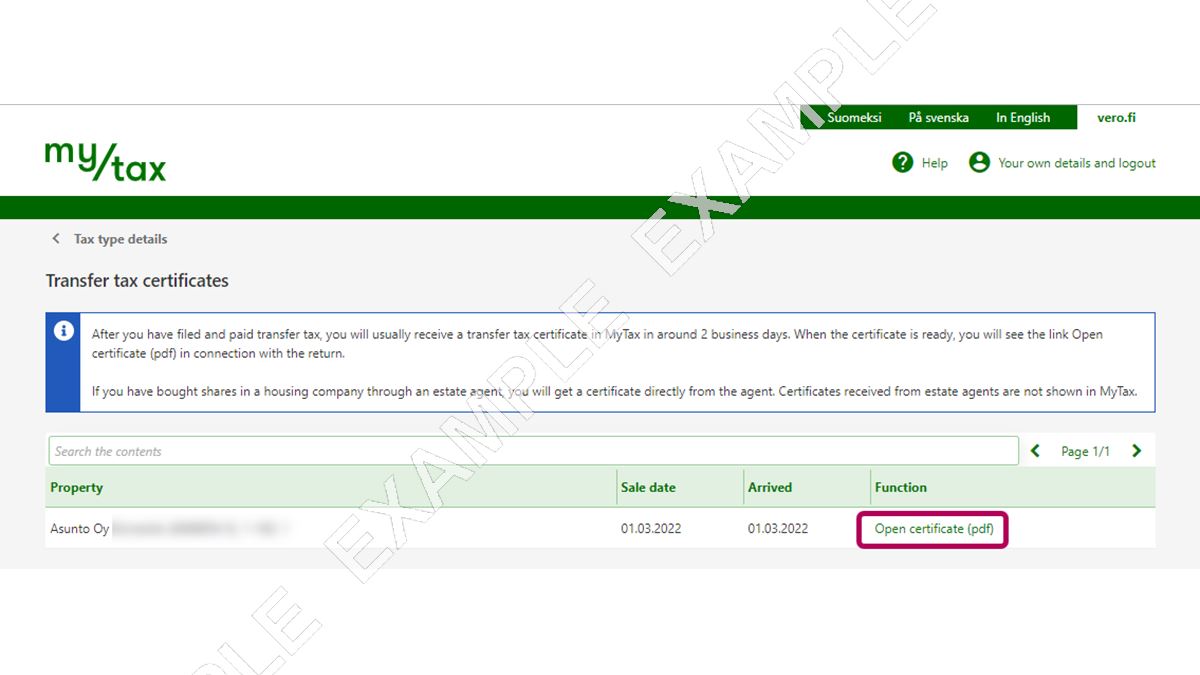

When the certificate is ready, you can open it by clicking the Open certificate (pdf) link. If the certificate is not yet available in MyTax, a notification saying “Certificate has not arrived yet” is displayed.

-

If you have requested a new certificate, after having made corrections for example, you can see the certificate under Other certificates of transfer tax. Select the certificate based on the date of arrival and click Open certificate (pdf).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Alternatively, you can also do as follows

-

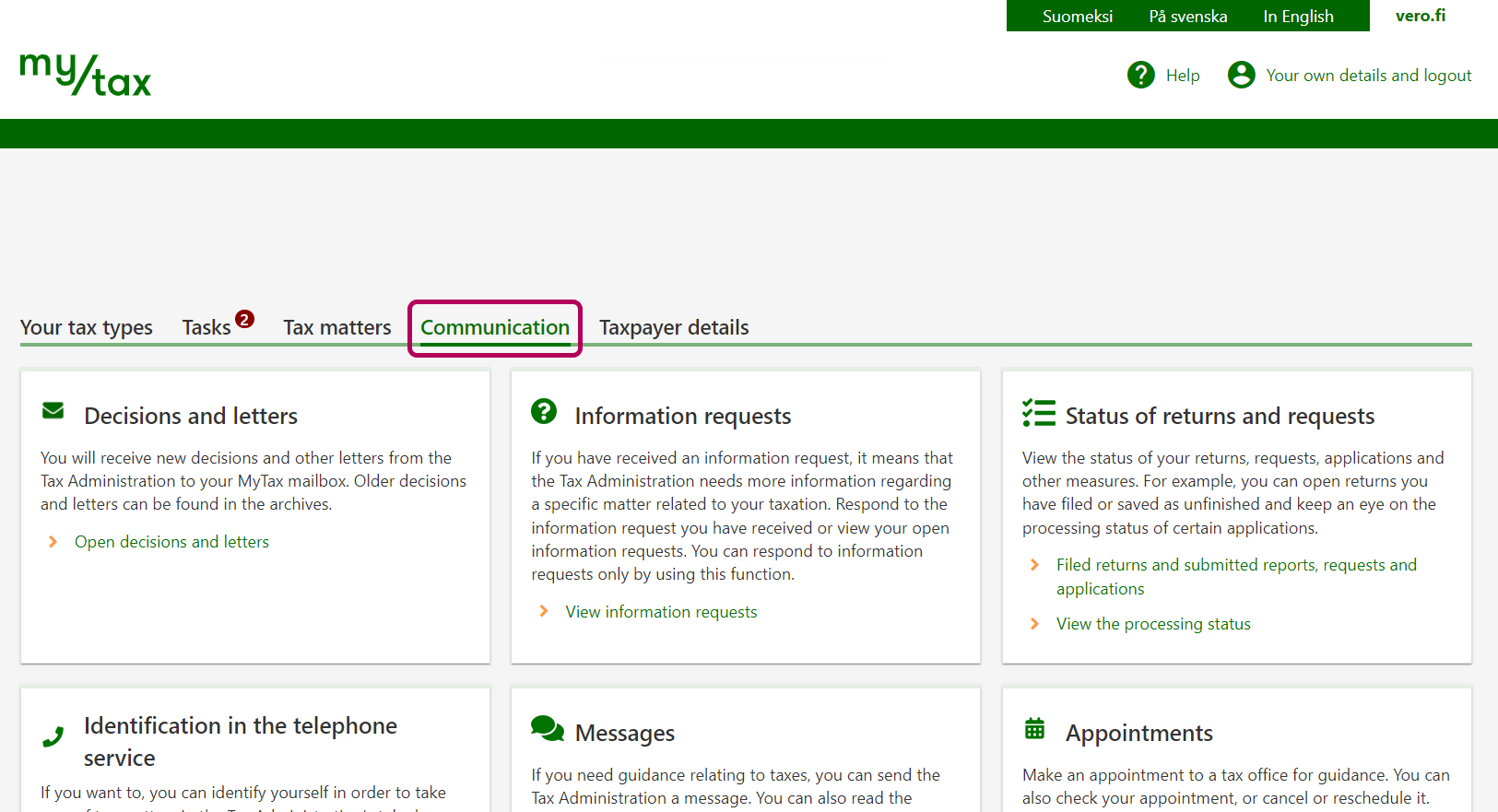

Select the Communication tab.

-

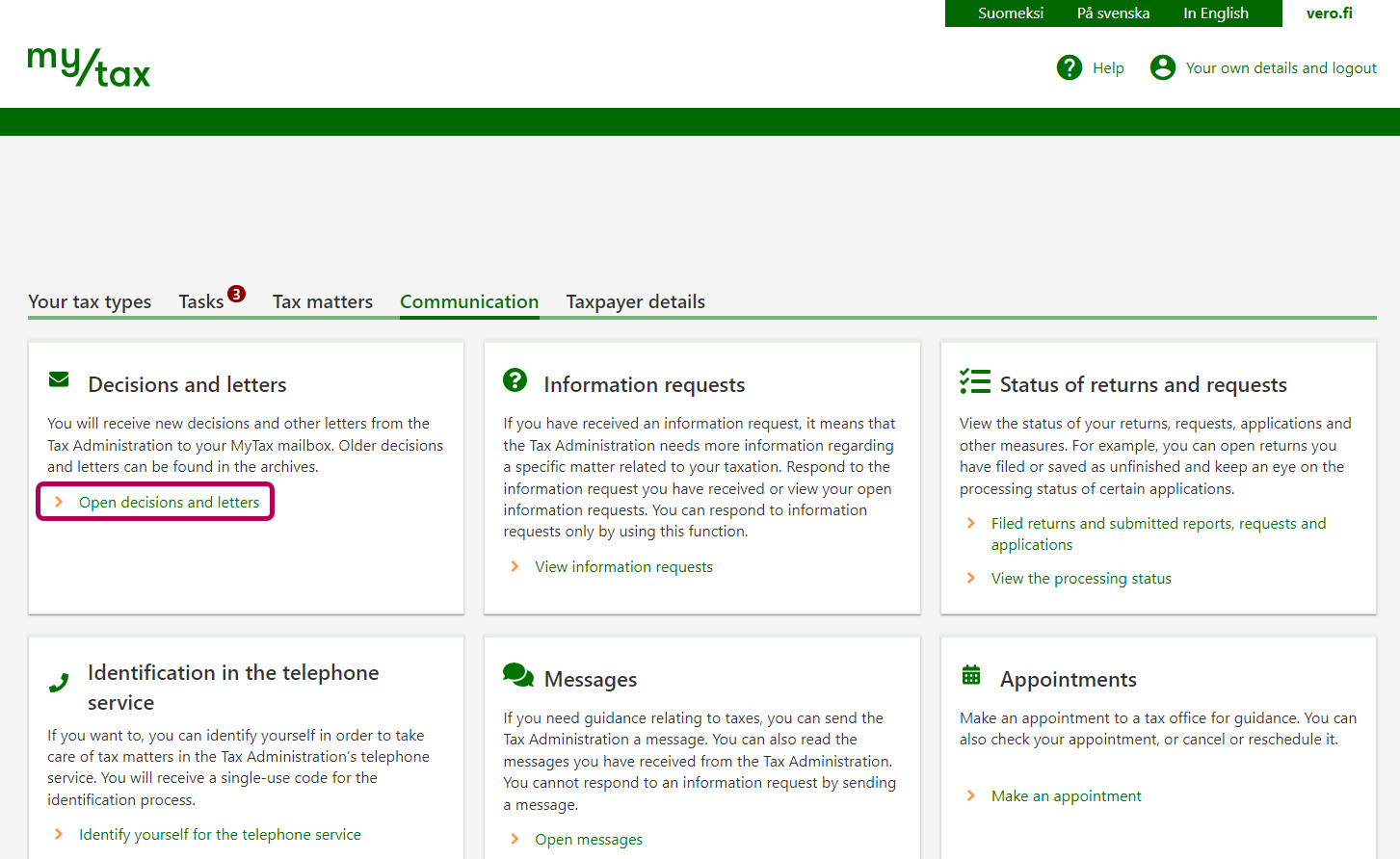

Click the Open decisions and letters link under Decisions and letters.

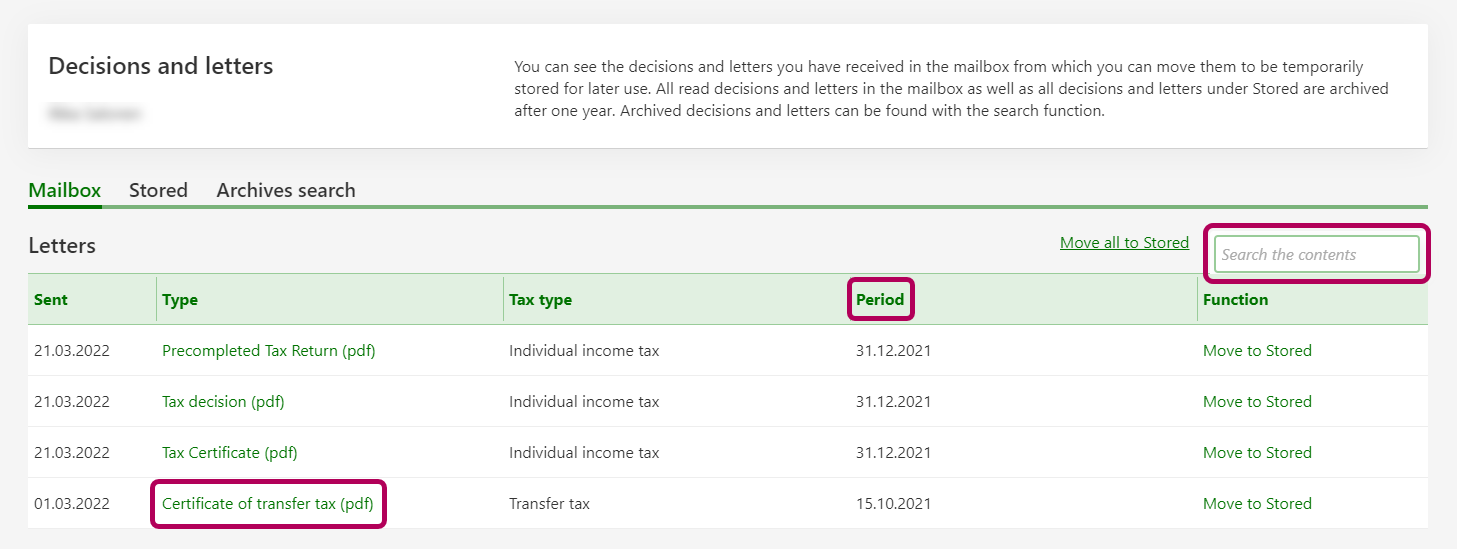

All read certificates in the mailbox as well as all certificates under Stored are archived after one year.

-

If you have received multiple certificates of transfer tax, you can identify them by the sale date. The sale date is shown in the Period column.

If you are looking for a certificate from a specific date, do as follows: Write the date of the sale (e.g. 01.03.2021) in the Search the contents field and press Enter.

{kind=link}

{kind=link}

{kind=link}

Transfer taxation has only been handled in MyTax as of 8 November 2019. In MyTax, you can see:

- Any returns and notices you have submitted in MyTax.

- Any paper transfer tax returns you have submitted after 1 November 2019 on paper forms released at that time or later. In general, there is always a delay before a paper return becomes available for viewing in MyTax.

When you have used a transfer tax return, a certificate of your transfer tax will be stored in MyTax for viewing after both the return and the payment have been recorded in the Tax Administration’s data system. Finding the certificate in MyTax

If the housing-company shares are the type that entitle you to start living in a flat of the housing company, hand the certificate over to the building manager. This enables the building manager to enter your name in the list of shareholders.

If a realtor assists you when you buy the shares in a housing company, you will receive the certificate proving the payment of the transfer tax from the realtor (the estate agent’s office). MyTax does not contain the certificate if the realtor issued it. In the case of “new construction”, if you bought the shares for a newly built flat, you must submit the transfer tax return independently. After you have done that, the certificate will be stored in MyTax for viewing.

Older tax returns

You cannot view the return in MyTax if you submitted it before November 2019, with the old paper form. Please do not re-submit the return. If you need a copy of such a return, i.e. the one with a stamp on, please call the service number on +35829 497 022 (transfer taxes); sometimes the superintendent of a housing company may demand that you show a stamped form.

If a space for parking or storage is part of the contract, remember to pay the transfer tax on it and remember to include the parking or storage in the information you report on the transfer tax return.

If the contract contains a breakdown of the price of the parking or storage space, fill in the specific price information in your transfer tax return.

In general, transfer tax must be paid in 2 months from the date of purchase of shares in a housing company i.e. from signing the contract. If a realtor assists you, transfer tax must be paid immediately when the contract is signed. These deadlines are the same even if there is a clause for redemption in the housing company’s articles of association.

If a third-party buyer comes forward, invoking their rights as a redeemer of the flat you were going to acquire, that buyer must pay the transfer tax and file a tax return on it in two months after redemption. In this case, you will no longer be the buyer and you can ask for refund of any transfer tax you may have paid.

If you submit the transfer tax return late, the Tax Administration may impose a late-filing penalty or punitive tax increase. If you do not pay your transfer tax on time, you must pay interest. Read more about transfer tax return or payments that are overdue.

If you need to make corrections to the information you submitted, submit a replacement. You can do this in MyTax or send a paper transfer tax return that replaces your original return. In this case, you must not only correct the mistakes but also complete the other spaces on the form again.

How to make corrections to a transfer tax return in MyTax

If you submit a replacement on paper, remember to tick the “Replacement transfer tax return” box on the first page.

Note: if you submit the replacement past the deadline date for transfer taxes, the Tax Administration may impose a late-filing penalty or punitive tax increase.

If by this time, you already paid the transfer tax, look up the specific guide for correcting payment and the submitted return.

First, if you encounter any cases-in-process for which ownership is still unclear because the people who have the shares have not proven to you that transfer tax is paid, it is the housing company’s responsibility to verify the current ownership situation of the apartment.

If a residential apartment was bought in 2023 or later, the shareholder’s transfer tax is not expired, i.e. does not fall under the statute of limitations. In this case, the shareholder must show the housing-company manager a certificate proving that transfer tax was paid (if they have not yet shown it). After you receive the Tax Administration’s certificate concerning paid transfer tax, you can enter the shareholder’s name in the company’s list of shareholders. In the same way, based on the Tax Administration’s certificate, you can have the shareholder’s name recorded in the Residential and Commercial Property Information System.

For residential apartments bought in 2022 or earlier, the transfer tax normally falls under the statute of limitations. However, if the shareholder bought “newly constructed property”, as defined by tax rules, the statute of limitations may still not have affected their transfer tax. In the case of “newly constructed property”, the apartment’s date of transfer to the new owner determines the due date for transfer tax payment. Read more about dates of expiration (in Finnish or Swedish).

If an apartment’s transfer tax falls under the statute of limitations, it is enough if you just refer to the contract of sale (or other similar document) to update the company’s list of shareholders with the current ownership information. The Tax Administration issues no certificates to prove that a certain transfer tax falls under the statute of limitations. You can submit information on new owners to the Residential and Commercial Property Information System when you have the company’s list of transfers recorded there.

Key terms: