When you log in to MyTax, your tax-related letters will change from paper to electronic form automatically. Read more about the changes.

Instructions for filing and paying transfer tax

You can file the transfer tax in MyTax or complete and submit a paper form. Limited-liability companies and other corporate entities must submit transfer tax returns electronically in MyTax.

You can pay the transfer tax in MyTax or in your e-bank. You need the Tax Administration’s bank account number and a bank reference number for transfer tax. You can get the reference number in MyTax or phone our service number to ask for it.

The category of the purchased property affects the deadlines for filing and payment:

- Apartment and other spaces related to shares in a housing company

- Newly constructed property

- First home

- Real estate unit (house)

- Building, such as allotment cottage

- Corporate stock

- Shares based on time-sharing, shares in a golf-course company

The category of the purchased property affects the deadlines for filing and payment

Guidance for real estate agents and securities dealers

Instructions for paying transfer tax if the buyer is from a foreign country

Frequently asked questions

To pay transfer tax, you will need your personal reference number for transfer tax in order that the payment could be allocated to the correct tax.

If you pay the transfer tax in MyTax, the reference number and other payment details are automatically pre-populated on the payment template in your e-bank service.

If you pay in your e-bank, you can check the reference number and the Tax Administration’s bank account number

- in MyTax: Select the tab Your tax types on the home page. Go to Payment status and click Paying taxes and payment details.

- by calling our service number 029 497 026 (payment transactions, limited service available in English, standard call rates).

Check the illustrated guidance in section 5: How to pay taxes in MyTax.

Can a real estate agent or a bank get my reference number?

If you buy a share in a housing company through a real estate agent, you must pay the transfer tax when you sign the contract. You should preferably check the reference number before the contract is signed.

The real estate agent or the bank can also ask for the reference number and the Tax Administration’s bank account number on your behalf by telephone. When making the phone call, the real estate agent or the bank officer must have your personal ID or Business ID at hand.

If the software that the real estate agent or bank uses has an interface to the Tax Administration, they can request your reference number for transfer tax through the interface in real time.

When you pay transfer tax, use your dedicated reference number for transfer tax. When you do so, the payment will be immediately used to pay your transfer tax. You can check the reference number in MyTax.

When paying transfer tax, you can also use the general reference number for taxes but in that case your payment will not be used for the transfer tax until on the due date. If you have other taxes falling due before that, then the payment will be used to pay them first.

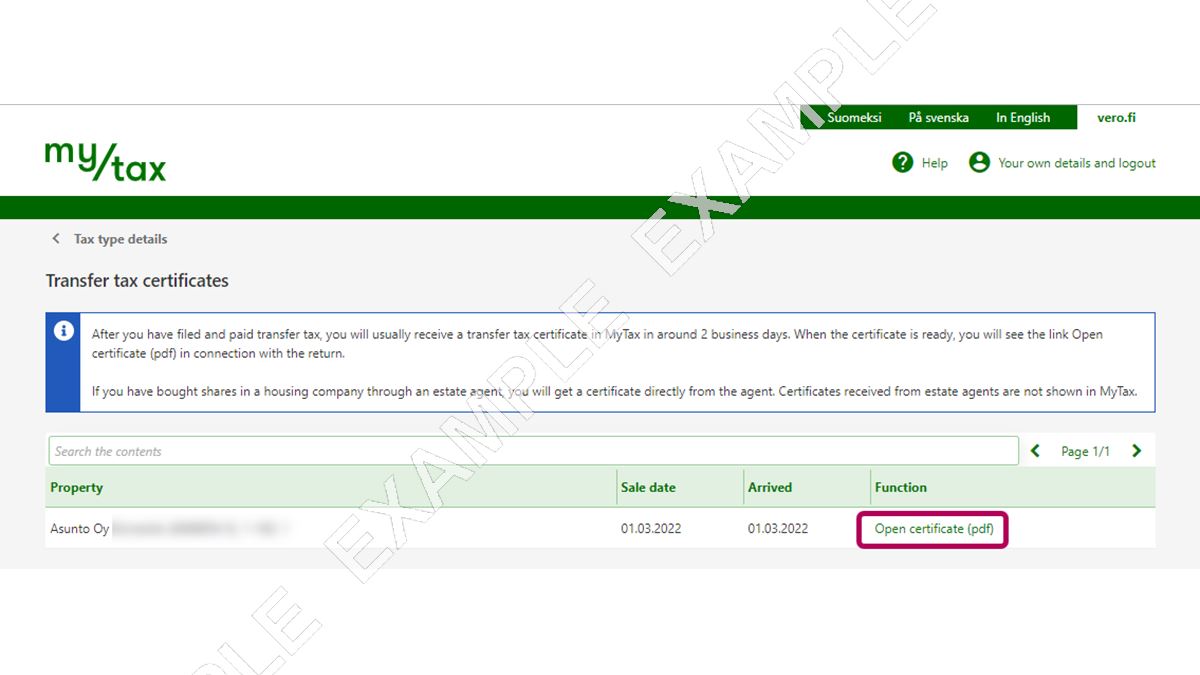

After you have filed and paid transfer tax in MyTax, you will receive a certificate of the transfer tax in MyTax. This usually takes about 2 working days. You will also receive a certificate when you have bought your first home.

When the certificate is ready, you can open it through the details on the transfer tax or in the MyTax mailbox. If Your tax types tab does not show transfer tax, please log in to MyTax again. If you have filed your transfer tax return on paper, wait for the certificate of transfer tax to become available in MyTax.

Note: You cannot view the return in MyTax if you have submitted it before November 2019, with the old paper form. Read more: As I remember, I already submitted my transfer tax return. So why can’t I see my payment or transfer-tax form in MyTax?

Do as follows

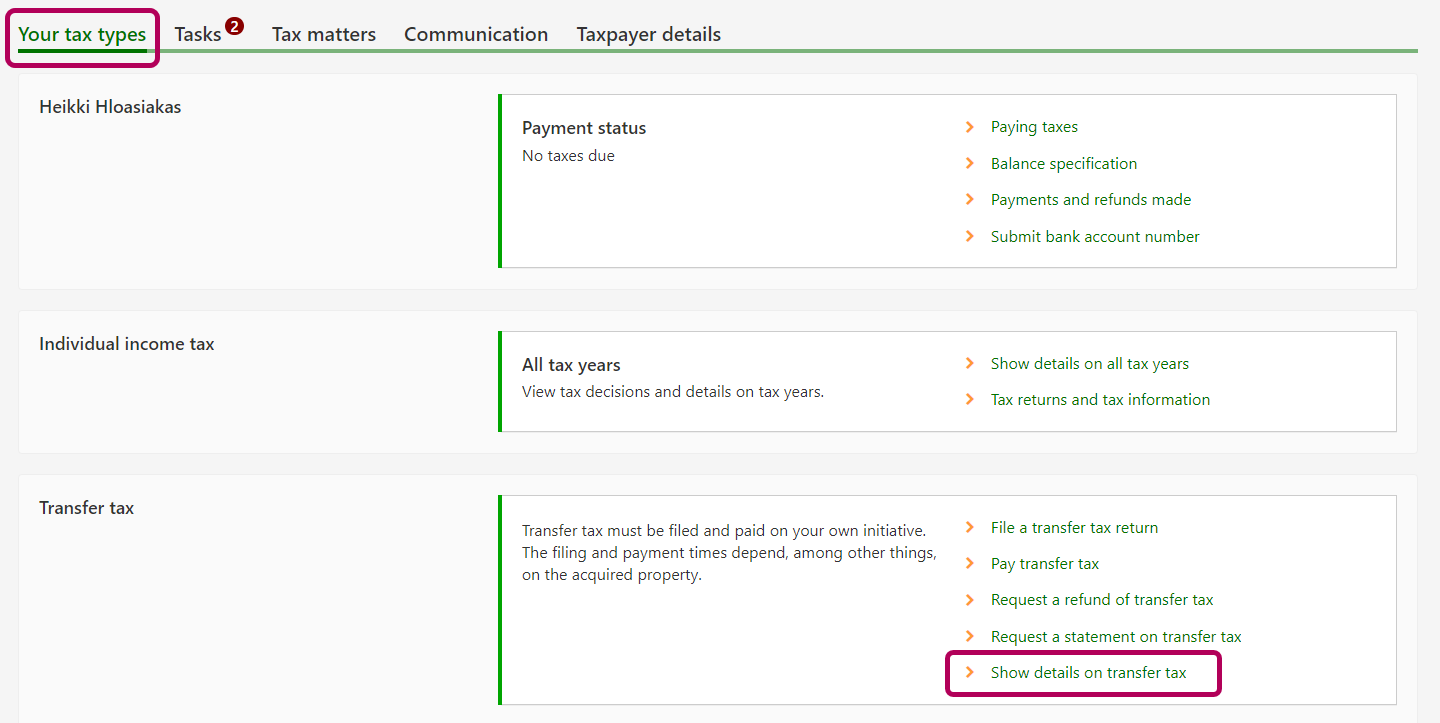

Log in to MyTax (opens in a new window).

-

Open the tab Your tax types on the home page. Go to the Transfer tax section and click Show details on transfer tax. If Your tax types tab does not show transfer tax, please log in to MyTax again.

-

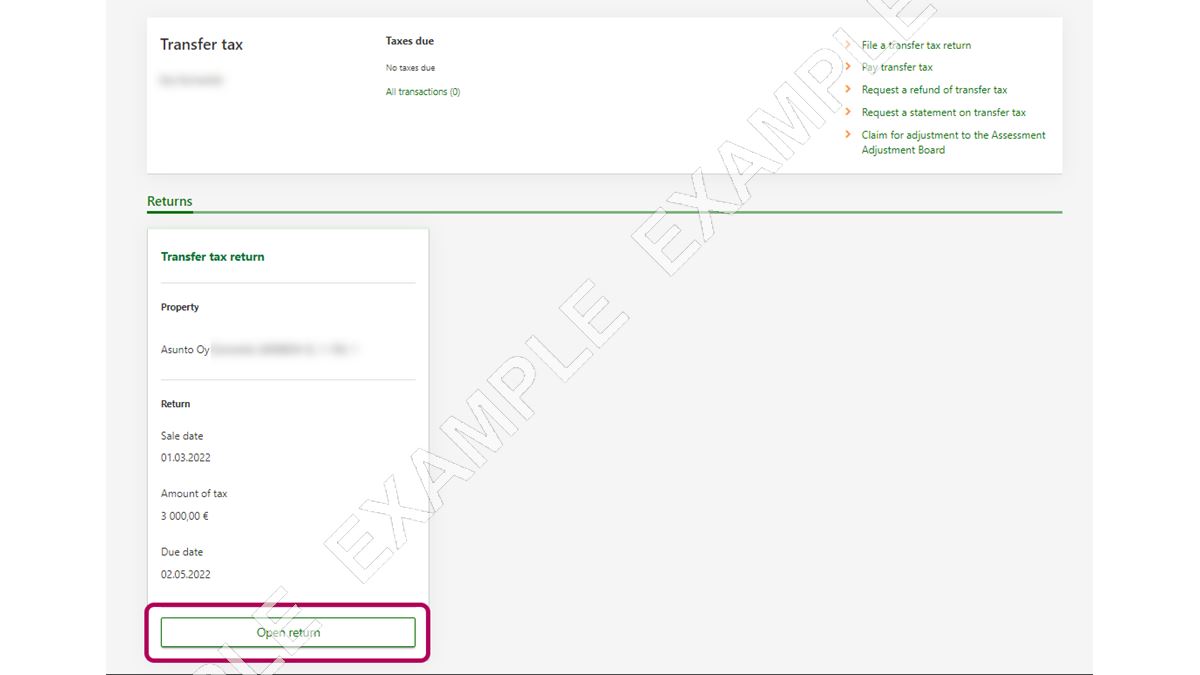

The Transfer tax page includes all the transfer tax returns you have filed. Select the return to which the certificate you need is related. Click the Open return button.

-

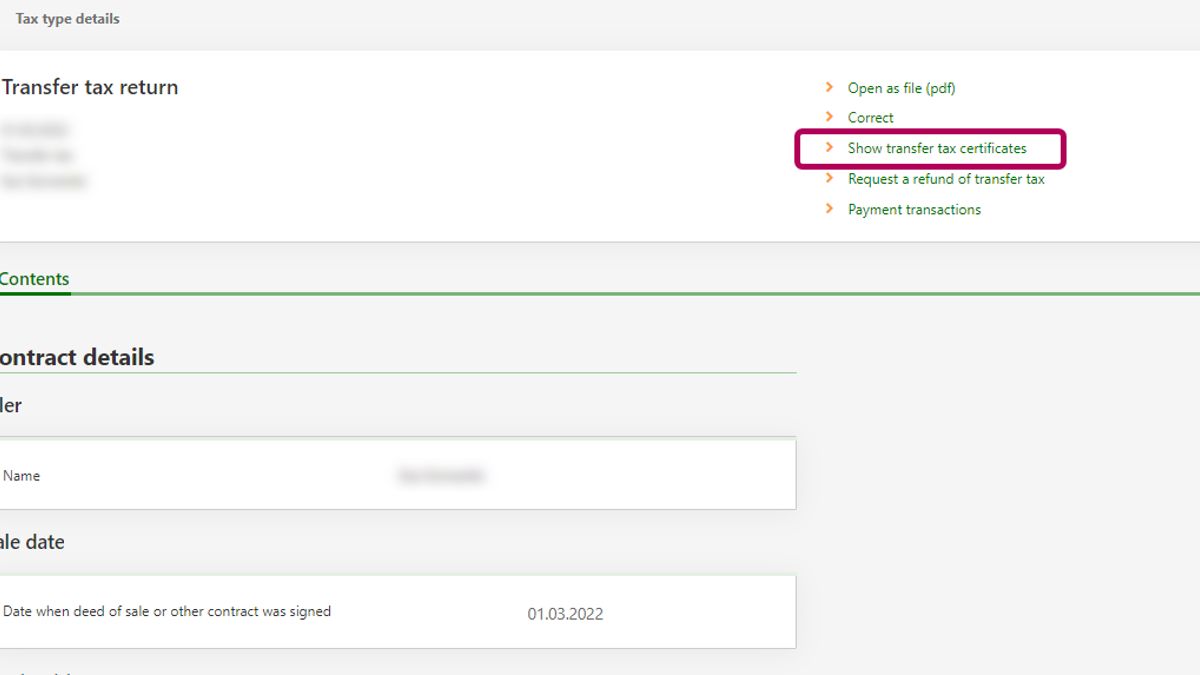

Select the Show transfer tax certificates link at the top of the page

-

When the certificate is ready, you can open it by clicking the Open certificate (pdf) link. If the certificate is not yet available in MyTax, a notification saying “Certificate has not arrived yet” is displayed.

-

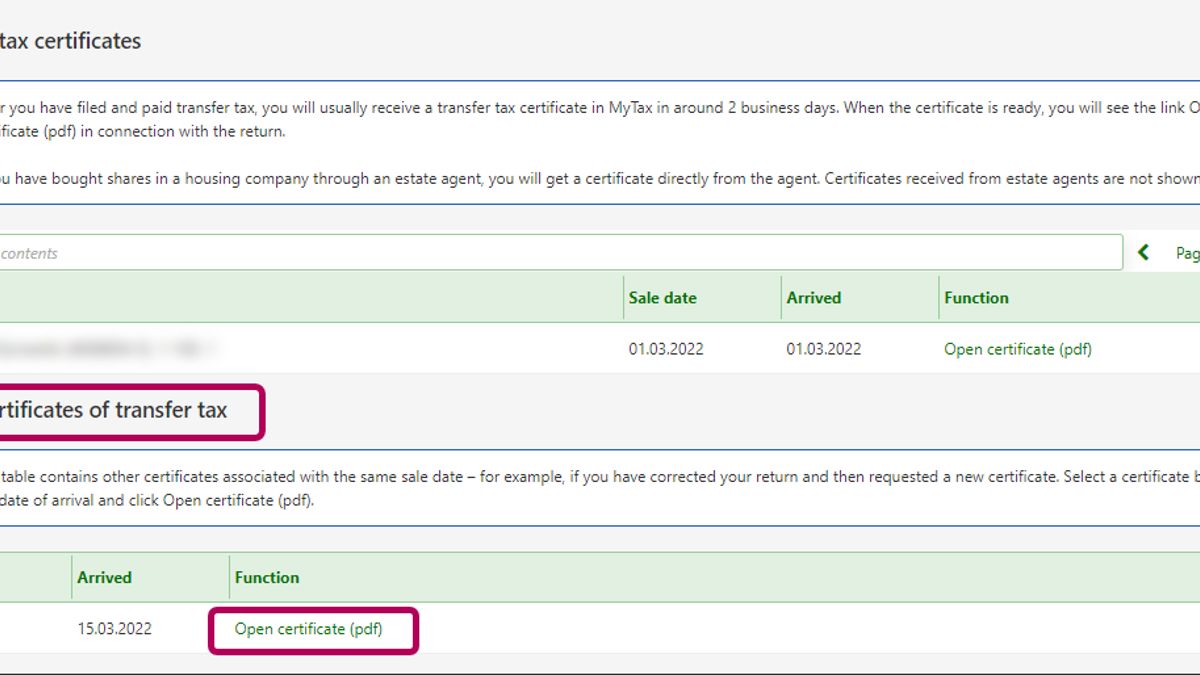

If you have requested a new certificate, after having made corrections for example, you can see the certificate under Other certificates of transfer tax. Select the certificate based on the date of arrival and click Open certificate (pdf).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Alternatively, you can also do as follows

-

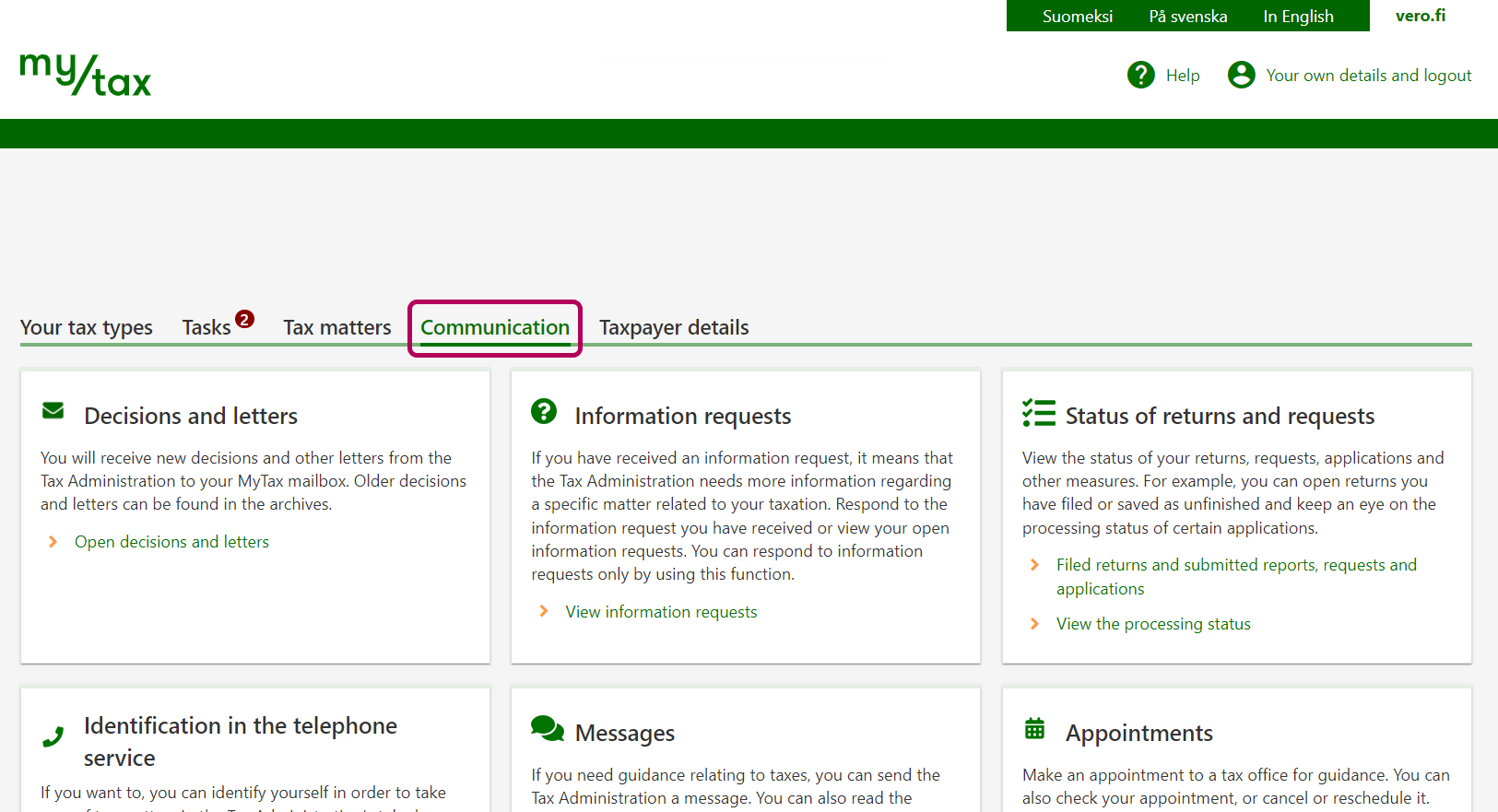

Select the Communication tab.

-

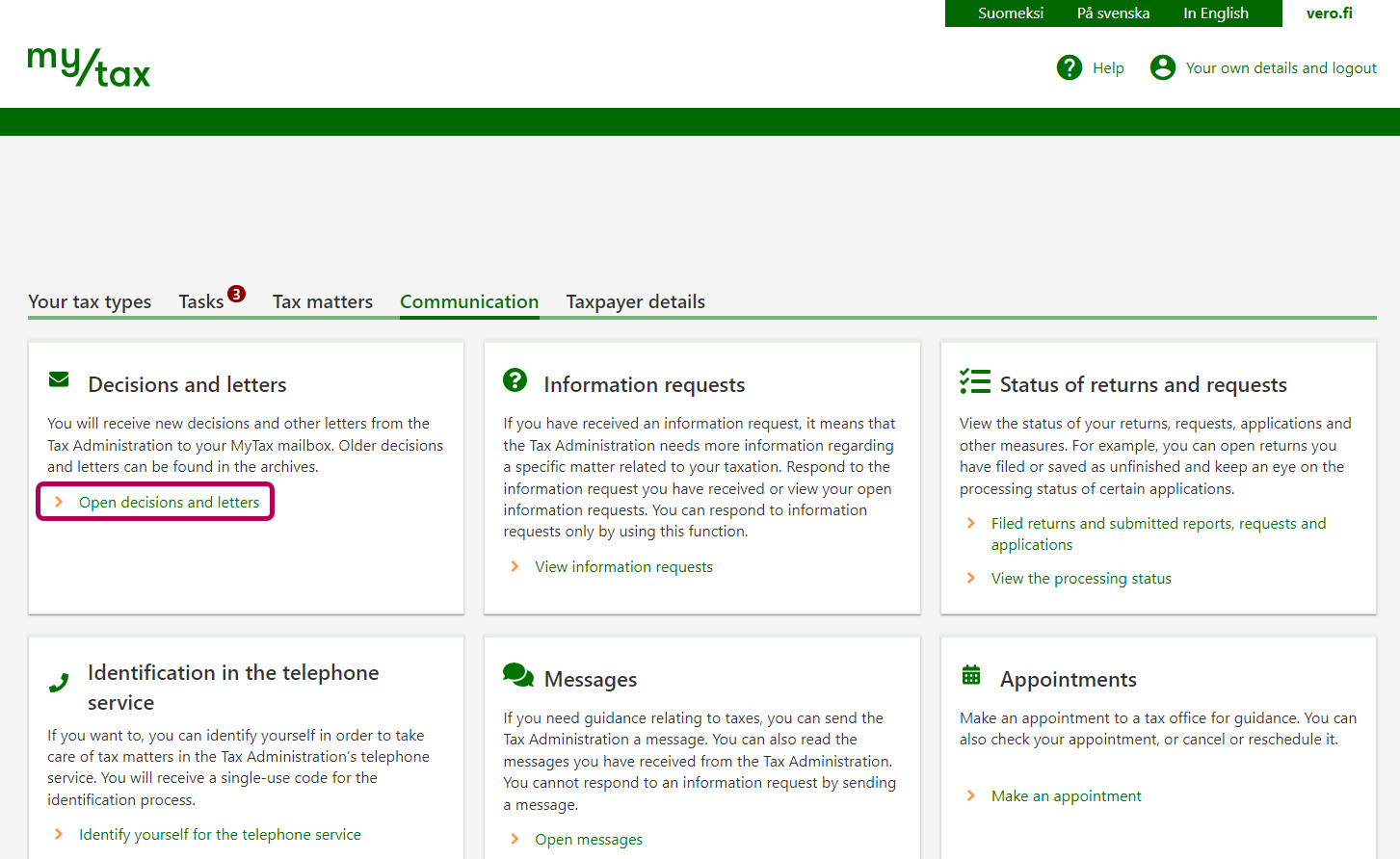

Click the Open decisions and letters link under Decisions and letters.

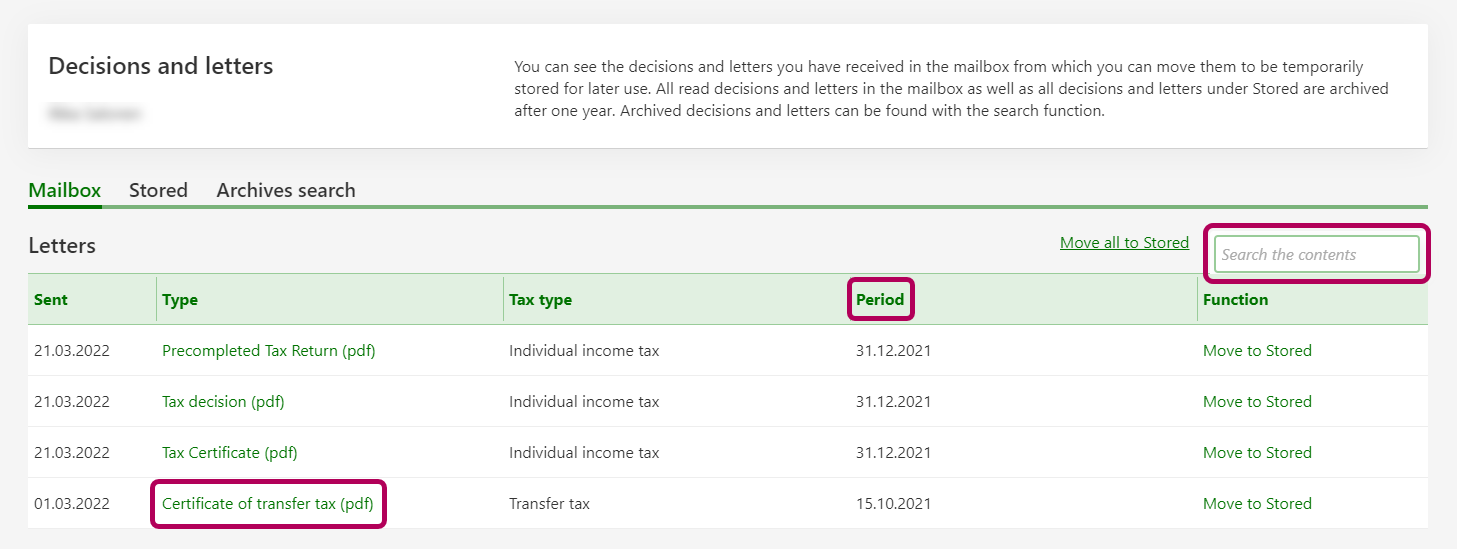

All read certificates in the mailbox as well as all certificates under Stored are archived after one year.

-

If you have received multiple certificates of transfer tax, you can identify them by the sale date. The sale date is shown in the Period column.

If you are looking for a certificate from a specific date, do as follows: Write the date of the sale (e.g. 01.03.2021) in the Search the contents field and press Enter.

{kind=link}

{kind=link}

{kind=link}

Transfer taxation has only been handled in MyTax as of 8 November 2019. In MyTax, you can see:

- Any returns and notices you have submitted in MyTax.

- Any paper transfer tax returns you have submitted after 1 November 2019 on paper forms released at that time or later. In general, there is always a delay before a paper return becomes available for viewing in MyTax.

When you have used a transfer tax return, a certificate of your transfer tax will be stored in MyTax for viewing after both the return and the payment have been recorded in the Tax Administration’s data system. Finding the certificate in MyTax

If the housing-company shares are the type that entitle you to start living in a flat of the housing company, hand the certificate over to the building manager. This enables the building manager to enter your name in the list of shareholders.

If a realtor assists you when you buy the shares in a housing company, you will receive the certificate proving the payment of the transfer tax from the realtor (the estate agent’s office). MyTax does not contain the certificate if the realtor issued it. In the case of “new construction”, if you bought the shares for a newly built flat, you must submit the transfer tax return independently. After you have done that, the certificate will be stored in MyTax for viewing.

Older tax returns

You cannot view the return in MyTax if you submitted it before November 2019, with the old paper form. Please do not re-submit the return. If you need a copy of such a return, i.e. the one with a stamp on, please call the service number on +35829 497 022 (transfer taxes); sometimes the superintendent of a housing company may demand that you show a stamped form.

If you need to make corrections to the information you submitted, submit a replacement. You can do this in MyTax or send a paper transfer tax return that replaces your original return. In this case, you must not only correct the mistakes but also complete the other spaces on the form again.

How to make corrections to a transfer tax return in MyTax

If you submit a replacement on paper, remember to tick the “Replacement transfer tax return” box on the first page.

Note: if you submit the replacement past the deadline date for transfer taxes, the Tax Administration may impose a late-filing penalty or punitive tax increase.

If by this time, you already paid the transfer tax, look up the specific guide for correcting payment and the submitted return.

The purchase of property may be conducted digitally so that all parties sign the deed of sale-and-purchase digitally at different times. In these cases, the contract enters into effect when the final signature is added. As a result, you should write the date of the final signature into the transfer tax return's line "date when the deed of sale or other transfer agreement was signed".

In accordance with the provisions of the amended act on transfer tax, the date of the final signature also determines which rate of transfer tax is applied, and whether the first-time homebuyer’s transfer tax exemption can be applied.

The date of contract is when the agreement is finalised. This means the moment when the digital signature of the last person who is expected to sign the deed has done so. You need to write that date into the transfer tax return's line “date when the deed of sale or other contract is signed”.

Because the Property Transaction Service creates an electronic application for registration automatically, and because the deadline for transfer tax filing and payment is the time when registration is requested, the buyer needs to both have filed the transfer tax return and paid the tax by the date of contract, i.e. the time when the agreement is finalised.

Yes, you must file a transfer tax return even if the company considers the change in the form of activity to be partly or fully exempt from tax as described in § 24 of the act on income tax (Tuloverolaki 1535/1992 (TVL)).

If the company considers the transfer to be fully exempt from tax, state on the transfer tax return that the compensation is €0. Enclose a separate, free-form account of the assets that the company considers to be exempt from tax. If the transfer is partly exempt from tax, report the portion subject to tax on the transfer tax return and the portion exempt from tax in a separate free-form enclosure. This applies to both securities and real estate. The company must file a transfer tax return in MyTax.

If the income tax assessment shows that the company’s judgement about the tax exemption was incorrect, the company must correct the details by submitting a corrected return (a replacement transfer tax return). In addition, the company may have to pay penalty fees.

Amendments to the act on transfer tax entered into force on 1 January 2024, and the transfer tax treatment of business transfers also changed. The amended act is applied retroactively on business transfers conducted on or after 9 October 2023.

A business transfer is an arrangement where a limited liability company transfers either all its assets, liabilities and balance-sheet reserves or those related to a specific business entity to another limited liability company that will continue the transferred business operations. In exchange, the transferring company will be given shares of the recipient company. The recipient company is legally obligated to continue the business operations that were transferred to them.

A business transfer is exempt from transfer tax if it fulfils the requirements for tax exemption in income tax assessment defined in § 52 d of the act on the taxation of business income (Laki elinkeinotulon verottamisesta 360/1968).

If the agreement on business transfer was signed on or after 9 October 2023

- A real estate unit or security can be transferred to an existing corporation that continues the operations such that the transfer is exempt from transfer tax. Previously, the tax exemption only applied to newly established companies.

- The recipient company must file the transfer tax return on the transfer. The agreement on the business transfer must be added as an attachment to the return.

- The recipient company does not need to submit a separate application for transfer tax exemption.

If the agreement on business transfer was signed before 9 October 2023

- In order for the transfer to be exempt from transfer tax, the real estate unit or security must have been transferred to a company that has been newly established for the purpose of continuing the business operations.

- The recipient company must submit an application for transfer tax exemption. The application can be submitted in MyTax.

- If the company receives a decision on transfer tax exemption before the due date for paying the tax, the company does not need to file a transfer tax return or pay the tax.

- If the company has not submitted an application for tax exemption before the due date for transfer tax payment, the company must file a transfer tax return and pay the tax. However, the company can later request a refund of the transfer tax they have paid.

Read more about the requirements for transfer tax exemption (available in Finnish and Swedish, link to Finnish)

Check the due dates for filing and paying transfer tax for each property type

The act on transfer tax has been amended to include a temporary tax exemption provision, effective as of 1 January 2024.

This provision concerns the incorporation of certain municipal facilities used for health care and wellbeing services into companies. The tax exemption is applicable to transfers conducted on or after 9 October 2023. These transfers are exempt from tax if they meet the conditions for tax exemption defined in § 43 a of the act on transfer tax (Varainsiirtoverolaki 931/1996). However, a transfer tax return must be filed, with the deed of transfer regarding the assets in kind as an attachment.

The transfer is exempt from transfer tax if:

- The incorporation takes place by the end of 2030.

- The transferor is a municipality or joint municipal authority alone or together with another municipality or joint municipal authority.

- The limited liability company that receives the transferred real estate is owned by the municipality or joint municipal authority alone or together with another municipality or joint municipal authority. The company may already exist, or it may be established for this purpose.

- No cash consideration is involved in the transfer. Instead, the municipality or joint municipal authority receives shares of the recipient company.

- The real estate unit to be transferred was mainly used by the municipality or joint municipal authority for social welfare, health care or rescue operations on 31 December 2022. In addition to the real estate unit, a part of the real estate unit or shares in the real estate company may also be transferred exempt from tax, if the requirements listed here are fulfilled.

- The transferred real estate unit had been rented out to the wellbeing services county as described in the legislation on the social welfare and health care reform.