Studies on the shadow economy

Payment arrangements during the COVID-19 pandemic did not prevent bankruptcies – costs rose high

28.1.2026

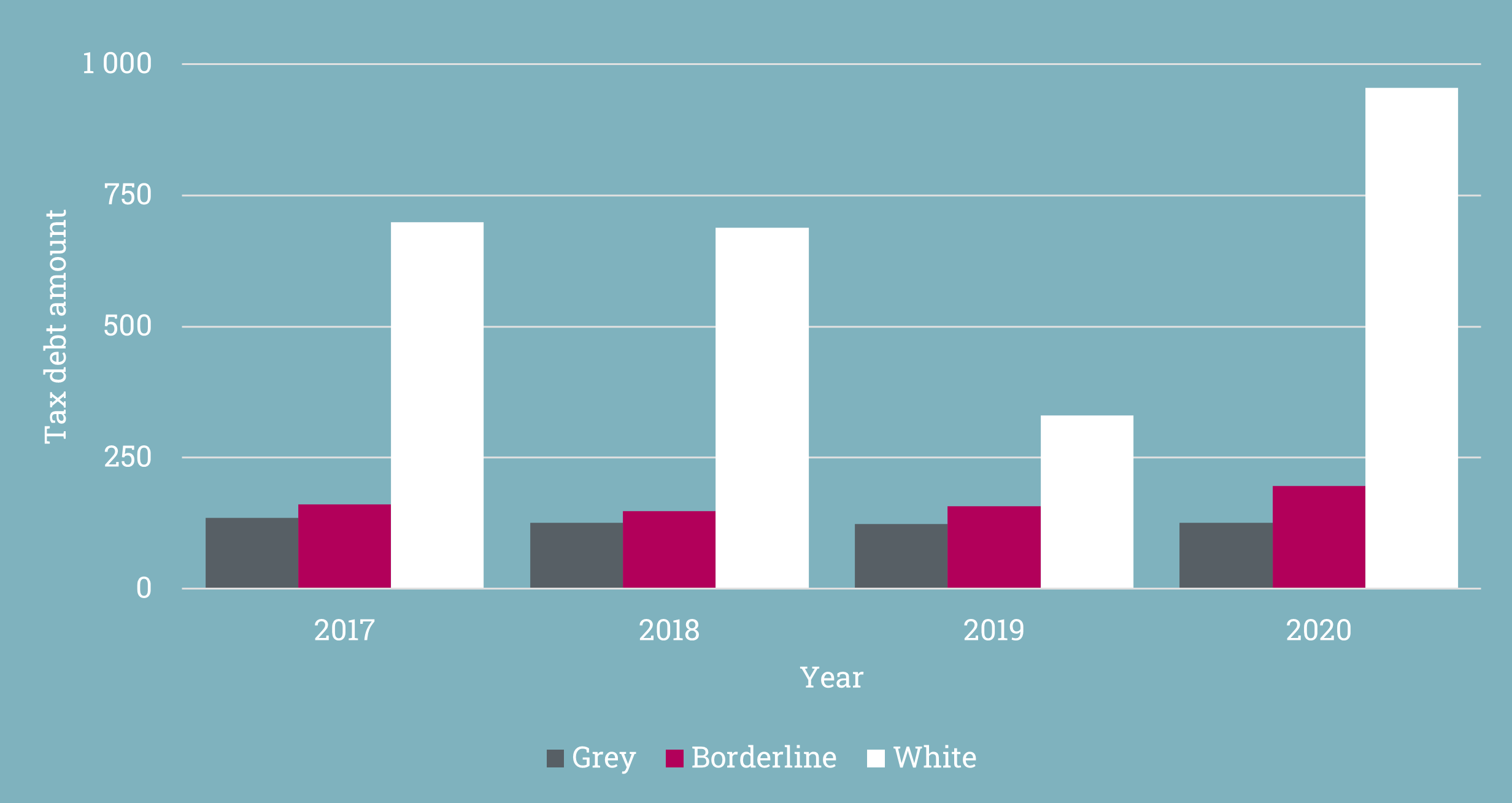

Due to restrictions imposed during the COVID-19 pandemic, the Finnish Tax Administration granted companies payment arrangements on more favourable terms. According to a recent report, companies that were granted payment arrangements with eased terms had a higher risk of grey economy activity than other companies. Additionally, several financially solvent companies took advantage of payment arrangements as a means of financing due to low interest rates. Payment arrangements that were granted exceptionally without official discretion resulted in an estimated loss of EUR 33 million in tax revenue.

Discounted payment arrangements were intended to ease the situation of companies

Restrictions imposed during the COVID-19 pandemic, which began in 2020, caused companies to face financial difficulties. Efforts were made to alleviate the situation of companies by, for example, granting payment arrangements under more favourable terms for a few months between 2020 and 2021. The interest calculated for a tax subject to a payment arrangement was also temporarily lowered. In 2020, companies could also apply for a refund of value added tax already paid.

According to a new report by the Grey Economy Information Unit, the key financial indicators of companies that had been granted a discounted payment arrangement were, on average, weaker than those of other companies. In particular, the wholesale and retail industry and the accommodation and food service industry were overrepresented among companies that had been granted a payment arrangement.

Due to a low rate of late-payment interest on taxes, a discounted payment arrangement created an incentive for some financially solvent companies to use a payment arrangement as a means of financing. In addition to companies facing payment difficulties, many companies with a high turnover and good return on equity also applied for a payment arrangement, paying their obligations ahead of schedule.

Actors with a risk of grey economy activity actively applied for payment arrangements

As getting a payment arrangement has temporarily been easier, some actors in the grey economy may have had an incentive to apply for a payment arrangement in order to remain in the prepayment register and outside the tax debt register. This has allowed them to continue operations and, for example, to apply for some subsidies granted during the COVID-19 pandemic. The report found that companies with a high risk of grey economy activity applied for a discounted payment arrangement more actively than other companies. Additionally, at least 124 companies classified as companies involved in the shadow economy during a tax audit had received a discounted payment arrangement.

No effect on the number of bankruptcies, but significant loss of tax revenue

Companies that applied for a discounted payment arrangement were more likely than other companies to declare bankruptcy. The discounted payment arrangement option postponed bankruptcies in the short term but ultimately did not prevent them. Companies with the highest risk for grey economy activity declared bankruptcy more often than low-risk companies.

As the circumstances were exceptional, a company’s financial situation and its ability to meet the obligations included in the payment arrangement were not assessed as a precondition for a payment arrangement. It is estimated that the absence of official discretion resulted in a loss of EUR 33 million in tax revenue. During any future crises, efforts should therefore be made to maintain some sort of discretionary mechanism and to target support measures more precisely.

Read the full report in Finnish (PDF 942 kB)

Only one in five limited liability companies report their loss of equity to the Finnish Trade Register

17.11.2025

According to a recent report, only around 20 per cent of limited liability companies with negative equity in three consecutive years (2021–2023) had submitted the statutory register entry to the Trade Register. Failure to report this data distorts the view of the financial conditions for business operations and impairs their transparency.

The Limited Liability Companies Act requires that if the company has negative equity, the board of directors must at once make a register entry to the Finnish Trade Register. According to a report by the Grey Economy Information Unit, more than 12,000 limited liability companies continue their operations year after year despite having negative equity.

Neglecting the register entry increases grey economy risk

The magnitude of the grey economy risk for companies was assessed using a machine learning model. The results were clear: the companies that made a register entry were more likely to be in low-risk groups, while those that neglected the entry were more often in high-risk groups.

Why is submitting the registry entry important?

The equity of a limited liability company is a buffer that protects the company from financial drawbacks and serves as evidence of its solvency to outsiders.

When a company's equity is negative, its liabilities outweigh its assets. The registration of the loss of equity is an important part of the transparency of the company’s financial situation. The information about loss of equity serves as a warning sign for parties such as the company’s creditors and contracting partners.

In the worst-case scenario, the financial imbalance may result in the company’s permanent insolvency. If a company continues its operations despite its insolvency while at the same time deliberately impairing its creditors’ status, the activity can be considered dishonesty by a debtor. The risk of fraudulent or inaccurate filing of tax returns to the detriment of creditors may also increase.

How could the situation be improved?

The report shows that there are shortcomings in the registration of loss of equity. There is a need to more actively inform micro-enterprises and small enterprises in particular about the importance of registering the loss of equity. Failure to register may expose the persons responsible for the company to legal and financial risks.

Supervision by the authorities could also be developed, for example, by identifying companies at risk of involvement in the grey economy that have not made the register entry even before they go bankrupt. Provisions on the exchange of information between the public authorities should be reviewed, for example, to enable the transmission of data from the Tax Administration to the Trade Register authorities. Effective supervision of the financial situation of limited liability companies would require submitting the financial statements of limited liability companies electronically and in a structured format to the parties that need them.

20.10.2025 | Increase in tax debts and bankruptcies – targeted monitoring is necessary for combating the grey economy

Increase in tax debts and bankruptcies – targeted monitoring is necessary for combating the grey economy

20.10.2025

Limited liability companies that have been declared bankrupt involve significant risks of the grey economy. For example, three out of four bankrupt companies that had been subject to a tax audit were classified as grey economy operators, and an equal proportion was forwarded for consideration to pursue a criminal complaint. Shortcomings in tax returns and indications of the wind-down process on the verge of bankruptcy are key warning signs of the grey economy. A recent study by the Grey Economy Information Unit covering the period 2022–2023 examined over 4,000 companies that had been declared bankrupt and compared them with a reference group of companies that had continued their operations.

Risk of the grey economy emphasised in bankrupt companies

The study indicates that bankrupt companies are considerably more susceptible to grey economy activities than the companies in the reference group. Although the bankrupt companies do not significantly differ from the other company stock in terms of their background characteristics, they exhibit a higher-than-average number of features indicative of involvement in the grey economy. Three out of four bankrupt companies that had been subject to a tax audit were classified as grey economy operators, and an equal proportion was forwarded for consideration to pursue a criminal complaint. The model predicting grey economy activity also confirmed observations made in non-audited bankrupt companies: more than half of the bankrupt companies ranked in the categories indicating the highest risk of the grey economy, compared to one fifth of the reference group companies. Around eight per cent of the bankrupt companies exhibited signs of the wind-down process of a company on the verge of bankruptcy. These cases involved an exceptionally high risk of the grey economy and required special attention from the public authorities.

Tax debts predict difficulties

In the bankrupt companies, there was a significant increase in tax debt in relation to turnover before bankruptcy. One year before the bankruptcy, around half of the companies had tax debt exceeding five per cent of their turnover; by the year of bankruptcy, this was the case with most of the companies. In the reference companies, the corresponding share was considerably smaller. The accumulation of tax debts and payment arrangements was often connected to bankruptcy petitions by the Tax Administration. Three out of four bankruptcies expired due to a shortage of funds.

“Even a minor tax debt may increase the future risk of bankruptcy unless the accumulation of debt can be effectively halted. The risk of bankruptcy is imminent at the latest when the tax debt in relation to turnover exceeds five per cent. Indeed, the findings of this study indicate that this can be considered a kind of threshold for survival,” summarises Janne Marttinen, Director, Grey Economy Information Unit.

Grouping of companies exposed risk groups

In the study, the bankrupt companies were grouped into six clusters based on their lifespan and financial data. Of the companies with a long lifespan, the most high-risk group consisted of companies that had missing tax return data for the year prior to bankruptcy. An increased risk of grey economy activities, criminal offences and acquisition of a company on the verge of bankruptcy was detected in these companies. Shortcomings in taxation data were also observed in the companies with a short lifespan.

Public receivership is a tool for investigating economic crime

Public receivership is a procedure supervised by the Bankruptcy Ombudsman, which involves continuing the bankruptcy through government funds when the estate’s assets are insufficient for liquidation measures. This procedure aims to combat economic crime and the grey economy, especially in cases that would otherwise expire due to a lack of assets. Public receivership can be used to enforce criminal and damages liabilities, to impose business prohibitions and to demand the reversal of legal proceedings for the bankruptcy estate.

The transfer to the public receivership procedure requires both insufficiency of the estate as well as a genuine need or some other special reason for the receivership.

“In 2024, 51 bankruptcy estates were transferred to public receivership, and by the end of August 2025, the number of cases pending was nearly 500. Public receivership has succeeded in enforcing criminal liabilities and accumulating funds for estates without means through legal and civilian proceedings to cover central government costs and to distribute the funds among creditors. Public receivership procedures regularly involve delivering a verdict on a debtor’s crimes. The shares of distribution allocated among creditors in 2024 amounted to more than EUR 1 million in bankruptcy estates transferred to the public receivership procedure,” says the Office of the Bankruptcy Ombudsman.

Current situation of bankruptcies – increase in debtor’s offences of dishonesty

During 2025, the number of bankruptcies has continued to increase compared to the previous year, and there has also been growth in the number of requests for investigations related to economic crimes. For example, the number of offences involving dishonesty by a debtor is the highest it has been during the ten years that prevention statistics have been compiled. In recent years, the proportion of debtor’s offences of dishonesty of all initiated bankruptcies has been approximately 20 per cent – the share has been slightly growing.

It will take years to curb the ongoing increase in bankruptcies and investigate the related economic crimes. Effective cooperation between public authorities promotes the investigation efforts, and in this context, the resources available in pre-trial investigations and the prosecution and court system play a key role. As estate administrators play a key role in identifying offences related to bankruptcies and in bringing the cases to pre-trial investigations, attention should be paid to the financing of their investigation efforts. Only a fraction of bankruptcy estates without means can be transferred to public receivership.

Read the full report in Finnish (PDF 0,99 MB)

6.10.2025 | Licence conditions and supervision used to tackle the grey economy in the transport sector

The transport licence system is a key tool in the efforts to combat the grey economy. Despite this, there are shortcomings in reliability requirements for nearly one in three licence holders, and there is still room for improvement, especially in the taxi sector. In addition to this, over 10 per cent of companies in the taxi sector continue to be in the highest grey economy risk category. These are some of the facts that emerge from the recent report of the Grey Economy Information Unit of the Tax Administration.

One in three licence holders did not meet reliability requirements that were set in the study

According to the report, around one in five transport licence holders did not meet the financial reliability requirements based on the company’s data. When also including the details of responsible persons and affiliated companies, this proportion increased to nearly one in three. The examination concerned taxi, goods and passenger transport licences.

The reliability assessment is based on the company’s past compliance with tax and other financial obligations. The assessment also takes into account the company’s solvency - the company may not be subject to debt recovery proceedings and may not have gone bankrupt.

Major deviation in the taxi sector in the risk of the grey economy

The risk level decile for involvement in the grey economy was lower among transport licence holders compared to Finnish companies on average. Among the transport licence holders, the average risk level decile for involvement in the grey economy was the highest among taxi licence holders (5.0), while being 3.7 for goods transport licence holders and 3.5 for passenger transport licence holders. However, major deviation was observed in the taxi sector, as the observed group included a large number of both low-risk and high-risk companies. More than 10 per cent of taxi companies were found in the highest risk category (10).

Estimated risk level decile for involvement in the grey economy among transport licence holders

The risk of involvement in the grey economy was assessed using machine learning models based on tax audit results and the companies’ financial and administrative background data. The models enabled forming a risk distribution that covers the entire business sector, which made it possible to make comparisons between the licence holders and other Finnish companies.

Licence requirement reduces both neglect of tax obligations and the risk of the grey economy

Having a transport licence reduced the likelihood of neglecting tax obligations in companies. This result was visible in all licence types examined. In all three licence types, the risk forecast for the grey economy was on average one tenth lower for licence holders compared to companies without a transport licence. The impact of the transport licence on combating the grey economy was assessed by comparing the companies with a transport licence with reference companies without a transport licence operating in the transport sector.

The report supports strengthening the common licence conditions in the transport sector and enhancing oversight by the authorities. The taxi sector requires special attention, as it includes companies with good conduct as well as high-risk companies.

22.9.2025 | The Public Procurement Act Helps Combat the Shadow Economy – Yet hundreds of high-risk operators remain hidden in public procurement

The Public Procurement Act Helps Combat the Shadow Economy – Yet hundreds of high-risk operators remain hidden in public procurement

22.9.2025

Companies participating in the competitive tendering of public procurements have significantly lower risk of involvement in grey economy practices compared to similar companies that do not take part in tendering processes. However, companies identified as grey economy operators in tax audits have submitted the lowest bids each year, worth approximately 200 million euros. Risks are especially present in the field of service procurements, and the legislation does not allow for comprehensively investigating the reliability of companies’ responsible persons. A recent publication of the Grey Economy Information Unit examines the impact of the Act on Public Procurement and Concession Contracts on combating the grey economy.

Hundreds of grey economy companies in public procurement annually

In Finland, tens of billions of euros are spent on public procurement every year. Thanks to the exclusion criteria included in the Act on Public Procurement and Concession Contracts, operators who have previously neglected their obligations or have a criminal background can be excluded from competitive tendering. This prevents grey economy operators from participating in competitive tendering, and it also encourages companies and businesses to fulfil their social obligations.

The participants in the tendering processes were mostly financially sound companies with an extensive history in the field, and their risk of engaging in grey-economy practices differs substantially from the average company population. In 2022–2023, up to more than 100 companies classified as grey economy operators in tax audits still took part in competitive tendering per year. They submitted over 200 of the lowest tenders each year, with a total value of approximately EUR 200 million. Hundreds of tender-winning companies, or their responsible persons, were found to have shortcomings in meeting statutory obligations. The total value of winning bids submitted by such companies ranged annually between 385 and 630 million euros.

Procurement entities are also obliged to determine the reliability of companies’ responsible persons. However, legislation does not make it possible to obtain confidential information from other public authorities concerning key persons. This is problematic, as there were hundreds of companies that did not have shortcomings in the fulfilment of their obligations and participated in competitive tendering each year, but their background persons had issues such as tax debt or enforcement debt.

The Act on Public Procurement is effective – Even companies with a criminal background are rare

The Act on Public Procurement and Concession Contracts was found to have a preventive impact on the grey economy. This impact was studied using two response variables, namely a grey-economy risk decile estimated with a machine learning model and the companies’ compliance with their own obligations. Based on each method, the risk of grey economy practices was found to be lower among the companies that participated in public tendering processes than among the control group. The companies that participated in tendering processes were also more likely to fulfil their obligations. Furthermore, the study revealed that companies that participated in competitive tendering processes covered by the scope of the Act on Public Procurement and Concession Contracts were significantly less likely to neglect their obligations than companies that participated in small-scale tendering.

Companies with responsible persons who have been found guilty of crimes listed in the Act on Public Procurement and Concession Contracts shall be excluded from tendering processes. In 2022–2023, a few dozens of such companies participated in competitive tendering processes, and in 45 cases they submitted the lowest tender. However, several essential criminal offence categories describing the unreliability of the operator are still missing from the exclusion criteria.

Risks detected especially in service procurements – More effective prevention requires better access to information

Companies that submitted the lowest offer in competitive tendering processes in the field of service procurements were found to have a higher risk of engaging in grey economy practices, and they also demonstrated more shortcomings in compliance with obligations, than companies that participated in competitive tendering for procurements and supply purchases in the construction sector. Furthermore, it was found that sectors such as forestry, accommodation and catering were also associated with an increased risk of grey economy practices.

The study also explored more efficient methods for identifying grey-economy operators and excluding them from the tendering processes. This objective could be promoted by measures such as the digitalisation of processes and extending procurement entities’ access to information for monitoring during the contract period. According to the report, it would also be necessary to develop procurement entities’ access to information on background persons.

19.8.2025 | Financial reliability as a condition for money collection permits and discretionary government grants

Financial reliability as a condition for money collection permits and discretionary government grants

19 August 2025

From the perspective of combating the grey economy, an organization applying for a money collection permit or discretionary government grant should be financially reliable. Economically reliable operators have fulfilled their official statutory obligations and are not undergoing measures such as enforcement or bankruptcy. The Grey Economy Information Unit has assessed how the financial reliability of associations and foundations would affect the granting of money collection permits and access to discretionary government grants. In addition to combating the shadow economy, the requirement for financial reliability would also improve the reliability of how the funds received as subsidies are used.

The requirement for financial reliability combats the shadow economy

The requirement for the financial reliability of organization applying for a money collection permit or discretionary government grant would support the fight against the shadow economy, as grey economy activities involve neglect of statutory obligations to the authorities, such as taxes and other statutory payments. Neglecting statutory obligations also increases the risk of other negligence in the activities of organization. For example, the likelihood of neglecting tax liabilities is higher for operators with missing trade register data or other breaches of provisions in relation to their activities. A link has been found on the criminal background of persons responsible for companies and irregularities in the management of companies’ tax liabilities. The requirement that the financial obligations be fulfilled and their regular clearing could also improve the reliability of money collection activities.

Having a financially responsible manager improves the reliability of activities

Managers of organization receiving public funding or collecting funds from the public should also be financially reliable. The persons responsible for associations and foundations represent the organizations and manage their activities. If the persons responsible for organizations neglect their obligations, this also increases the risk of abuses and the grey economy in the organizations they manage. This, on the other hand, may affect the reliability of how the government grants or the collected funds are used. The performance of individual financial obligations is already cleared, for example, in security clearances or business operations subject to a licence. This is done because neglecting obligations could pose a risk that the individual might compromise the reliability of the activities when performing their work tasks. The financial reliability of individuals would be particularly important in the case of activities involving management of funds received as subsidies or donations.

Had the financial reliability of the persons responsible for an association or foundation been used as a condition for obtaining a money collection permit in March 2025, the money collection permit could have been denied to approximately 200 associations and foundations with a collection permit. This represents approximately 15% of all money collection permits granted. If the financial reliability of the persons responsible for associations and foundations had been used as a requirement for receiving a discretionary government grant in 2023, the requirements could have affected the activities of nearly 400 associations and foundations. In 2023, these organizations were paid almost EUR 30 million in business subsidies or comparable financial assistance. In the review published by the Grey Economy Information Unit, the information used for assessing reliability included data on individual assessments by estimation, tax debts, enforcement measures and bankruptcies as well as bans on business operations.

When an organization is applying for a money collection permit or discretionary government grant it may be necessary to clear the financial reliability of the other companies managed by the persons responsible for the entity if the data on the organization or its responsible persons alone does not enable forming a sufficient picture to assess the reliability of the organization concerned. Negligence in the activities of other companies managed by the responsible persons may also be reflected in the activities of the applicant for a money collection permit or the recipient of a discretionary government grant. The responsible persons usually use the same operating model also when managing business in other companies.

40% of associations did not submit a tax return – no comparative data on taxation

Associations and foundations must submit a tax return if they have tax transactions during the tax year, including taxable income or ownership changes related to real estate units, or if the activities of a non-profit association have changed significantly compared to the previous tax year. Approximately 40 per cent of associations receiving discretionary government grants or granted a money collection permit had submitted no tax return at all during the previous three years. No comprehensive financial data were available for these associations to allow assessing their financial reliability. This is another reason for which it would be important to clear the reliability of the responsible persons and the other companies managed by them.

The data content of the Register of Associations should be improved

The reliability of persons involved in the management of approximately six per cent of the associations that received discretionary government grants in 2023 could not be assessed at all, as there was no personal data at all recorded on the responsible persons in the Register of Associations. In 2023, approximately EUR 19 million in discretionary government grants had been paid to these 242 associations, which is more than eight per cent of all business subsidies paid to associations. Only one per cent of associations with a money collection permit had insufficient information. In addition to shortcomings in the responsible person data, it has also been found that the personal data in the Register of Associations are partly incorrect. For example, in 2024, some persons assigned as responsible persons in the Register of Associations would have been as old as 117 years of age. This shows that not all information in the Register is up to date.

The associations should be obligated to report information on the members of their boards and any recent changes to the Register of Associations on pain of a fine or negligence penalty. This would make it possible to clear the reliability of the persons responsible for all associations, for example, as a condition for receiving a money collection permit or a discretionary government grant.

Link to the Finnish Tax Administration’s media release 19.8.2025 (in Finnish) [.fi]›

Review 19 August 2025 The impact of compliance reports on combating the grey economy

10.6.2025 | Tax audits have a wide impact on the tax behaviour of companies in the grey economy

Tax audits have a wide impact on the tax behaviour of companies in the grey economy

10.6.2025

The Grey Economy Information Unit has found that tax audits have led to a significant increase in companies' taxable income. Similar, although weaker, effects were also observed in the related companies of the tax audited companies. A recent study examined the impact of tax audits on the tax behaviour of limited liability companies in the grey economy in the tax filing periods following the audit.

The study found that the net profit declared by the audited companies increased on average by around EUR 72,000 per tax year, which implies a calculated increase of around EUR 14,500 in corporate income tax.

The impact of tax audits on the tax behaviour of limited liability companies is wide-ranging

Among the 348 audited companies, changes in reporting behaviour had a significant impact on the amount of corporate income tax. The estimated impact of these changes on the amount of corporate income tax was on average around EUR 5 million per tax year. This suggests that tax audits have a significant indirect fiscal impact. By comparison, the average amount of corporate income tax imposed on the same companies based on audit findings was around EUR 2.7 million per year.

The impact of tax audits on salaries and fees

The salaries and fees declared by audited companies increased by around EUR 34,000 per tax year. This result suggests that audited companies are also reviewing their employer reporting practices, which improves the position of employees and increases tax revenues.

Impact of tax audits on affiliated companies

The study examined the impact of tax audits not only on the tax behaviour of limited liability companies but also on their related companies, identified through responsible persons. According to the results of the study, the taxable income of the related companies also increased by an average of EUR 14,000 per tax year after the tax audit, which translates into an increase of EUR 2,800 in corporate income tax. This suggests that the impact of tax audits may also extend to the related parties of the audited companies.

The tax audit also has a steering effect

Tax audits are an important tool in tax control. They identify grey economy activities such as missing sales and unjustified expenses. These means can be used by companies to artificially reduce their tax burden and gain a competitive advantage in the market. Tax audits also reveal possible tax fraud. Companies with large-scale and serious grey economy activities often go out of business after a tax audit. However, the tax audit also guides and supports businesses to do the right thing.

"The changes in tax behaviour revealed by the study are significant when looking at the growth of taxable income in relation to companies' turnover. Based on the results of the study, taxable income increased by an average of around 4% – and by 20% relative to the median turnover. The differences in the proportions show that the companies included in the analysis were of very different sizes." says Head Analyst Alem Luoma of the Grey Economy Information Unit.

Extrapolation of the results and future research opportunities

The number of companies examined in the study was relatively small, which affects the extrapolation of the results. In the future, it would be useful to extend the study to a larger number of companies. This would allow a more holistic assessment of the effectiveness of tax audits, for example according to groups of companies.

"The effectiveness of a tax audit is a broad issue that requires several different approaches to consider in a holistic way. Different types of companies may behave very differently after a tax audit. However, the results of the study clearly show the influence of the tax audit on companies, which is not limited to the audited companies but also extends to some extent to related companies," says Janne Marttinen, Director, Grey Economy Information Unit.

19.05.2025 | Financial reliability as a condition for discretionary government grants – more than EUR 100 million would be denied to associations and foundations

19.5.2025 | Financial reliability as a condition for discretionary government grants – more than EUR 100 million would be denied to associations and foundations

19 May 2025

In 2023, up to EUR 65 million in discretionary government grants would not have been paid to associations and EUR 59 million to foundations if the financial reliability of their responsible persons and their associated companies had been a condition for paying the grants. The Grey Economy Information Unit has assessed how reforming the Act on Discretionary Government Grants to combat the grey economy would affect the payment of discretionary government grants to associations and foundations. From the perspective of combating the shadow economy, discretionary government grants should only be paid to financially reliable parties that have fulfilled their official statutory obligations and are not undergoing measures such as enforcement or bankruptcy.

Only 1.3% of associations that received discretionary government grants in 2023 had neglected their statutory obligations to the authorities. However, nearly EUR 3 million in discretionary government grants were paid to these associations in 2023. Of the associations in the target group included in the review, 40% had not filed any tax returns between 2020 and 2022, and no financial data that could be used to assess their financial reliability is available on the associations. For this reason, it would be important to investigate whether the persons managing associations fulfil their obligations.

Negligence of management of official obligations common among persons responsible for associations

An investigation of the financial reliability of the persons responsible for associations could have affected the grants received by approximately 350 associations and the refusal to pay grants amounting to EUR 23 million. This would correspond to around ten per cent of all government grants paid to associations. The responsible persons of the associations also included individual persons subject to a ban on business operations. The associations managed by these individuals received more than half a million euros in government grants. A review of the obligations of the responsible associated companies would have affected the receiving of grants of 800 associations, and the amount of refused grants would be as much as EUR 65 million.

Other companies of persons responsible for foundations have failed to meet their obligations

In 2023, only five foundations had shortcomings in managing their financial obligations. These foundations were paid little less than one million euros in discretionary government grants. If, in addition to the financial reliability of the foundations, the negligence of the persons responsible for the foundations and their associated companies had been investigated, the restrictions would have applied to as much as about half of the foundations that received grants. In 2023, nearly EUR 60 million in discretionary government grants were paid to these foundations, amounting to around two thirds of the total assistance paid to the foundations.

The requirement for the financial reliability of operators applying for government grants would promote the efforts to combat the shadow economy. As a party failing to comply with the obligations governed by public law may also neglect other provisions or requirements related to grants, the efforts to combat the shadow economy would prevent possible fraudulent actions.

Register of Associations data is partly incomplete

The reliability of persons involved in the management of approximately six per cent of the associations that received discretionary government grants in 2023 could not be assessed at all, as the personal data recorded on the associations in the Register of Associations was incomplete. In 2023, approximately EUR 19 million had been paid to these 242 associations, which is more than 8% of all grants paid to associations. The associations should be obligated to report information on the responsible persons and any recent changes to the Register of Associations on pain of a fine or negligence penalty. This would also improve the obligation laid down in the Act on Preventing Money Laundering and Terrorist Financing regarding knowing and identifying the actual beneficial owners of corporate entities. An obligation for associations to submit their annual financial statements to the Finnish Patent and Registration Office would also improve the transparency of their activities.

10.02.2025 | Neglecting the reporting requirement results in removal from the Trade Register

Neglecting the reporting requirement results in removal from the Trade Register

10.2.2025

Each year, the Finnish Patent and Registration Office (PRH) removes many companies from the Trade Register for neglecting their requirement to submit reports or not having a quorate board of directors. In 2019–2023, the PRH removed nearly 50,000 companies from the Trade Register due to a failure to submit their financial statements.

The Grey Economy Information Unit examined companies that were removed from the Trade Register in 2019–2022 for having neglected the requirement to submit reports on financial statements. In tax audits, it has been found that some companies continue to engage in business activities despite their removal from the Trade Register. A company that continues its activity outside the registers may be an instrument of shadow economy.

An amendment to the Trade Register Act makes it possible to re-enter a company to the Trade Register after removal due to negligence

In October 2024, the PRH suspended the removal of companies from the Trade Register while the legislative amendment was being processed. The PRH had re-entered companies based on applications if they had been removed from the Trade Register by the end of 2022, but companies removed after 1 January 2023 were no longer re-entered. The aim of the rapidly progressing legislative amendment was to enable, under certain conditions, the re-entering of companies removed from the Trade Register. The amendments to the Trade Register Act in accordance with the legislative proposal were adopted on 30 December 2024, and the act entered into force on 1 January 2025.

The procedure for removing and re-entering companies to the Trade Register incurs costs and inconvenience for both the companies and the authorities. In the view of the Grey Economy Information Unit, removing active companies from the Trade Register should be the last step after a comprehensive reminder process and sanctions.

Investigation project with the collaboration of multiple authorities is being planned

The legal effects of a company being entered in the Trade Register are regulated comprehensively, but the legal effects of being removed from the register have not been unambiguously regulated. This leads to various interpretation problems with regard to the obligations, responsibilities and rights of companies removed from the register. The action plan for tackling the shadow economy and economic crime (2024–2027) contains an investigation project aimed at identifying the challenges, legal provisions and public authorities’ actions that cause the main problems related to companies removed from the Trade Register. The purpose of the investigation project is to prepare concrete proposals for eliminating those problems.

14.01.2025 | Up to EUR 250 million of government grants paid annually to companies neglecting their obligations

Up to EUR 250 million of government grants paid annually to companies neglecting their obligations

14 January 2025

The grey economy is not always an obstacle to getting discretionary government grants, and millions of euros in government grants are paid to companies that neglect their public obligations. The Act on Discretionary Government Grants does not currently include enough provisions for combating the grey economy. From the perspective combating grey economy, it is essential that the recipient of a discretionary government grant has fulfilled its statutory obligations. A report published by the Grey Economy Information Unit examined the tax reliability of limited liability companies that received government grants in 2023, the government grants received by companies at high risk of grey economy, the impact of tax audits on applying for grants and the impact of possible legislative amendments on granting government grants.

Reforming the Act on Discretionary Government Grants would combat the grey economy

The Grey Economy Information Unit has assessed how reforming the Act on Discretionary Government Grants to combat the grey economy would affect the payment of discretionary government grants. In the proposed amendment, discretionary government grants could only be paid to financially reliable parties that have fulfilled their official statutory obligations and are not undergoing measures such as enforcement or bankruptcy. Based on the results of the report, EUR 255 million of discretionary government grants would not have been paid to limited liability companies in 2023 if financial reliability had been a criterion for the payment of the grants.

The examination for the report separated limited liability companies into two categories: ones that had received individual subsidies of over EUR 100,000 and ones that had received individual subsidies of over EUR 10,000. Based on the findings of the report, some EUR 145 million of individual government grants exceeding EUR 100,000 and some EUR 230 million of individual government grants exceeding EUR 10,000 million had been paid to companies where the company, a responsible person at the company or associated company had significantly neglected their statutory obligations. When the financial reliability was examined solely based on the limited liability company´s management of its obligations, approximately EUR 40 million would not have been paid even then. Some EUR 13 million would not have been paid to limited liability companies that received individual subsidies of over EUR 100,000.

The examination found that the responsible persons of limited liability companies that received discretionary government grants included members of management who were subject to a ban on business operations; their companies received more than EUR 300,000 in discretionary government grants. In addition to fulfilling statutory obligations, another factor in granting discretionary government grants could be more extensive information on criminal background. To implement reliability regulation, the option to use the compliance reports produced by the Grey Economy Information Unit should be extended to several government grant authorities to support the prevention of grey economy.

Tens of millions of euros of discretionary government grants to operators in the grey economy

The findings of the report indicate that the recipients of discretionary government grants in 2023 included companies that were assessed to be grey economy companies based on tax audits carried out on limited liability companies. In 2023, some 200 limited liability companies in the grey economy received discretionary government grants, and the total sum of the grants was approximately EUR 29 million. The most common contribution paid to companies defined as grey was pay subsidy.

Issues with companies’ fulfilment of obligations subject to public law may also reflect their risk of involvement in the grey economy. As a rule, discretionary government grants should only be granted to parties that manage their obligations and have the prerequisites for profitable business activities. Based on the results of the report, the business subsidy system seems to be only a minor factor in improving companies’ fulfilment of their obligations. Even a tax audit revealing significant grey economy did not interrupt ongoing companies’ participation in the business subsidy system. Companies would probably be more motivated to fulfil their statutory obligations if doing so was a statutory requirement for receiving grants.

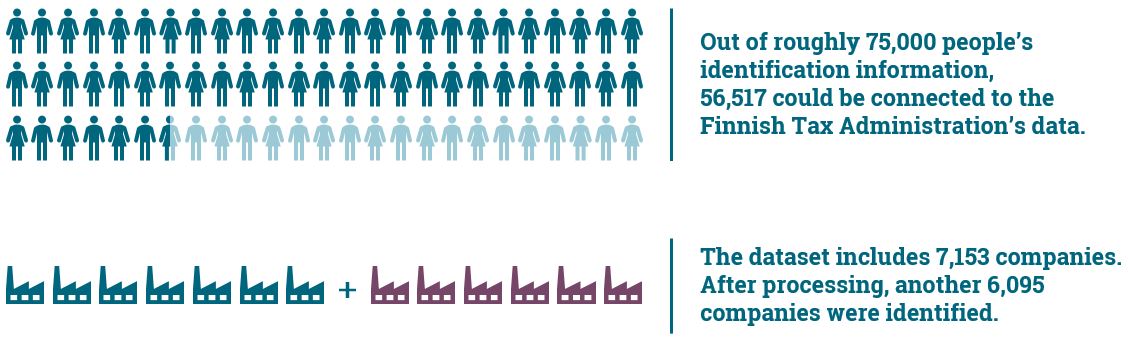

In the Act on Discretionary Government Grants, discretionary government grants mean financing awarded in the form of financial support for an activity or project. Discretionary government grants do not include financial benefits in the form of loans, guarantees or tax relief. Depending on the method of calculation, some EUR 4 billion of discretionary government grants are awarded annually, of which companies have accounted for about 30 per cent. In 2023, more than 16,000 limited liability companies received a total of nearly one billion euros in discretionary government grants, including some 75,000 individual disclosures of discretionary government grants.

Studies from 2024

9.12.2024 | Organised crime is gaining ground in the business world

Organised crime is gaining ground in the business world

9.12.2024

There are individuals involved in organised crime activities holding responsible positions in thousands of Finnish companies. This is one of the findings presented in the first report on business activities carried out by organised criminal groups in Finland. The report utilised, for example, the observation and monitoring data of the National Bureau of Investigation.

Lines of business familiar from the grey economy

Companies involved in organised crime operate especially in the fields of construction, real estate and car sales. These are traditional risk sectors of the grey economy, where there is also a lot of undeclared work.

The Government has defined certain lines of business as critical for society. Nearly 130 companies linked to organised crime were found to operate in critical lines of business. These companies represented such fields as cleaning services and security services.

Tax liabilities were fulfilled poorly, and the key business figures were weak

The tax debt of companies involved in organised crime totalled more than EUR 16 million at the end of 2022. The number of assessments based on estimated income carried out in these companies was also many times higher than in other companies.

Compared to the rest of the company population, these companies were smaller and less profitable and often had negative equity. Their financial statements were also often incomplete.

The damage caused to society by organised crime is significant

Because of the grey economy activities practised by organised crime, society loses more than EUR 40 million every year. The estimate does not cover all losses caused by organised crime, such as damage resulting from money laundering.

In Finland, the situation is still manageable, and by preventing it, we avoid any greater damage. When comparing the situation in Finland to Sweden, in Finland, the number of active operators is only one tenth of that in Sweden, and the damage caused by crime is only a fraction of that in Sweden. In Sweden, the criminal proceeds of organised crime are estimated to amount to up to EUR 15 billion and the additional costs incurred by the business sector to EUR 9 billion.

Combating organised crime is one of the priorities of Petteri Orpo’s government. The strategy against organised crime currently being prepared will provide a holistic approach to tackling this phenomenon. The strategy will be completed by the end of 2024.

Read the full report in Finnish (PDF 1.1 MB)

Link to the Finnish Tax Administration’s media release 10.12.2024 [.fi]›

18.11.2024 | One fifth of Finnish limited liability companies would not meet reliability requirements

One fifth of Finnish limited liability companies would not meet reliability requirements

18.11.2024

The purpose of reliability requirements is to ensure that a company is economically viable and meets its societal obligations. Reliability requirements allow the public authority to deny a registration, licence or subsidy from an applicant who neglects their obligations. Regulations on companies’ reliability have been especially introduced in sectors that are societally significant or involve a higher-than-usual risk of the grey economy. Similar regulations are also included in legislation on contractor liability and procurements.

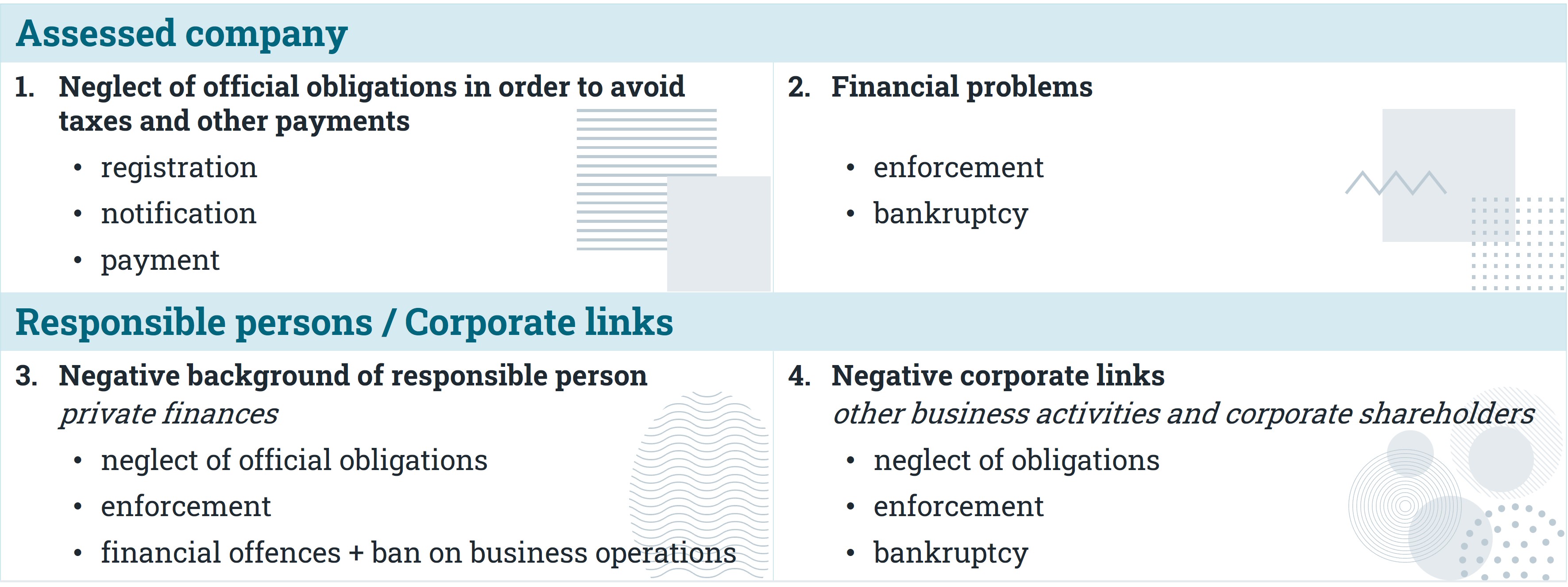

What does reliability assessment involve?

Assessing a company’s reliability by examining its past activity enables drawing conclusions on its future activity. If a company has been able to fulfil its obligations related to taxes and other payments, it is likely able to fulfil its other social obligations as well. The company also needs to be solvent. It cannot be undergoing enforcement or bankruptcy. Reliability regulations often also make it possible to perform similar checks on companies’ responsible persons and any other linked companies.

Reliability assessment

Corporate link = same responsible person in both companies, or mutual ownership relationship between limited liability companies

The likelihood of grey economy in a company is increased most by responsible persons’ tax and enforcement debts. Changes in individual income taxation and assessment by estimation also significantly increase the risk of grey economy in a company. There is a strong link between a responsible person being convicted of economic crime and neglect of corporate tax liability.

Tax debt and errors in tax returns of other linked companies increase the risk of the assessed company neglecting its obligations. In addition, the likelihood of grey economy in linked companies has been found to be associated with the likelihood of grey economy in the assessed company.

How would Finnish limited liability companies meet reliability requirements?

When reliability is examined from the data of Finnish limited liability companies, some 16,500 companies would not meet the reliability requirements due to neglected obligations or financial problems. Including the negligence of responsible persons’ private finances would increase the number to nearly 52,000 limited liability companies, or one fifth of all limited liability companies in operation. Examining the corresponding data of linked companies would only increase that number by 2,000.

This article is based on a report by the Grey Economy Information Unit (in Finnish):

How to identify the responsible person of a grey economy company, 2024 (PDF 822 kB)

Impact of high-risk links on the activities of a limited liability company, 2024 (PDF 885 kB)

Significance of criminal record data on the negligence of obligations, 2022 (PDF 907 kB)

21.10.2024 | Combating the grey economy need sufficient resources and up-to-date powers

Combating the grey economy need sufficient resources and up-to-date powers

21 October 2024

In its report, the Grey Economy Information Unit examined tax audits of the grey economy, some of which were carried out at the same time as pre-trial investigations by the police. Tax audits on grey economy operators reveal a high number of cases of aggravated tax fraud. The police’s financial crime investigation resources are not sufficient to deal with the ever-increasing number of reports of crime. Updating the Tax Administration's powers and tax auditing rights to modern standards and increasing the resources of the police in the fight against financial crime would improve both tax collection and the detection of crimes.

Number of tax audits in the grey economy on the rise

Every year, tax audits are detecting more and more serious tax offences that lead to the filing of a report to the police. Tax audits on the grey economy are also being carried out in cooperation with the police’s pre-trial investigations, so called real-time tax audits. The number of real-time tax audits has decreased significantly in recent years.

Around 8,800 tax audits were carried out between 2019 and 2023, only about 3% of which were carried out as real-time tax audits. An increasing number of tax audits are leading to the consideration of a report of an offence. In 2019, a quarter (26%) of all tax audits were in the grey economy, i.e., they were either carried out at the same time with police’s pre-trial investigation or led to the consideration of a report of an offence. In 2023, almost half (45%) of tax audits were in the grey economy.

Financial crime investigations are severely backlogged

The Tax Administration is often a partner of the police in financial crime investigations. Cases of tax fraud can be large and complex, often involving a large amount of documentary material. The complexity of criminal investigations and court proceedings often means long processing times and considerable costs. Digitalisation has enormously increased the amount of data to be investigated, challenging both the criminal investigation and the tax audit. Increased internationalisation often requires extensive inquiries about administrative assistance.

Data from the resource monitoring tool on the Grey Economy and Economic Crime website shows that the number of financial crime reports and open cases reported to the police has increased significantly over the last five years. From 2019 to 2023, the number of reported offences increased by around 20% and the number of open cases by about 40%. According to prevention statistics, almost half the cases investigated by the police in financial crime investigations are tax and accounting offences.

Cooperation improves the imposition of criminal liability in tax offences

The study collected the experiences and views of real-time tax audits through interviews. A small group of experts in the fight against the grey economy from the police and the Tax Administration were interviewed. Stopping the activities of the grey economy and removing the proceeds of crime from the offenders are effective deterrents to further criminal activity. The key to tackling the grey economy is to hold offenders criminally accountable for their actions. It is clear, that simultaneous tax audits and criminal investigations allow the authorities to use their monitoring tools effectively. Coercive police measures usually provide more comprehensive material to be investigated, as well as evidence of the facts and the perpetrators. The collection of digital material often requires the seizing of computers and other smart devices, and this is effectively done through coercive police measures.

What do the experts think about the current situation?

Tax auditing rights are not up to date

According to tax law, the taxpayer's duty to disclose information and material for the purposes of a tax audit is extensive. In the case of tax audits in the grey economy, even more extensive research is often needed, both to reach the operators and to obtain the material to audit. In real-time tax audits, it has been possible to search for and seize accounting materials using coercive means by the police. However, police financial crime investigations are no longer providing enough help because there are simply not enough resources.

It is not possible to increase police resources for financial crime investigations to make real-time tax audits sufficiently comprehensive for tax audits of serious grey economy. In order to ensure that the Tax Administration can continue to combat the grey economy also in the future, legislation and tax auditing rights need to be updated and developed. The Tax Administration lacks the explicit right to carry out tax audits, secure evidence and verify identity.

What can be done about this situation?

The number of tax audits in the grey economy, the number of offences referred to the police for investigation and the number of cases of financial crime are on the rise. Could the ratio of resources to workload be eased, for example through legislative changes or the fine tuning of policies?

- For example, could the necessity of carrying out a criminal investigation be changed, or could the investigation be speeded up?

- Would a tax increase be a sufficient punishment more often?

- Is the line drawn between basic and aggravated tax fraud correctly positioned?

There is no single cure-all remedy to the situation.

21.10.2024 | Only companies that fulfil their public obligations and are economically reliable can take responsibility for their environmental obligations

Only companies that fulfil their public obligations and are economically reliable can take responsibility for their environmental obligations

The Tax Administration, Grey Economy Information Unit 21 October 2024

An environmental permit must be applied for activities that may cause environmental damage or pose a related risk. Such activities include forestry, metal and chemical industries, energy production, large animal shelters and fish farming. The environmental permit may issue provisions on aspects such as the scope of the activity and its emissions and their reduction. The preconditions for granting the permit include that the activity must not cause health hazards or significant environmental damage or related risks.

The environmental permit gives the permit holder the right to put a strain on the environment, and a legal requirement to restore the sites after the completion of the company’s activity. Only an economically sound and financially viable undertaking can fulfil the obligations imposed by the permit. After the bankruptcy of a permit holder, restoration work remains the responsibility of society. Legislation on environmental permits does not set requirements for the financial reliability of the applicant and holder of an environmental permit or for the management of public obligations related to business activities.

We examined how approximately 6,500 permit-holding companies engaged in business activities have fulfilled their tax obligations as well as the permit holders’ financial situation and capability to fulfil their tax obligations and other responsibilities related to business. There were no agricultural producers in the data set.

Key statistical observations on permit holder companies:

Companies’ tax debt indicates a long-term internal financing problem. Weak key figures on profitability, indebtedness and liquidity predict a reduced capacity to manage business-related payment obligations. Loss of equity means that the company does not have any assets in the balance sheet to meet its payment obligations related to its business activities. A lack of means established by enforcement means that the company does not have the funds to manage its public obligations or other liabilities arising from the business activity.

Reliability requirements – the example of the prerequisites for entry into the waste management register

Up to 400 (6%) environmental permit holders would probably not meet the requirements for economic reliability and the management of public obligations if they were active in a line of business requiring waste management registration. Reliability provisions corresponding to the Waste Act are also required in numerous other Finnish sectors requiring a permit or registration. Similar provisions could also be well-suited as prerequisites for environmental permits.

Under the Waste Act (section 95), an operator is not regarded as economically reliable if:

1) the operator has, during the current year or within the three calendar years preceding it, repeatedly or to a significant extent failed to comply with its registration, notification or payment obligations relating to taxes, statutory pension, accident insurance or unemployment insurance contributions or payments levied by Customs; or

2) the operator has debts being collected through enforcement that are greater than minor in relation to its solvency or debts that have been returned from enforcement with an impediment certificate issued because of lack of means; or

3) the operator has been declared bankrupt.

24.09.2024 | A view to the foundations: Corporate governance and financial administration also affect the management of tax obligations

A view to the foundations: Corporate governance and financial administration also affect the management of tax obligations

24 September 2024

A building condition assessment is not focused on surfaces; instead, attention should be paid to the structures of the building. As a result, the assessment involves exploring issues such as the condition of the building’s foundation. The same applies to business activities: the foundations of the company are built on governance and financial administration. If these processes are out of order, the legality of the business and the reliability of the financial data obtained on this are at stake.

A report published by the Grey Economy Information Unit shows the importance of governance and financial administration also from the perspective of the fulfilment of tax obligations. The examination included micro-sized limited liability companies whose size exceeded the size limits of the audit obligation.

Shortcomings in the company’s Trade Register information indicate a greater likelihood of neglecting tax obligations

Based on the findings of the report, the likelihood of neglecting tax obligations is higher for companies that have deficiencies in their Trade Register information concerning their board of directors, financial statements or financial audit. Neglecting tax obligations was the most common in companies with the above shortcomings in Trade Register information and which are at the end of their life cycle.

These results are unsurprising as in micro-enterprises in particular, the business tax return is derived fairly straightforwardly from the company’s accounting and financial statements. The shortcomings in the company’s governance or financial administration process are inevitably also reflected in the fulfilment of tax obligations. The results also indicate that the shortcomings in notifications submitted to various authorities accumulate in certain companies. The company’s board of directors and management nonetheless bear the overall responsibility for reporting the information to various authorities in a timely manner and with the correct content. This responsibility also remains in situations where the company is about to cease its operations.

Based on our experience, we know that compliance with payment obligations related to business activities declines situations where the company is facing financial difficulties, says Johanna Miettinen, Senior Adviser at the Grey Economy Information Unit. At the same time, invoices for services related to accounting and auditing are also at risk of being left unpaid. Due to the end of customer relationships, reliable financial information is no longer obtained on the company’s business activities. In this situation, one of the cornerstones supporting business operations has collapsed and there is a risk that the company will be unable to submit tax returns with accurate content to the Tax Administration.

Several developments affecting the financial reporting of micro-enterprises are ongoing in Finland

The report examined the impact of the selection of an auditor and the method of submitting the financial statements and tax returns on the fulfilment of tax obligations. Based on the results, micro-enterprises utilise the flexibility offered by legislation in their arrangements for governance and financial administration. To some extent, these choices are also reflected in the management of tax obligations.

For example, the likelihood of neglecting tax obligations was found to be lower for companies that had selected a large auditing firm as their auditor than for those that had selected some other party as their service provider. Similarly, minor differences in quality were observed between authorised accounting firms and other financial administration service providers.

The financial administration sector has been undergoing significant changes due to the polarisation of the market. Accounting firms and auditors are increasingly specialised in serving certain types of clients. Meanwhile, legislation aimed at combating money laundering and terrorist financing has become stricter in recent years. Larger operators are better equipped to manage their client risks also from this perspective. In the future, there is a need to pay attention to whether the financial administration and auditing market is becoming increasingly differentiated based on customer risk. This factor should also be taken into account in combating the shadow economy.

The size limits for the auditing obligation also arise in discussions at regular intervals. For example, the exclusion of all micro-sized companies from the statutory audit obligation has been repeatedly proposed. Based on the results of the study, this trend is not desirable. Based on the findings, the audit reports contain information that can also be used to assess the fulfilment of the company’s tax obligations.

Digitalisation creates new opportunities but also raises concerns related to combating the shadow economy

The report also provided indicative evidence that the manner in which the tax return and financial statements are submitted is relevant to the fulfilment of tax obligations. In general, the use of online notification channels promotes the appropriate fulfilment of tax obligations.

As digitalisation increases, access to information and the development of information exchange between the authorities will also open up new opportunities for combating the shadow economy. A broader knowledge base enables a more comprehensive examination of companies. From the perspective of companies, this also reduces overlap in the notifications submitted to the authorities.

On the other hand, the authorities have expressed their concerns (survey of changes in the operating environment) about the challenges created by increasing digitalisation and artificial intelligence in combating the shadow economy and financial crime. For example, it may be difficult to identify fictitious information generated by artificial intelligence, such as images and receipts, from the data mass associated with real business.

In other words, the winds of change are also blowing in the financial administration sector. In this change, business needs to be supported by an appropriate foundation. Those working to combat the shadow economy should continue to pay attention to the arrangements companies make for their governance and financial administration. Behind these arrangements, there are individuals who set the level for the fulfilment of the company’s business-related obligations.

Read the full report in Finnish (PDF, 1.36 MB)

19.08.2024 | Does missing association register information increase the shadow economy risk?

Does missing association register information increase the shadow economy risk?

19 August 2024

Only around half of the associations registered in the Register of Associations are in the Finnish Tax Administration’s customer register. Can the missing information increase associations’ business activities outside registers and the shadow economy risk? Associations must submit a tax return if they receive taxable income, for example. The taxability of activities and income is assessed separately in conjunction with taxation.

Business activities outside registers found in tax audits

The Grey Economy Information Unit used taxation information to examine the shadow economy risks of non-profit associations. Tax audit reports from the tax audits of 40 associations were used in the study. Based on the restricted tax audit information, associations engage in business activities outside the Finnish Tax Administration’s VAT Register, for example. In the tax audits, more than €5 million was proposed to be added to the business income taxation of non-profit associations alone, for example.

No other shadow economy activities of the responsible persons of associations were found in the tax audits. Similarly, in earlier studies, business activities outside registers (report in Finnish) have been found as has misuse of associations for shadow economy activities. Undeclared sales income of self-employed persons was directed into the bank account of an association administered by the self-employed person, for example.

Non-profit associations work solely and directly in the public interest, and their activities do not concern a limited group of people only; instead, their activities are open to everyone or otherwise targeted at a large audience. Those participating in the activities of non-profit associations do not receive any financial benefits, such as dividends, profits or unreasonably high wages. Associations that promote non-profit activities include youth associations, sports clubs, and recreational or leisure associations based on volunteer work. (Source: the Finnish Tax Administration – When is an association or foundation a non-profit organisation? [.fi]›)

Hundreds of persons are responsible for associations

Those responsible persons between 30 and 65 years old, meaning chairpersons, persons entitled to sign for an association and reported members of boards, of associations in the Finnish Tax Administration’s customer register were examined in the study. The responsible persons included persons with tax debt or subject to enforcement, but no conclusions on any increase to the shadow economy risk of this group could be made based on the data. Responsible persons with a low income of less than €10,000 annually were paid tax-exempt reimbursements of expenses for a total of €1.6 million during the three years examined (€660–€900/person/year). No misuse was found in the data related to the tax-exempt reimbursements paid to responsible persons. Of the responsible persons, 40 had a valid ban on business operations, which prohibits a person from engaging in business activities but does not prevent a person from engaging in the activities of a non-profit association.

Based on the statistical analysis carried out in the study, of the approximately 55,000 associations in the Finnish Tax Administration’s registers, 1,334 owned real estate units and 2,925 owned apartments in 2017–2022. Of the associations that owned real estate units or apartments, nearly 40% reported rental income from real estate units or apartments renter out.

How could the monitoring of the shadow economy related to associations be improved?

More than 100,000 associations are registered in the Register of Associations maintained by the Finnish Patent and Registration Office, and these associations have nearly 300,000 responsible persons entered. Of the associations in the Finnish Patent and Registration Office register, only around half are registered in the Finnish Tax Administration’s register. This means that the Finnish Tax Administration does not receive information on the activities and responsible persons of all registered associations. The responsible persons in the Register of Associations even include people aged 117 years, which shows that not all of the register data is up to date. Around 700 of the responsible persons do not have a Finnish personal identity code entered in the Register of Associations.

The reporting, publicity and currency of the financial information and responsible person details of associations are vital considering the shadow economy risk related to their activities. Most associations do not submit a tax return to the Finnish Tax Administration or financial statements to the Finnish Patent and Registration Office. Because information is not required to be reported in some cases, the authorities do not have sufficient information on the activities of associations for targeting risk-based monitoring.

Monitoring the shadow economy activities of associations and the transparency of activities could be improved if associations were obliged to submit their annual financial statements to the Finnish Patent and Registration Office. Changes to the board members of associations should be reported to the Register of Associations in addition to any changes to the chairperson of the board or persons entitled to sign for the association.

10.06.2024 | Short lifecycle companies carry a high shadow economy risk

Short lifecycle companies carry a high shadow economy risk

10 June 2024

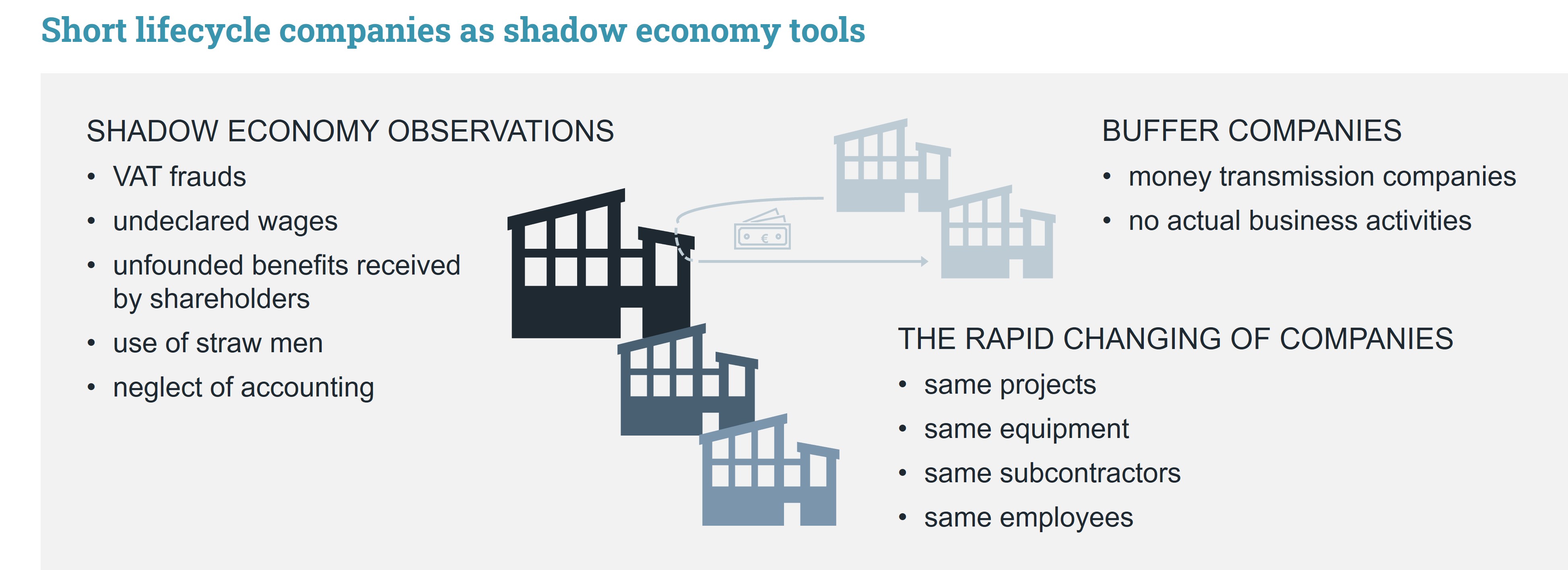

According to a recent report, roughly a third of companies with a short lifecycle carry a high shadow economy risk. These companies are involved in the shadow economy much more frequently than limited liability companies on average. Tax audits especially revealed VAT abuse, undeclared wages and unfounded benefits received by shareholders in the shadow economy activities of short lifecycle companies. The rapid changing of companies, the use of straw men and companies not engaged in actual business activities are signs of the exploitation of short lifecycle companies.

Up to a third of short lifecycle companies carry a high risk

Based on the report’s results, some 4,300 of companies with a short lifecycle carried a high risk from the perspective of the shadow economy in 2018–2022. This was more than a third of all short lifecycle companies operated during the same period. The shadow economy risk was slightly higher in short lifecycle companies that had operated for less than a year than in companies that had already been in business for two or three years. The annual tax gap caused by the shadow economy activities of short lifecycle companies was estimated at roughly €40 million in 2019–2021. In addition, the abuse of short lifecycle companies have an indirect impact on tax revenue from companies operated in the long term, which was not taken into account in the estimate.

Short lifecycle companies are used as shadow economy tools

Based on tax audits, short lifecycle companies are exploited in the shadow economy in the form of systematic arrangements of several companies and as individual companies. VAT abuse, undeclared wages and unfounded benefits received by shareholders were especially highlighted in the shadow economy activities of short lifecycle companies. Some short lifecycle companies were not engaged in any external business activities, as their only purpose was to forward funds, enabling unfounded tax benefits for other companies in the same arrangement. The rapid changing of companies one after the other is another form of the exploitation of companies. Based on tax audit findings, companies often continued the activities of a previous company in the same projects, and using the same equipment, subcontractors and employees.

Various straw men were discovered in roughly a third of all audited short lifecycle companies. More than 70 per cent of all recipients of disguised dividends were other than shareholders entered in official registers. Straw men acting as official responsible persons in companies were often relatives of actual shareholders such as a marital or cohabitant spouse, mother, father, stepmother, child or other relative. In addition to abuse related to registrations, nearly 90 per cent of shadow economy companies with a short lifecycle had neglected their accounting obligations.

Short lifecycle companies are often financially unprofitable

The restaurant sector and retail had the largest number of short lifecycle companies, but many of them also operated in business consulting, house construction, IT services and wholesale. The line of business reported to the authorities did not always match the actual business activities. Based on the report’s results, only less than a fifth of short lifecycle companies were engaged in financially profitable activities, while most of them did not accumulate practically any tax revenue for the state. Dormant companies with a short lifecycle accounted for a considerable part of the tax debt of short lifecycle companies, and they naturally cannot repay their tax debt.

18.03.2024 | Trading with receipts and invoices costs millions for the state

Trading with receipts and invoices costs millions for the state

18 March 2024

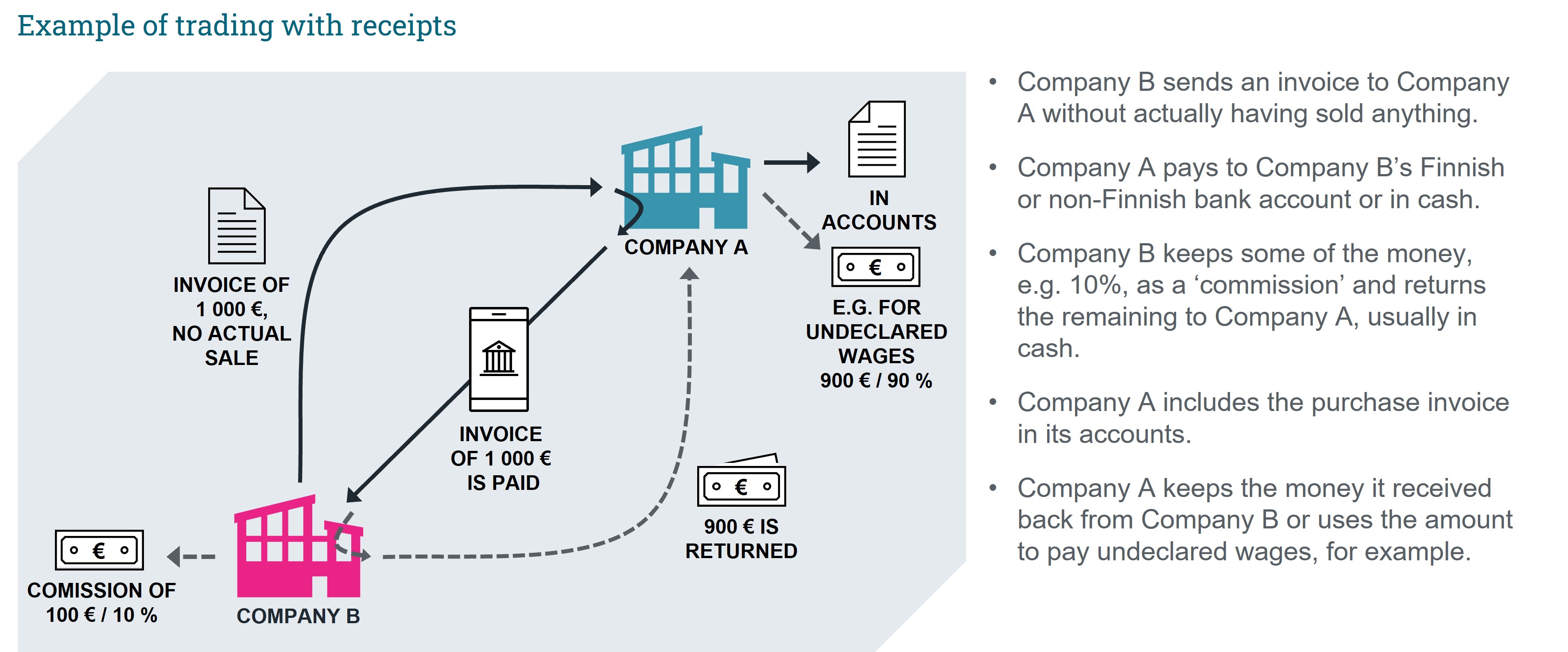

Buying and selling receipts and fictitious or false invoices is used to evade taxes for the worth of millions of euros. Today, tax evasion with buying and selling receipts and falsified documents is becoming increasingly global. In more than half of the cases involving buying and selling receipts, a company has hidden money for undeclared wages or assets have been transferred to a shareholder without paying taxes. This type of fraud is usually discovered in tax audits.

Falsified receipts and invoices are a significant phenomenon of the shadow economy and economic crime

The Grey Economy Information Unit has examined the falsified receipts and invoices discovered during tax audits. A falsified document is a document included in a company’s accounts whose content or amounts do not correspond to real life events. Sometimes the entire document is falsified.