When you log in to MyTax, your tax-related letters will change from paper to electronic form automatically. Read more about the changes.

Your tax handbook in Finland

Find out essential tax facts for startup companies

Why Finland?

Combined with Finland’s strengths in sustainable innovation, AI, quantum technologies, green solutions, and its reliable, secure infrastructure, our environment forms a vibrant ecosystem where ideas scale quickly — and ambitious companies transform into global success stories!

- Currency in Finland: Euro (EUR/€) - yes, we are a part of the Eurozone

- Finland has one of the most competitive corporate tax rate in the EU and OECD: 20%

- Corporate forms: limited liability company, general partnership, limited partnership, co-operative, self-employed person, branch of foreign company

- Standards for accounting and financial statements: Finnish Accounting Standards (FAS) / International Financial Reporting Standards (IFRS; mandatory for listed companies)

- Technology superpower: In the home country of Oura, Wolt, ICEYE, IQM, Freepress.ai, Supercell, Rovio and many other game changers, you will be able to manage your tax matters online by using our world-class e-services in MyTax.

- A professional accountant can help you a lot with accounting and reporting obligations. We recommend using one

Finland offers a powerful launchpad for early‑stage companies, blending world‑class education, extensive public funding and strong partnerships with research institutions. The country’s accelerators, incubators, and regional development agencies further fuel growth through mentoring, facilities, and high‑value networks. Startups also gain global visibility through platforms like Slush and Nordic Innovation House.

Some of the top-notch public services available free of charge

- Business Finland - accelerator for global growth, innovation funding, exports and investing

- Set up a company and/or take care of IPR protection: Finnish Patent and Registration Office

- Your entry to working and settling in Helsinki area: International House Helsinki

- Soft landing services, access to financing, piloting platforms, matchmaking, business information etc. are available in many regions and cities in Finland. For instance, in Helsinki area: Helsinki Partners - Welcome to Helsinki!

Corporate taxation

Income tax rate for limited liability companies and other corporate entities: 20% Business income received by partnerships and private traders (self-employed individuals), on the other hand, is divided into earned income and capital income (see Individual taxation).

Tax liability: Finnish residents are taxed on their worldwide income. A company is tax resident if it is registered or established under Finnish law. Starting 2021, a foreign company may be regarded as tax resident in Finland if its place of effective management is in Finland.

Foreign companies' tax liability in Finland: As a main rule, foreign companies are liable for income tax in Finland if they have a permanent establishment in Finland. For example, a branch or a place of management can form a permanent establishment in income taxation (see also above what is said about having effective management in Finland).

Taxable income: Corporate tax is paid on the company’s profit. When taxable income exceeds deductible expenses, the profit is subject to income tax. As a main rule, expenses that are incurred for business purposes are deductible. If deductible expenses exceed taxable income, the loss will be carried forward to future years.

Accelerated depreciations for the years 2020-2025: depreciation of newly acquired machinery and equipment may be doubled for tax years 2020-2025 (depreciation percentage 50%).

R&D deduction incentive for the years 2021-2027: In addition to normal deduction (100%) on R&D costs, a super R&D deduction of 150% is available for tax years 2022-2027 on certain criteria.

General additional R&D deduction ("combined deduction"): The general additional deduction is 50% of the wage costs and expenses for purchased services, relating to corporate’s own R&D. The maximum deduction is €500,000 and the minimum deduction is €5,000 for one tax year. The extra additional deduction is 45% based on an increase in the R&D costs between the previous and current year’s expenses.

Losses in taxation: Tax losses are carried forward and offset against taxable income within the next 10 tax years.

Group contribution within group companies: Group companies may even out their taxable profits and losses under the preconditions set out by law ("group contribution"). Starting 2021, the final tax losses of a foreign subsidiary are, under certain conditions, tax deductible for a Finnish parent company.

Interest deduction limitations: Finland has implemented interest limitation rules in accordance with the EU regulations. Net interest expense is fully deductible up to €500,000. Interest expense exceeding this amount is deductible only up to 25% of the adjusted taxable income (EBITDA). However, net interest paid to other than group related parties will always be deductible up to €3,000,000. There is also a balancesheet exemption if the company fulfills a balance sheet ratio (equity/assets) test. Under this exemption, all interest expenses are deductible.

Dividends: Dividends received by a Finnish company are, with certain exceptions, exempt from tax when the company paying the dividend is a resident in Finland or in another EU/EEA country. Shareholders of a limited liability company are not taxed until they start withdrawing income from the limited liability company in the form of wages or dividends. Distribution of dividends does not cause tax consequences in the distributing company (although requirements to withhold tax may arise).

Participation exemption: Capital gains from the sales of shares are tax-free, with some exceptions, if the shares belong to fixed assets, the seller company owns at least 10% of the share capital of the entity, and the shares have been held for at least one year.

Income from abroad: Foreign-sourced income may be taxable in the source country as well as in Finland, which may lead to double taxation situation. In the assessment of corporate income tax, the Finnish Tax Administration generally eliminates double taxation with a credit method. Taxes that exceed the maximum credit can be used later during the five following years for any taxes payable on foreign income of the same type or source within the limits of maximum available credit.

Tax treaties: Finland has a comprehensive network of tax treaties with more than 70 countries (up-to-date income tax treaties are available on Finlex).

Transfer pricing: Transfer pricing is based on the arm’s length principle. Intra-group transactions must be based on the same terms as those used in transactions between unrelated parties. Intra-group transactions in multinational groups include e.g. sale of goods, provision of services, use of immaterial rights, sale of intangibles, and financing. The Finnish Tax Administration follows the approach of the OECD Guidelines for Transfer Pricing.

Tax returns and payment of taxes (limited liability companies): A limited liability company must file a tax return within 4 months from the end of the last calendar month of its accounting period. The tax return is recommended to be filed electronically, which is easy to do in the MyTax e-service. Income taxes are levied as prepayments during the fiscal year.

Tax year: The tax year is the company's financial year. If two or more financial years end during the same calendar year, the years are combined for tax purposes.

Value added taxation

Like everywhere else in the EU, VAT is paid on the sales of goods and services. The VAT basis is the price received from selling goods or services. The standard VAT rate is 25,5%. Finland has two reduced rates: 13,5% and 10%. There is also zero-rate sales, plus certain goods and services are exempt from VAT.

| VAT rate | Goods and services covered by the VAT rates (examples) |

|---|---|

| 25.5% | Standard |

| 13.5% | Food, restaurant, and catering services (alcohol 25.5%), passenger transport, books, medicines, entrance to sport and cultural events, accommodation |

| 10% | Newspapers, magazines |

| 0% | Sales of goods and services to other EU Member States and exports of goods |

Exempt from VAT: Social, healthcare, medical services, public education and similar services, financial and insurance services.

Registration for VAT: All companies with VAT liable operations whose annual turnover subject to VAT exceeds €20,000 must be registered for VAT. Companies usually enter the VAT register when they file their start-up notification, but it can also be done later. Registration forms are available online on the Business Information System website.

Filing and paying VAT: Companies that are registered for VAT must regularly file VAT returns. Returns can be filed in the MyTax e-service. Companies must calculate, file, and pay VAT on a monthly basis in MyTax at their own initiative. The tax period is usually one calendar month. The general due date is 12th day of the second month following the end of the tax period. If the company’s turnover is no more than €100,000 per calendar year, VAT can be filed and paid in quarterly periods. If turnover is no more than €30,000, VAT can be filed and paid in quarterly periods or once a year.

| Tax reporting period | Turnover threshold | Tax period example | Due date for tax return and payment |

|---|---|---|---|

| Calendar month | No turnover threshold | 1/2026 | 12 March 2026 |

| Calendar quarter | Max. €100,000 | 1-3/2026 | 12 May 2026 |

| Calendar year | Max. €30,000 | 1-12/2026 | 1 March (28 of February is Sunday) 2027 |

Note that when the 12th day of the month is a Saturday or Sunday, the return and the payment must arrive at the Tax Administration on the next business day.

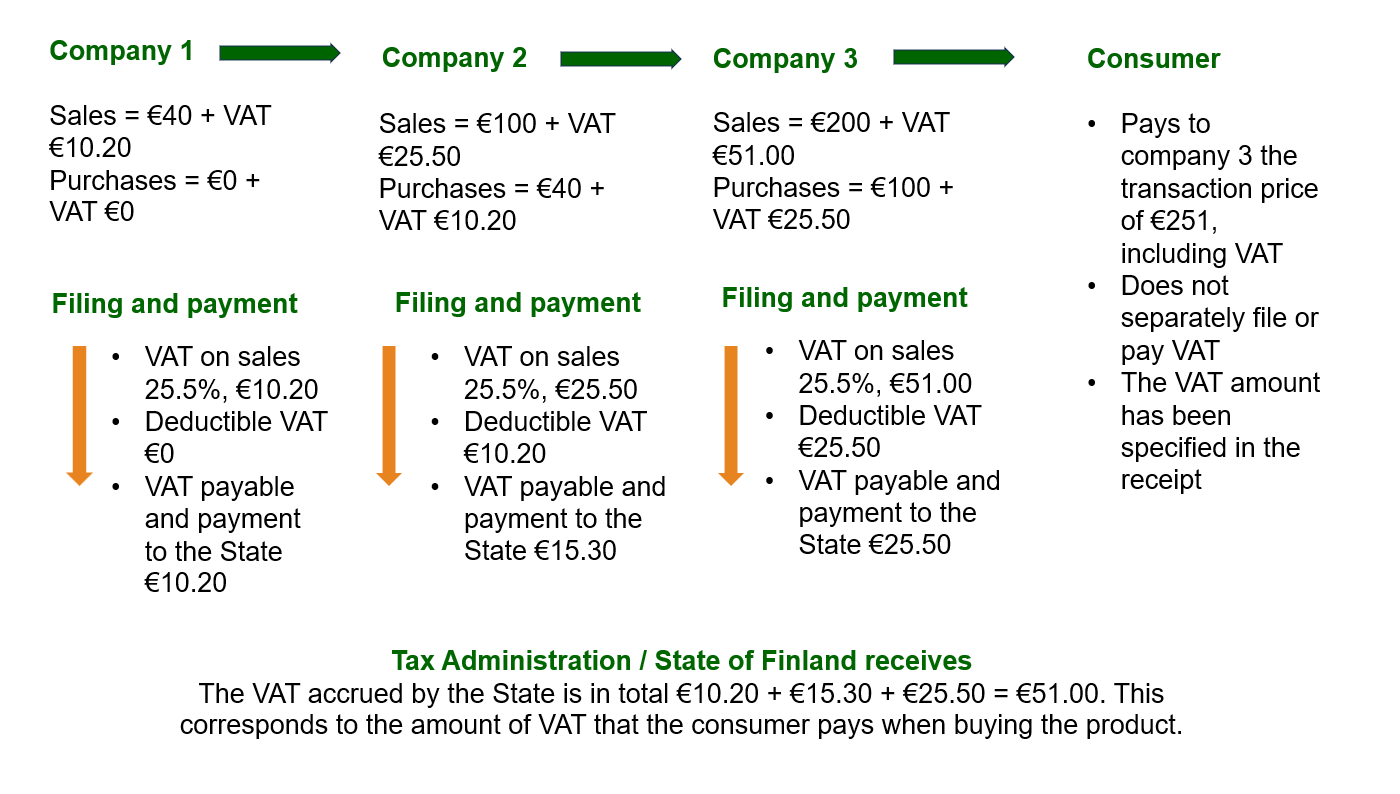

Principles of VAT: VAT is ultimately paid by the end consumer. Companies act as the collectors and remitters of VAT by paying VAT on their sales and by deducting VAT from their purchases relating to VAT liable operations. The chart below demonstrates a simple chain of sales reflecting the logic of VAT when filing and payment are allocated between different companies.

In certain situations – for instance, when a company exports products from Finland to third countries – deductible VAT may exceed the payable VAT. In these circumstances, the company receives deductible VAT on their tax account.

Example: A company purchases products in Finland from a Finnish seller. The deductible VAT is €100. All products are then exported to third countries. Because exports are taxed at 0% VAT, the company's VAT account will only contain the deductible VAT, which means that the company receives a refund (€100) from the Tax Administration.

Excise duty

Harmonised excise duties in the EU Member States are regulated by a directive. The directive is implemented in a national legislation. The harmonised excise duties apply to alcohol and alcoholic beverages, most tobacco products, liquid fuels, electricity and certain other fuels. National non-harmonised excise duties are levied on soft drinks, beverage packages, waste delivered to municipal landfill sites and mined minerals.

Excise duties are indirect taxes on the consumption or sales of specific products. Excise duties are collected for fiscal reasons, but they are also intended to promote social and health policy objectives as well as environmental and energy policy goals. Excise duties are levied on products manufactured in Finland and products imported into Finland. Excise duties are product-specific, meaning that the amount of duty paid is based on the number of products consumed or supplied for taxable use.

Excise duty returns can be filed in the MyTax e-service. Companies must calculate, file, and pay excise duties in MyTax at their own initiative. The filing and payment schedule depends on whether the company is liable to pay excise duty regularly or casually. Excise duty authorisations can also be filed in MyTax.

Being an employer

- Regular employers must register into the Tax Administration’s register of employers.

- A company acting as an employer is obligated to withhold tax and health insurance contributions from the employee’s wage or salary and remit them to the Tax Administration.

- In addition, an employer needs to arrange mandatory insurance contracts for employees, including a pension insurance contract as defined by law. Pension and insurance contributions are paid to the insurance companies selected by the employer.

- Tax withholding is based on the tax card or tax-at-source card that the employee has provided to the employer. A tax card can be updated whenever it may be necessary.

- Employers must report earned income details to the Incomes Register within five days from the payment.

- Employers can pay tax-exempt travel expense allowances if certain conditions are met.

- Fringe benefits (phones, cars, etc.) are considered taxable earned income.

- When a Finnish employee works abroad, their domestic employer still has obligations in Finland.

- When a foreign employee arrives in Finland, their taxpayer status (e.g. residency) must be taken into account in tax assessment.

- Unlisted companies can issue shares to their employees without tax on a taxable benefit, if the price charged from every employee is not lower than the mathematical value of the shares (close to the so called substance value in practice).

Individual taxation

Resident taxpayers

In general, a private person is a resident taxpayer in Finland if their home and place of residence is in Finland. In addition, any person who stays in Finland for longer than 6 months is considered a resident for tax purposes. A resident taxpayer pays income tax to Finland on the income they received from anywhere in the world. This may be limited by a tax treaty if the person is also a resident in another country.

Earned income (e.g. salaries and wages) is subject to progressive state income tax, municipal income tax, and the health insurance contribution. The employer withholds these payments from the employee's pay according the tax rate stated on the employee's tax card.

Tax tip: the tax percentage calculator is a useful tool for estimating the amount of taxes on certain income. In addition, the employer withholds pension and unemployment insurance premiums (approximately 8.19%) from the pay. Please note that the tax card is easy to update when estimated taxable income is changing.

Example of a person who lives in Helsinki

| Yearly salary | Tax rate | Pension & unemployment insurance contributions |

|---|---|---|

| €30,000 | 8.5% | 8.19% |

| €50,000 | 19.00% | 8.19% |

| €100,000 | 30.0% | 8.19% |

Capital income (e.g. capital gains, dividends, rental income) is subject to tax at the rate of 30%, or 34% on the part exceeding €30,000.

As a resident taxpayer a person must file a Finnish tax return in the spring following the tax year.

Key employees arriving from abroad can apply for a flat-rate tax of 25% instead of progressive income tax on certain criteria (starting from the salary paid from 1 January 2026).

Non-resident taxpayers

A private person is a non-resident taxpayer in Finland if they live abroad and stay in here for 6 months or less. A non-resident taxpayer pays income tax to Finland only on the income received from as ource in Finland. However, Finland's right to tax may be limited by a tax treaty.

Earned income (e.g. salaries and wages) received by a non-resident taxpayer is subject to tax at source (35%). However, if the person's country of residence is another EU country, Norway, Iceland or Liechtenstein, or a country that has a tax treaty with Finland, the person can request to be taxed progressively.

Capital income (e.g. dividends) is generally subject to tax at source (30%), but tax treaties typically narrow it down to 0-15%.

If a tax at source is withheld from income, that is final tax, and no tax declaration is needed. If a person requests the non-residents progressive taxation, they must file a Finnish tax return in the spring following the tax year.

Other taxes

- Transfer tax: as a main rule, the recipient pays 1.5% of transfer tax on the disposal of shares, or 3% in the case of real estate

- Wealth tax: Not in use

- Real estate tax: General rate of real estate tax is max. 2%

- Inheritance and gift tax: Progressive tax scale

With tax money Finland pays for:

- free health and medical care

- free schools

- children's daycare

- higher education

- facilities for sports, arts, and hobbies

- environmental protection