If your transfer tax return or your payment is overdue

If your transfer tax return or your payment is overdue, the Tax Administration will impose penalty charges. In the same way, a penalty charge is also imposed for late filing of a request for registration of title.

Look up the deadlines for transfer tax return filing and payments.

The return is not submitted by its deadline date: Late fee or a punitive tax increase

If you file the transfer tax return late, you must pay a late-filing penalty or an increased tax. The amount you must pay depends on how many days the tax return is late.

If you file less than 60 days late (or exactly 60 days late), you must pay a late-filing penalty. We will send a specific decision letter on the penalty charge with instructions for payment.

The amounts to be imposed are:

- €50 for individuals and estates of a deceased person

- €100 for other taxpayers and for third parties that have the obligation to file transfer tax (such as limited-liability companies).

For example, if a self-employed individual works as a realtor and fails to submit the return on time, the amount would be €50. However, if the realtor is a limited-liability company, it would be €100.

Please note that a penalty charge would be imposed also in cases where a taxpayer has already filed their transfer tax return, and later sends a new return to replace the first one, max. 60 days late, and the effect of the corrected transfer-tax calculation is that the tax goes up.

Example: On 1 September, Jarmo acquired the shares of a housing company that entitle him to apartment number 1. The price was €200,000. Jarmo files his transfer tax return in MyTax by 1 November, not missing the deadline. However, in December, Jarmo becomes aware that he did not include the loan balance of €150,000 in the transfer tax return. The base of transfer tax is the price and the balance of the housing-company loan combined. Jarmo sends a new return to replace his original transfer tax return as soon as he can, i.e. within 60 days from the original deadline. The Tax Administration will impose a late filing penalty of €50.

You will have to pay a punitive tax increase if

- You have not filed a transfer tax return

- You file the transfer tax return more than 60 days late

- You receive a Tax Administration’s request for additional information, and make corrections to your original transfer tax return after that

Please note that a penalty charge would also be imposed in cases where a taxpayer has already filed their transfer tax return, and later sends a new return to replace the first one, max. 60 days late, and the effect of the new return is that the transfer tax grows higher.

You may also have to pay a punitive tax increase if the transfer tax return is incomplete or inaccurate.

The punitive tax increase is usually 10%. The increase may also be lower (2% or 5%) or higher (15–50%). How much your tax is increased depends on the type of negligence.

However, the punitive tax increase is always at least

- €75 for individuals and estates of a deceased person

- €150 for other taxpayers and for third parties that are accountable for transfer tax

Before tax increase is imposed, you will receive a letter from the Tax Administration informing you of it and asking about your response.

You make an overdue payment: late-payment interest

If you do not pay your transfer tax on time, you must pay interest. In 2024, the interest rate is 11%.

It is your responsibility to add the interest, on your initiative, to the transfer tax that you are paying after its due date. If you pay in MyTax, the interest is included in the sum automatically. Use the late-payment calculator to work out the exact amount.

Another situation where you must pay interest is if you applied for registration of your title or lease in time but you paid the transfer tax late.

Note: If you have any questions about payments, call our service number 029 497 026 (local network charge/mobile charge). If you have any other questions about transfer tax, please contact the Finnish Tax Administration’s transfer tax service number on 029 497 022 (local network charge/mobile charge).

Registration request is submitted late: a punitive tax increase may be imposed

If you have not applied for the registration of your title to a house, a real estate unit or lease in time, you will have to pay an increase.

Transfer tax is increased by 20% for each six-month period that begins. The counting of time towards the six-month periods begins the next day when the deadline date for registration has passed. However, although you might be late by many six-month periods in a row, the transfer tax will only be increased up to a maximum of 100%.

Because the increase is legally imposed due to your lateness with registration, and is not related to your taxes, the increase must be paid even if you had filed and paid transfer tax on time.

This is how you need to report and pay the increase

You can take care of the filing and payment of the increase in MyTax.

-

If you already filed your transfer tax return, now you must make corrections to it, adding the information about the punitive increase.

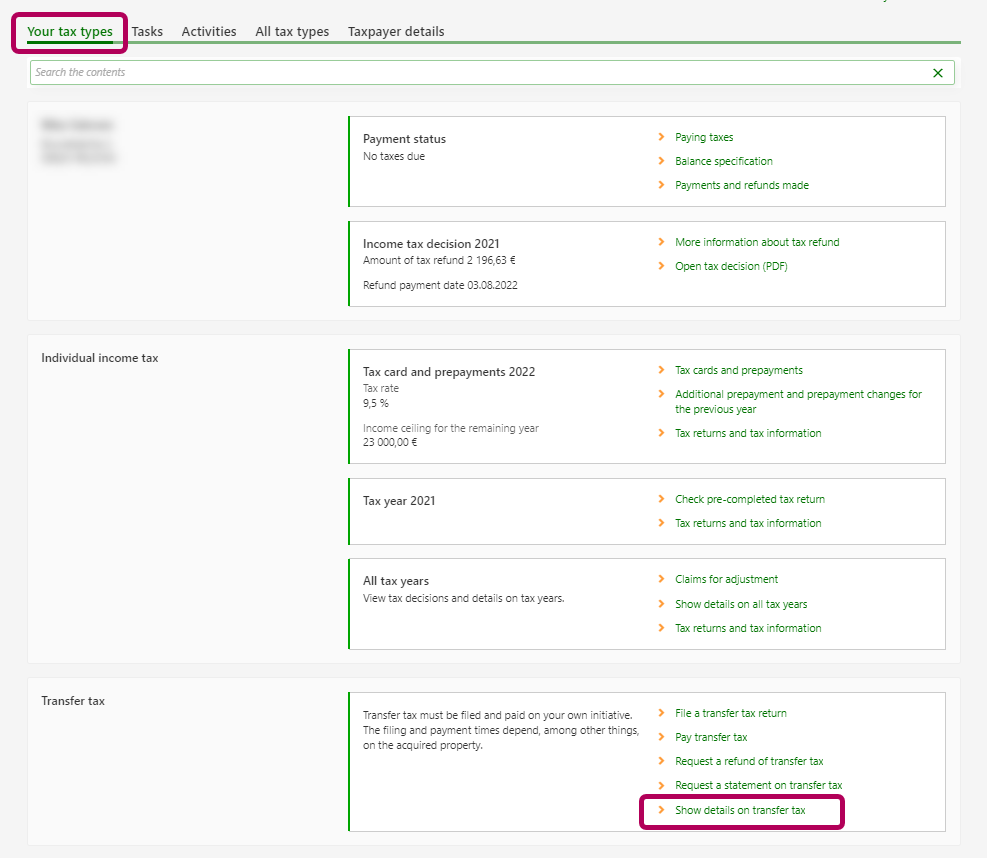

To do this, go to Transfer tax on the home page and select Show details of transfer tax.

-

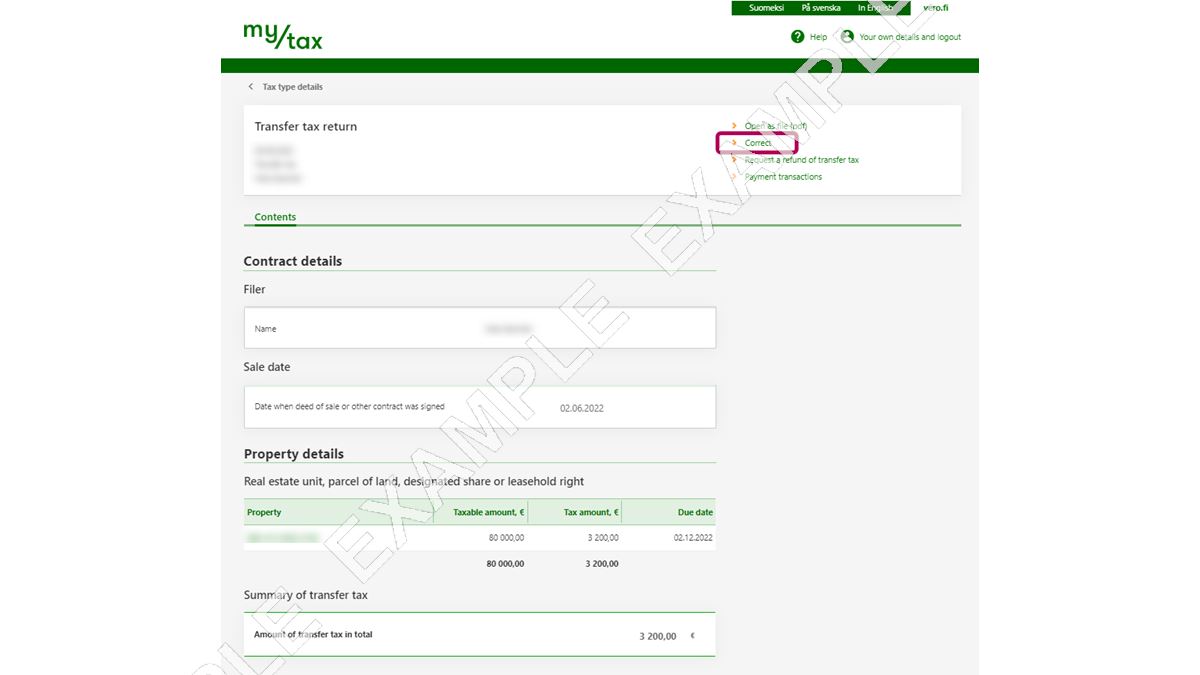

Select the transfer tax return you want to correct. Open the transfer tax return.

Click Correct on the top of the page.

-

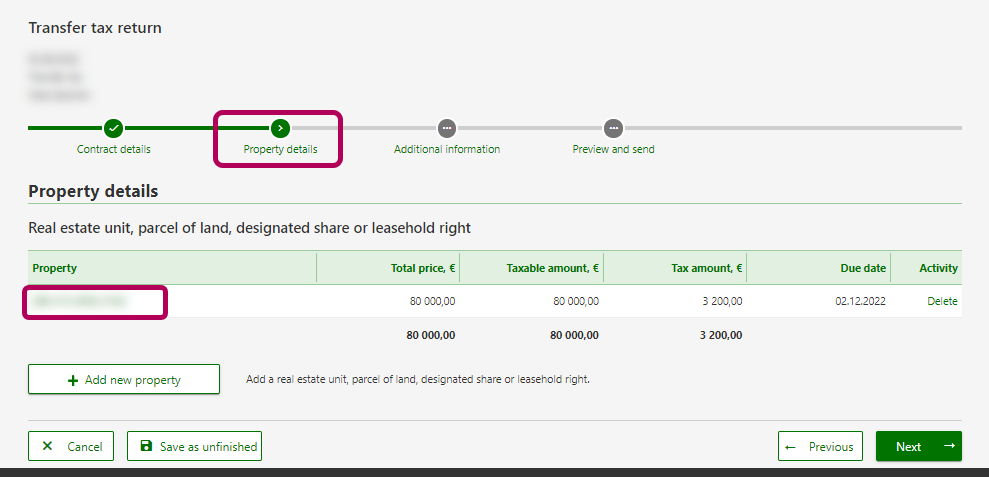

The Property details stage is where you must submit information on an imposed increase. Select the asset or property item you need to make corrections to.

-

Scroll down to Requesting title registration and registration of leasehold rights. Answer “No” to “Have you requested title registration or registration of leasehold rights within 6 months of signing the deed of sale or other contract?”

Fill in the amount increased in euros, or alternatively as a percentage of your transfer tax. If you choose the latter, MyTax will calculate the amount for you.

-

If you are unable to handle your taxes in MyTax, fill in the paper Transfer tax return, section 10, to file the punitive increase. Enter you personal bank reference number for transfer taxes when you pay the increased amount and any unpaid transfer tax.

Example: Liisa bought a house for €100,000 on 3 October 2022. She filed the transfer tax return and paid the transfer tax on time. However, she forgot to apply for the registration of title to the property. She should have submitted the application by 3 April 2023, but she did not do so until 11 October 2023. Because of this, Liisa must pay a punitive tax increase.

In Liisa’s case, the increase is calculated as follows:

Because the house was bought in 2022, the transfer tax rate on real estate is 4%. The transfer tax on Liisa’s house is 4% × €100,000 = €4,000.

The punitive tax increase is 20% for the 6-month period starting 4 April 2023 and another 20% for the 6-month period starting 4 October 2023. This amounts to 40% × €4,000 = €1,600.

Liisa corrects her transfer tax return in MyTax: she adds the amount of the increase and pays an additional €1,600 in transfer tax.

{kind=link}

{kind=link}

{kind=link}

{kind=link}