Taxation

Key figures in the prevention and investigation of tax fraud 2025

Source: Finnish Tax Administration

The Tax Administration ensures the accrual of tax revenue through effective control. The Tax Administration is combating the grey economy and other forms of economic crime using various tools ranging from registration to report monitoring and from control visits to tax audits. Efforts are made to stop fraudulent activity at as early a stage as possible. Targets of the grey economy include any objects of tax control under consideration for crime reporting. There are specialized personnel in combating more serious manifestations of the grey economy.

Cooperation between public authorities aims to ensure a comprehensive approach to combating, identifying and preventing different types of economic crime. Control involving multiple authorities investigates problems in certain sectors more extensively. The current low number of real-time inspections, where tax audits are carried out concurrently with pre-trial investigations, challenges the handling of the most demanding tax fraud cases in an increasingly complex environment. Resources are also allocated to activities that do not necessarily have a direct impact on results, such as the enforcement of sanctions and preventive work with stakeholders.

The exchange of tax information between tax administrations in different countries and international cooperation are central to the Tax Administration's work to combat the grey economy and financial crime. The Finnish Tax Administration has a very active role in international anti-fraud forums.

Dishonesty occurs throughout business life

Tax control activities reveal grey economy activities across business life. The professionalisation and intensification of financial crime is also visible in the Tax Administration. In terms of numbers, consumer service sectors such as restaurants and taxis are dominant. The phenomena and problems brought about by the transformation of working life is visible in labour-intensive sectors. Fraud has been detected in car dealerships, e-commerce and, more recently, data centres. Identity fraud, the use of companies as tools for crime, completely bogus declarations and company structures, foreign money transfers, virtual banks and various payment platforms are not dependent on any sector and are occupying the Tax Administration's fight against the grey economy.

Esimerkki alkaa

Turnover of audited grey economy businesses 2025

More than €10 million 2,3 %

€2–10 million 6,2%

Less than €2 million 50,3 %

Not known 41,2 %

The Finnish Tax Administration does not have information on the turnover of all grey economy actors, including foreign companies and companies that have been reported dormant or dissolved. This category also includes natural persons.

Esimerkki päättyy

Huomio osio alkaa

Control results in 2025

The results in euros of grey economy audits have risen, as has the number of audits. Tax fraud is almost always cross-border, money is moving faster than before in different ways and smaller businesses are being exploited. The use of companies and identities as instruments of crime is increasing. The Tax Administration is constantly developing faster means of analysis and control.

The Tax Administration’s bankruptcy petitions in 2025

In 2025, the Finnish Tax Administration filed a total of 1,894 bankruptcy petitions, the amount is approximately 25% more than in the previous year. The Tax Administration accounted for 48% of all petitions in 2025. The total number of bankruptcy petitions is based on data from Statistics Finland (Chart 1).

Criminal matters

The Finnish Tax Administration filed 837 reports of an offence in 2025. In addition, there were 293 other criminal matters in which the Tax Administration was a party but the pre-trial investigation was based on a report by another party.

A criminal case may contain several criminal offences, which is why the number of criminal offences is higher than the number of criminal cases. For example, an accounting offence is commonly associated with tax fraud. The focus of criminal cases involving the Tax Administration is on aggravated tax frauds (Chart 2a).

Judgment according to court

The number stands for criminal matters involving the Finnish Tax Administration in which a judgment was rendered in 2025. It is not the same as the total number of judgments rendered, as more than one criminal matter may be considered under each criminal proceeding and sentencing phase (Chart 2b).

Tax debts

The statistics show all tax debts, regardless of whether they are accumulated in the shadow economy or by other taxable entities. The challenging economic situation is reflected in the amount of total tax debt. In the first months of 2026, the amount of total tax debt has been some EUR 400 million larger than one year before. Of particular note is the increase in tax debt among self‑employed individuals. From the main categories of tax debt, the most debt is seen in value added tax and income tax of individuals, which also includes amounts withheld by employers that have been not been filed and paid.

In Figure 1 (tax debt by main category), the amount of tax debt on 1 March 2026 is presented in main categories following the largest tax types. Figure 2 shows the breakdown of tax debt under the main categories in more detail, e.g. the division of excise duty debt between different types of excise duties. Figure 3 presents the total amount of tax debt on the review date of 1 March 2026. The figures can be filtered by tax year to identify the amount of unpaid taxes for each tax year.

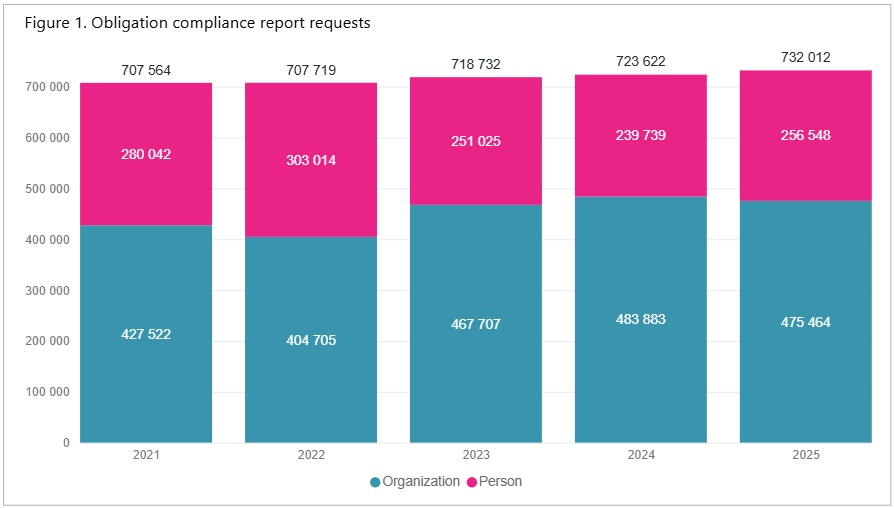

The Compliance Report supports decision-making

The information exchange between the authorities is at the core of the fight against the grey economy. It is difficult to make the right decisions without sufficient information on the financial standing of a subject or an applicant. The Compliance Report is an updated summary of the essential records held by the authorities. The Compliance Reports are issued by the Grey Economy Information Unit. The reports help authorities target and execute their control measures. The exchange of information between the authorities must always be based on the law.

The information on the Compliance Report is illustrative of the level of compliance of an organisation or a person with statutory obligations. The report includes information on activities, financial standing and compliance with obligations related to taxes, statutory pension, accident insurance and unemployment insurance contributions and fees levied by Customs.

The information on the Compliance Report is mostly based on information submitted by the subjects themselves. The report includes payroll information obtained from the Tax Administration, pension contribution information obtained from the Finnish Centre for Pensions and Customs information. The report also includes a possible extract from the enforcement register and information on bankruptcy and restructuring proceedings. The reports can be requested and received through an automated interface.

Act on Grey Economy Information Unit [.fi]› (in Finnish)