When you log in to MyTax, your tax-related letters will change from paper to electronic form automatically. Read more about the changes.

You can supplement the prepaid amount for 2025 with an additional prepayment

These instructions are for individual and corporate taxpayers alike.

If the tax withheld or prepayments made during the tax year do not cover the taxes for the entire year, you must pay the missing amount as back taxes after the tax assessment has been completed. If you want to pay the missing amount before that, you can request an additional prepayment. If you make an additional prepayment, you can reduce the amount of back taxes and the interest calculated on them.

When can I ask for a calculation for an additional prepayment?

Individual taxpayers (including the self-employed who have a registered business name) can request and pay an additional prepayment starting the tax year’s December. After you have submitted the request, you receive the Tax Administration’s decision concerning pre‑assessment enclosed with a bank transfer form.

Later, the opportunity to make an additional prepayment remains open until the Tax Administration finishes the assessment of the individual’s taxes for the year. Your tax decision for the 2025 tax year tells you the end date of your tax assessment. You will receive the decision in spring 2026. If you submit a request and determine a January due date for your additional prepayment, you do not have to pay late-payment interest with relief.

Corporate entities can request an additional prepayment only when the relevant tax year has ended.

During the tax year, no additional prepayments are accepted. You must instead ask for a new prepayment calculation or ask for a revised prepayment calculation.

For individual taxpayers, the tax year is the calendar year. Individuals can make additional prepayments without late-payment interest with relief up until the end of January.

If the due date of the additional prepayment is after 31 January, you will also have to pay late-payment interest with relief. Read more about late-payment interest with relief.

If the accounting period of a self-employed individual is other than the calendar month, the tax year comprises all the accounting periods that end during the calendar year.

For corporate taxpayers, the tax year is usually the accounting period. If the accounting period is not the calendar year, the tax year is determined by the end date of the accounting period. The tax year comprises all the accounting periods that end during the calendar year. Corporate taxpayers can make additional prepayments without late-payment interest with relief for a period of one month after the end date of the tax year.

If the due date of the additional prepayment is a later date, you will also have to pay late-payment interest with relief. Read more about late-payment interest with relief.

How to request and make an additional prepayment

You must submit a request for an additional prepayment before actually paying it, so the arriving payment can be allocated to the right tax. You will receive instructions for payment attached to the decision on prepayments. Neither the e‑invoice nor the web invoice can be used for paying additional prepayments.

For the self-employed and for other individual taxpayers, the Tax Administration starts accepting requests for 2025 additional prepayments on 7 December 2025.

Corporate entities can request an additional prepayment only when the relevant tax year has ended.

Please note: If you fill in the paper form to submit your request for additional prepayment and you prefer to avoid consequences of late payment, the completed form must arrive at the Tax Administration by 31 December 2025.

See the instructions

Minimum amount to pay as an additional prepayment is €170.00. Lower shortfall amounts must be covered in the form of a back tax when the year’s assessment of the taxpayer’s taxes is completed.

-

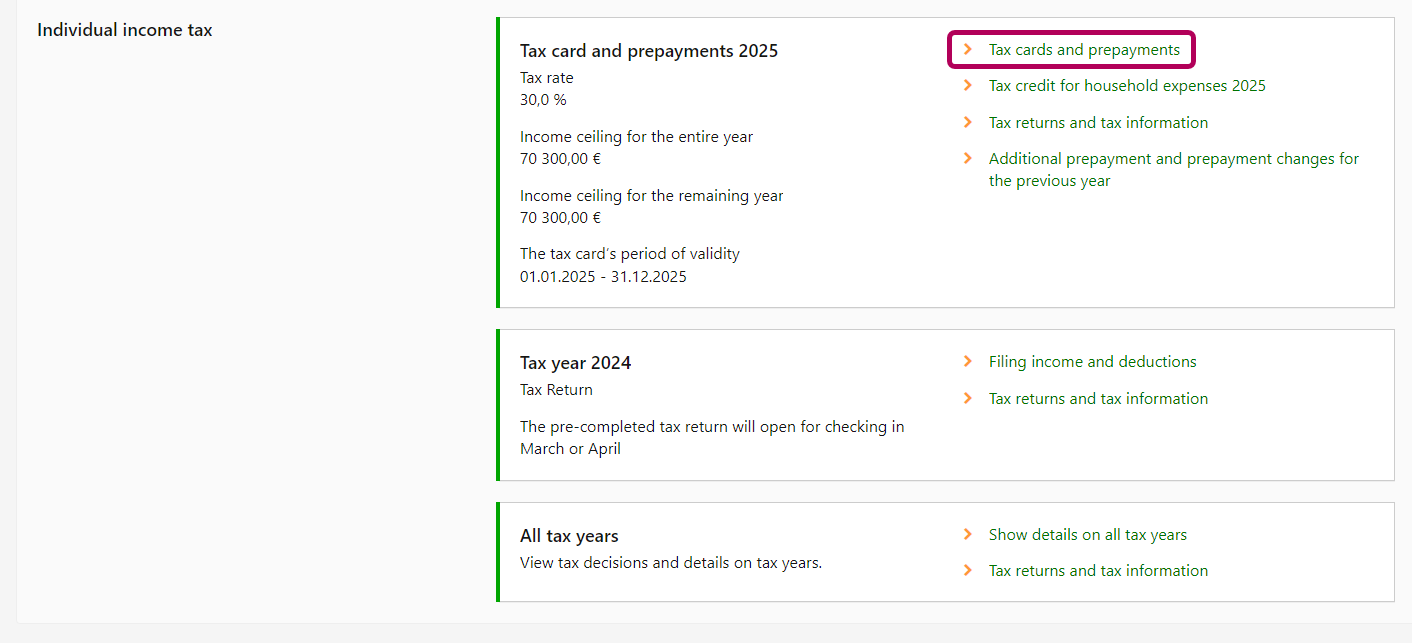

Go to the Individual income tax section, select Tax card and prepayments 2026 and click Tax cards and prepayments.

-

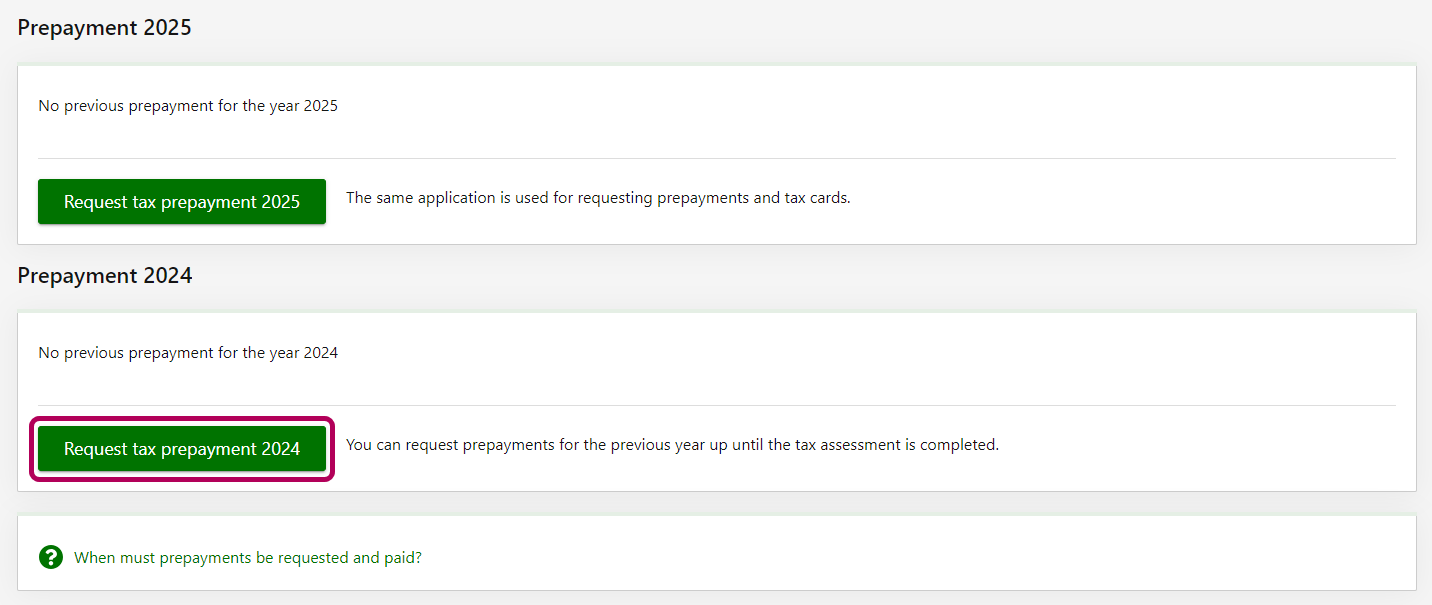

Scroll down all the way. Select Change the prepayment under Prepayment 2025.

-

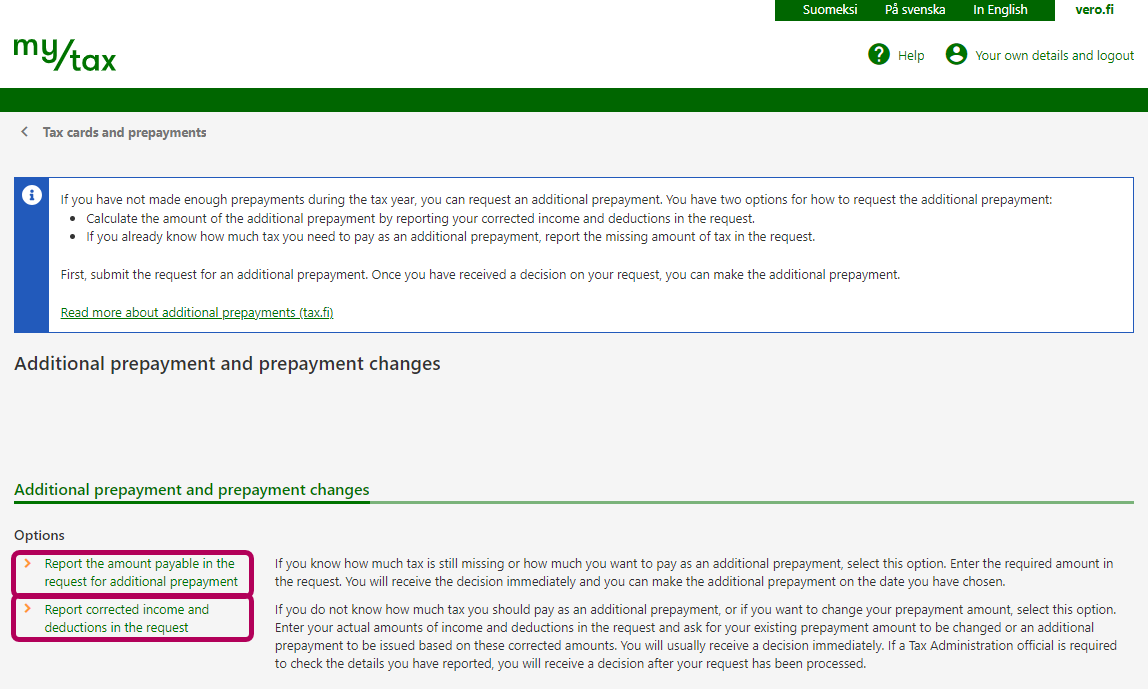

You can pay additional prepayments in two different ways. Choose the option most suitable for you:

- You may have estimated how much will be enough to pre-pay additionally. In this case, you can enter an exact sum of money when submitting the request. Click Report the amount payable in the request for additional prepayment.

- If you cannot estimate the exact additional prepayment, enter your actual amounts of income and deductions for the entire year. Click Report corrected income and deductions in the request. Complete the tax-card and prepayment request following these instructions, and MyTax will calculate the amount required: How to request prepayments — individual taxpayers

-

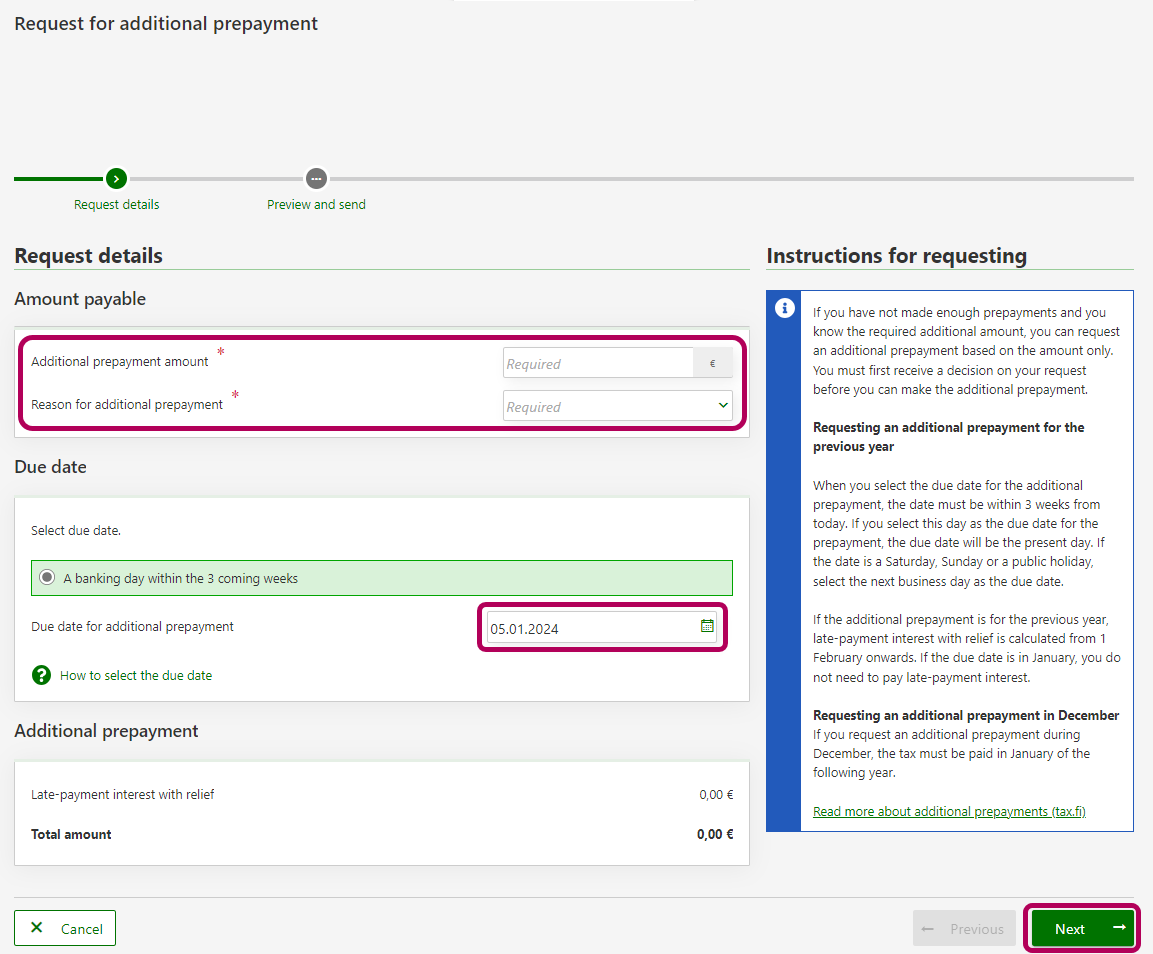

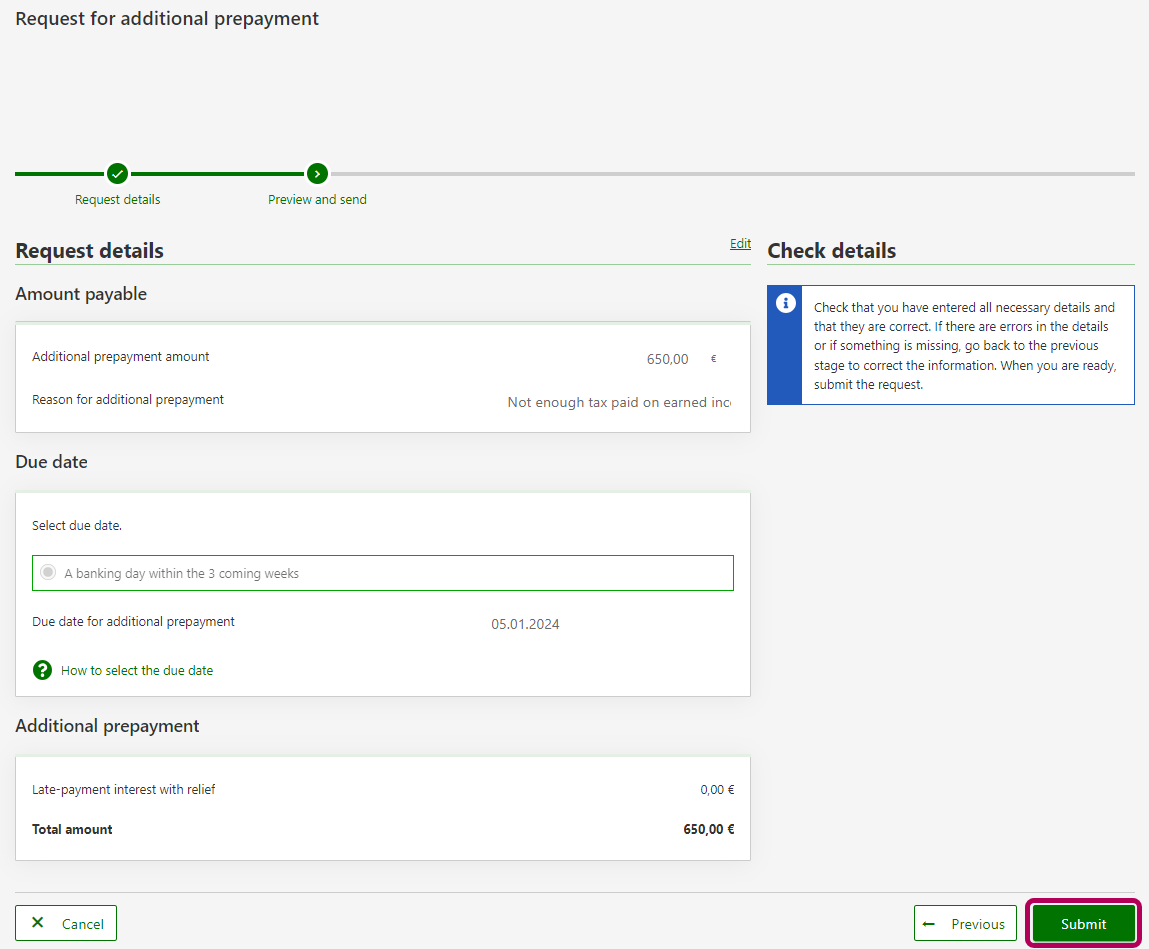

The request has 2 stages. You can see the stages in the breadcrumb trail at the top of the page.

Stage Request details:

Enter the amount of additional prepayment and select your reason for submitting the request. Typical reasons are “received rental income” and “sales profits and capital gains”.

Select a due date, a date in January.

In December, due dates can no longer be selected for the current year. The earliest due date that you can select is the first banking day in January. This means that if you request an additional prepayment at the beginning of December, you will in that case have to select a due date which is more than 3 weeks later in January.

Late-payment interest with relief is added to additional prepayments from 1 February.

-

The Preview and send stage: Please re-check all the information you entered. Click Edit or Previous to make corrections.

When everything is correct, click Submit. You get an acknowledgement of receipt.

-

You can open the prepayment decision concerning additional prepayment right away.

The decision is also archived in MyTax: How to find letters, tax decisions and tax certificates in MyTax

Instructions for payment are attached to the decision. You can make the additional prepayment in MyTax or your e-bank. If you choose to use your e-bank, you must enter the bank reference number for sending the payment. You receive this information together with the decision.

If you wish, you can pay the additional prepayment online straight away. To go directly to the online bank, click on Pay now. The payment details are pre-completed. The payment date is always the current day and the amount will be debited from your bank account immediately.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Minimum amount to pay as an additional prepayment is €170.00. Lower shortfall amounts must be covered in the form of a back tax when the year’s assessment of the taxpayer’s taxes is completed.

You wish to call our service number

- The number to call is 029 497 000 /Tax cards and prepayments (standard call rates, limited service in English).

- You can request an additional-prepayment calculation and pay the amount up to 31 January 2026. If you do that, you avoid having to pay interest.

- If the payment’s due date is a later date than 31 January, there will be interest for late payment added to it. Read more about late-payment interest with relief. Your request can be submitted and the payment made at any time up to the date when the Tax Administration completes your assessment for the 2025 tax year. Your tax decision for the 2025 tax year tells you the end date of your tax assessment. You will receive the decision in spring 2026.

You wish to use a paper form

- Fill in the form

- Application for tax card and tax prepayment (5010e) or

- if your income has consisted of capital gains, 9 Capital gain or capital loss (3013e).

- Please wait until you receive the Tax Administration’s decision containing a bank transfer form.

- Follow the instructions on the bank transfer form to pay the amount. The due date is generally three weeks from the day when the Tax Administration’s decision is dated.

- Note: When you send the paper form to the Tax Administration by 31 December 2025, we will send you a decision and the bank information for payment. The due date will be a date in January 2026. Allow enough time for postal delivery.

- On the condition that the due date for an additional prepayment you request is in January, you do not have to pay late payment interest with relief.

- If the payment’s due date is a later date than 31 January, there will be interest for late payment added to it. Read more about late-payment interest with relief. Your request can be submitted and the payment made at any time up to the date when the Tax Administration completes your assessment for the 2025 tax year. Your tax decision for the 2025 tax year tells you the end date of your tax assessment. You will receive the decision in spring 2026.

Minimum amount to pay as an additional prepayment is €500.00. Lower shortfall amounts must be covered in the form of a back tax when the year’s assessment of the taxpayer’s taxes is completed.

-

You are on the Your tax types tab. Click Make a prepayment request next to the correct year in the Corporate income tax section.

-

The request has 3 different stages. You can see the stages in the breadcrumb trail at the top of the page.

Stage Profit: Enter new details by source of income. Depending on the situation, you can enter profits for a business source of income, profits for a personal source of income, and profits for an agricultural source of income.

-

The Prepayment amount stage: MyTax shows you the amount to pay.

You must pay the additional prepayment in a single instalment. You can set the due date: it can be today’s date or any date within the upcoming 3 weeks. The due date has to be a banking day.

-

The Preview and send stage: When you have completed the request, click Submit.

You get an acknowledgement of receipt. You can open the prepayment decision concerning additional prepayment right away. The decision is also archived in MyTax: How to find letters, tax decisions and tax certificates in MyTax

Instructions for payment are attached to the decision. You can make the additional prepayment in MyTax or your e-bank. If you choose to use your e-bank, you must enter the bank reference number for sending the payment. You receive this information together with the decision.

Note: If you request an additional prepayment and would like to pay it on the last day of the month but the last day is a Saturday or Sunday, the due date will be the next business day. In other words, if you request an additional prepayment on Saturday 31 January, for example, the due date will be Monday 2 February. As a result, late-payment interest with relief will be calculated for two days even though you paid the additional prepayment on 31 January.

Frequently asked questions

Interest on an additional prepayment and interest on back taxes are calculated differently. When late-payment interest with relief is imposed on back taxes, €20 is subtracted from the interest. However, the amount subtracted is never higher than the amount of interest.

When late-payment interest with relief is imposed on an additional prepayment, no subtraction is made. If the tax is no more than approximately €880, it may be more beneficial to pay it as back taxes.

Example 1: Making an additional prepayment is more beneficial to the taxpayer

The prepayments you have made and the taxes that have been withheld on your income during the year do not cover your income taxes for the entire year. You receive a tax decision stating that you must pay €10,000 in back taxes.

Late-payment interest with relief is calculated on the back taxes as of 1 February. Late-payment interest accrues until the due date of the first instalment of the back taxes, in this case 1 August. The late-payment interest with relief is €10,000 x 182 days x 4.5% / 365 = €224.38. €20 is subtracted from the late-payment interest with relief calculated on the back taxes, so the amount you must pay is €10,204.38.

If instead of back taxes you request an additional prepayment of €10,000 with a due date of 2 April, for example, the late-payment interest with relief calculated on the additional prepayment is €10,000 x 61 days x 4.5% / 365 = €75.21. You do not have to pay any late-payment interest with relief at all if you pay all the required income taxes during the tax year or within one month from the end of the tax year.

Example 2: Paying back taxes is more beneficial to the taxpayer

You receive a tax decision stating that you must pay €850 in back taxes. Late-payment interest with relief is calculated on the back taxes as of 1 February. Late-payment interest accrues until the due date of the first instalment of the back taxes, in this case 1 August.

The late-payment interest with relief is €850 x 182 days x 4.5% / 365 = €19.07. Because the interest is less than €20, you do not have to pay it. The final amount of back taxes is €850.

If instead of back taxes you request an additional prepayment with a due date of 1 June, late-payment interest with relief is calculated on the additional prepayment as of 1 February. Interest accrues until the due date of the additional prepayment. The interest is €850 x 121 days x 4.5% / 365 = €12.68. The total amount payable is €862.68. In addition, you will have to pay the amount earlier than if you had waited for the due date of the back taxes.

Without a request, the payment will not be used for the additional prepayment. What happens to the payment depends on the reference number you used.

If you used a reference number for income tax

The Tax Administration will refund the payment to your bank account within approximately a week. If you have prepayments or back taxes falling due soon or if you have other overdue taxes or debt at enforcement, we will first use the payment to cover them.

If you used the reference number for self-assessed taxes or the general reference number for taxes

Request refunding of the payment in MyTax. If you have overdue taxes or debts at enforcement, we will first use the payment to cover them.