{kind=link}

{kind=link}

{kind=link}

How to make corrections

Payments

Scam messages have been sent out in the Tax Administration’s name. Read more about scams.

This guidance tells you how to submit a VAT return for a company.

Note: You must file a VAT return for every tax period, even if your company has not had any VAT-liable activities during the period: for example, if you have interrupted your activities or there is a break in the company’s seasonal activities.

File your VAT returns in MyTax. You can use the paper form only in exceptional cases. You can find the link to the form at the end of the page.

Log in to MyTax (opens in a new window).

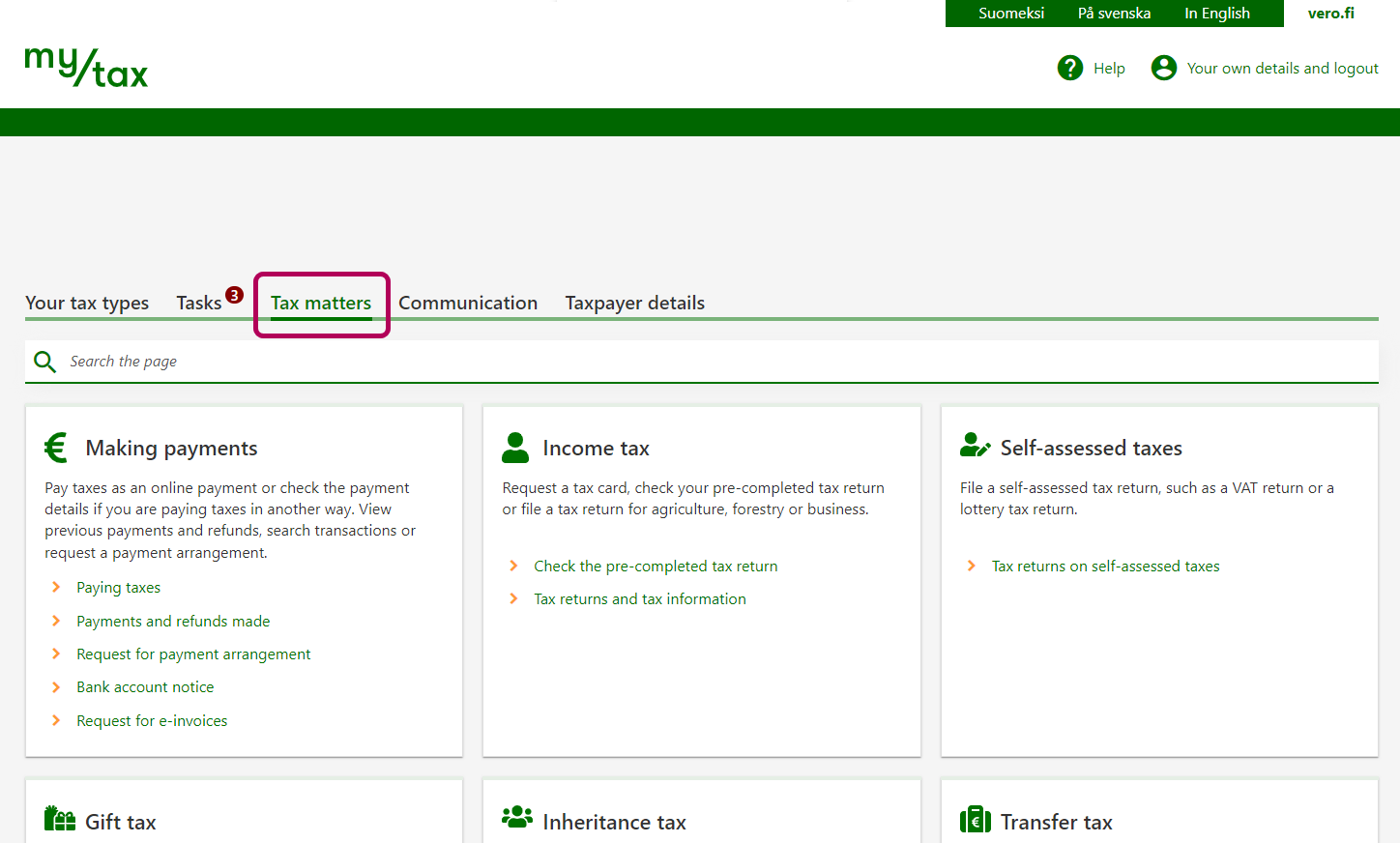

Open the Tax matters tab on the home page. Go to Self-assessed taxes and click Tax returns on self-assessed taxes.

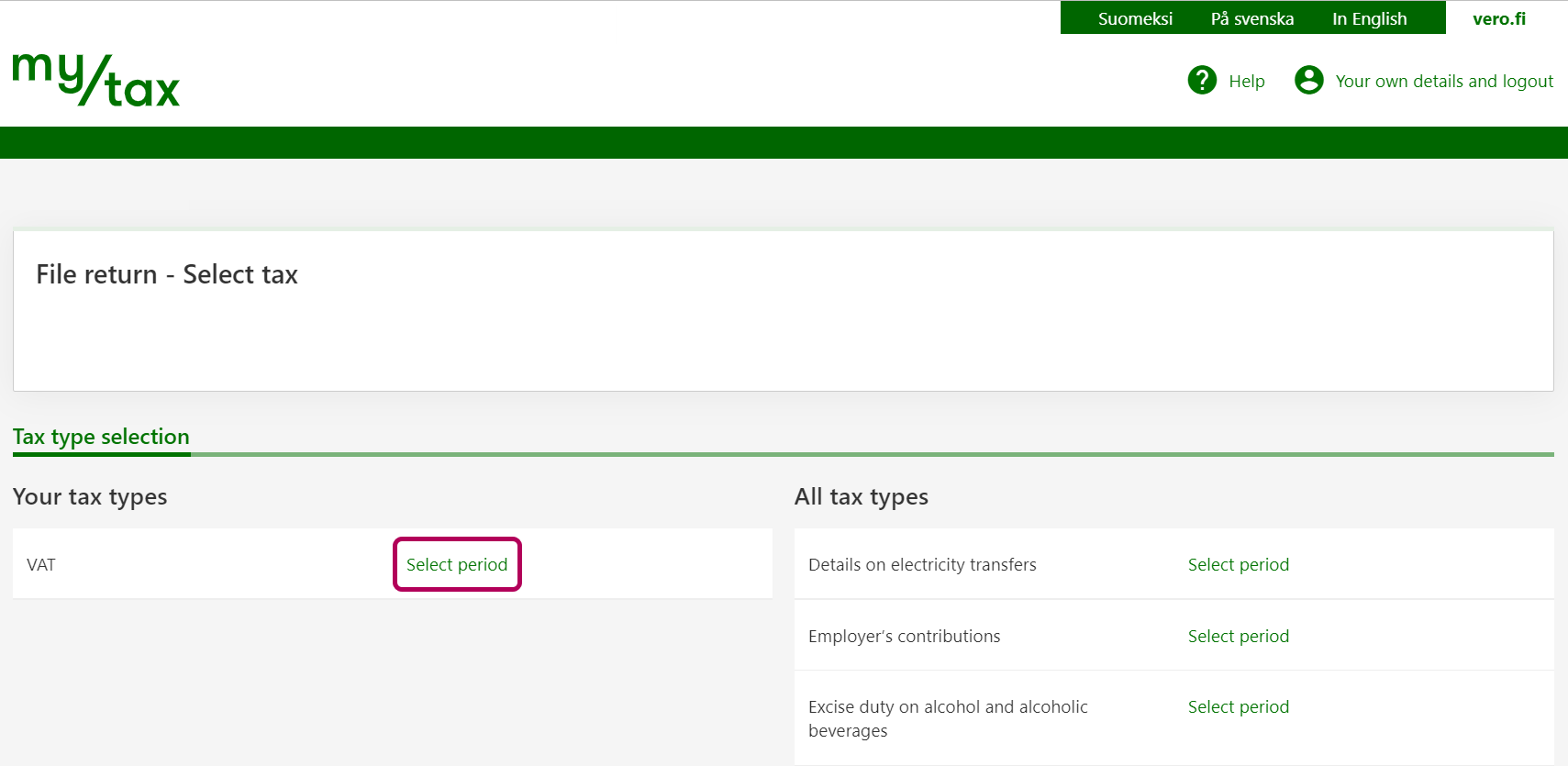

Under “VAT”, click on Select period.

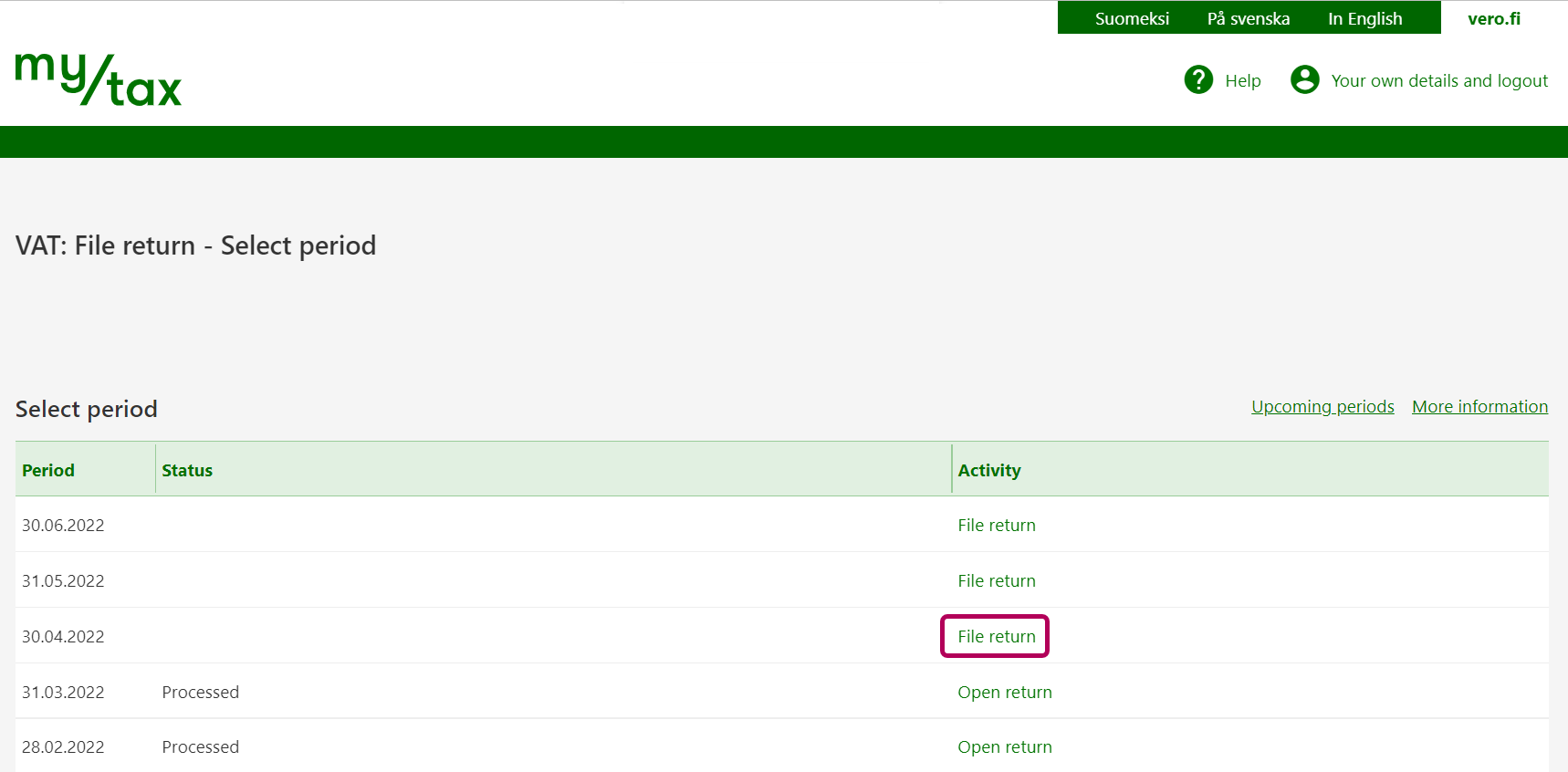

Click File return for the tax period for which you wish to file a return. Example: If your company’s tax period is a calendar month and you want to file VAT for December 2021, select the period ending on 31 December 2021.

The list shows the tax periods that have ended. If you want to file a return for an ongoing or a future tax period, click Upcoming periods to see more periods.

The VAT return has 2 stages: Return details, and Preview and send. In stage 1, enter Return details. Then proceed to stage 2 Preview and send: Check that the details are correct and send the return by clicking Submit.

If you company does not have any VAT-liable activities during the tax period, report it

You can file a return on interrupted activities 6 months in advance.

Note: If your company has sales where VAT is 0% but the VAT on associated purchases is deductible, do not file a “No activities” return. In such a case, report the sales under "Turnover taxable at zero VAT rate".

Read more: Termination of VAT-liable activities.

You must file a VAT return for every tax period, even if your company has not had any VAT-liable activities during the period: for example, if you have interrupted your activities or there is a break in the company’s seasonal activities.

When you are filing a VAT return in MyTax, the service asks you whether you are filing VAT on a cash basis. The default selection is “No”.

Change the answer to “Yes” if you are liable to keep accounting records and have chosen the cash accounting approach. The cash accounting approach means that you allocate both the VAT you pay and the VAT you can deduct to the month when you received a payment from the buyer or when you paid for a VAT-deductible purchase.

The cash accounting approach can be used, for example, by

Read more about cash-based VAT (available in Finnish and Swedish, link to Finnish)

If you file VAT information on paper, indicate the tax period as follows:

In addition, enter the year for the tax period in four digits.

Enter VAT on goods and services sold in Finland, specified by tax rate.

The general VAT rate is 24%. The reduced VAT rates are 14% and 10%. Current VAT rates.

Example: If your sales (VAT 24%) without VAT are €19,310.00 (= taxable amount), then the 24% VAT you must report is 24% × €19,310.00 = €4634.40. Read more about how to calculate VAT

Report here VAT payable on items such as:

goods bought from a foreign party who is not liable for VAT in Finland because the reverse charge mechanism is applied

services bought from a foreign party who is not liable for VAT in Finland because the reverse charge mechanism is applied

Report VAT on EU purchases of services only if the services are not covered by the general provision. Examples include VAT on real estate related services, passenger transport services and travel agency services. Read more about the general provisions and the provisions on the country of supply (chapter 7) (available in Finnish and Swedish, link to Finnish)

Report VAT on purchases of services from outside the EU regardless of whether or not the services are covered by the general provision.

emission allowances bought under the VAT reverse charge mechanism in Finland, i.e. the buyer pays the VAT.

Please note that if the emission allowance was bought in another EU country, it must be reported in “Tax on services purchased from other EU Member States” instead.

Do not report here the following information:

Note: As of 1 July 2021, the VAT special scheme has expanded into the One Stop Shop, a special scheme that covers all the goods and services sold to consumers in the EU. None of your sales reportable under a special scheme must be included in this section of the VAT return. Read more: VAT special scheme (One Stop Shop)

Enter the VAT on goods bought from parties that are liable for VAT in other EU countries (intra-Community acquisitions).

Intra-Community acquisition means that

You can calculate the amount of VAT by multiplying the price without VAT by the VAT rate applied to the goods purchased. If several VAT rates (24%, 14% and 10%) apply, add the amounts of tax together and enter the sum total.

Example: Your company has bought goods from other EU countries (intra-Community acquisitions) for €18,000. The VAT rate applied is 24%. The amount of VAT that you should report is 24% x €18,000 = €4,320. You can deduct the VAT on intra-Community acquisitions on the same terms as you can deduct the VAT included in goods you have bought in Finland.

If the VAT is deductible, also report it under "Tax deductible for the tax period". Enter the purchase price of intra-Community acquisitions under “Purchases of goods from other EU Member States”.

Read more: VAT and EU goods trade (available in Finnish and Swedish, link to Finnish)

Enter here the VAT on services bought from VAT-liable parties in other EU countries when the services purchased are in accordance with the general provision and the VAT is paid to Finland based on the reverse charge mechanism.

In addition, enter the VAT payable on an emission allowance bought in another EU country.

When the services bought are not in accordance with the general provision, enter the VAT under “Tax on domestic sales by tax rate” if the country of supply is Finland.

Read more about the general provisions and the provisions on the country of supply (chapter 7) (available in Finnish and Swedish, link to Finnish)

Note: If your company buys construction services or leases employees for construction services in Finland and the seller is from another EU country, report VAT under “Purchases of construction services and scrap metal (reverse charge)”.

To calculate the amount of VAT, multiply the price without VAT by the VAT rate applied to the purchase. If several VAT rates (24%, 14% and 10%) apply, add the amounts of VAT together and enter the sum total.

Example: Service purchases from other EU Member States amount to €10,000. The VAT rate applied is 24%. The amount of VAT is 24% x €10,000 = €2,400. You can deduct the VAT on the same terms as you can deduct the VAT included in services you have bought in Finland. In other words, it is included in the VAT deductible for the period.

Report the VAT on imports, i.e. the VAT on goods imported from outside the EU. Report all imports: there is no minimum euro threshold.

To calculate the amount of VAT, multiply the taxable amount by the VAT rate applied to the goods. If several VAT rates (24%, 14% and 10%) apply, add the amounts of VAT together and enter the sum total.

If the VAT is deductible, also report it under "Tax deductible for the tax period".

Example: Imports of goods from outside the EU total €80,000. The VAT rate applied to the goods imported is 24%. The amount of VAT is 24% x €80,000 = €19,200. You can deduct the VAT on these imports on the same terms as you can deduct the VAT included in goods you have bought in Finland. In other words, the tax is included in the VAT deductible for the period. A condition is that the purchase was made for business activities that qualify for the deduction.

In some circumstances, imports operated in Finland are exempt from tax (§ 94 – § 96 and § 72h of the Value Added Tax Act). In such a case, leave this section and section “Tax deductible for the tax period” blank. However, you must still report the basis of VAT for these imports under “Imports of goods from outside the EU”.

Read more

Imports between the Åland Islands and mainland Finland. Read more about the Åland Islands tax border and importing goods

Report VAT on such purchases of construction services and scrap metal to which the reverse charge mechanism is applied.

Also report here

Calculate the VAT by multiplying the purchase price without VAT by the VAT rate of 24%.

Also report the purchase prices for the above purchases under “Purchases of construction services and scrap metal”.

Note: If you have bought scrap metal from another EU Member State and it is regarded as an intra-Community acquisition, report the VAT under "Tax on goods purchased from other EU Member States".

Read more:

Enter the total amount of VAT deductible for the period.

You can deduct the VAT included in the purchase price of goods or services if

Note: When reporting the deductible amount of VAT for the tax period, do not enter a minus sign (-) in front of the number. Use the minus sign only if you have previously reported too much deductible VAT and are now making a correction.

Deductible taxes related to taxable business activities may also include

the Finnish VAT included in your purchases of goods and services, if you had bought the goods or services in order to support your sales reportable in a VAT special scheme, and the company is a VAT-registered company in Finland. Read more: VAT special scheme (One Stop Shop)

VAT included in the purchases is deductible only insofar as the goods or services purchased have been used for activities that qualify for the deduction of VAT. VAT is not deductible if the goods or services are intended for private use, for activities that are not subject to VAT or for use in activities where the right to make deductions is restricted. Purchases related to activities that do not fall within the scope of the Value Added Tax Act are also not deductible.

Read more:

You can get relief from all or part of your VAT, if your net sales (turnover) is less than €30,000 during the accounting period (12 months).

Request it on the accounting period’s or calendar year’s last VAT return, depending on your tax period.

MyTax calculates the VAT relief automatically when you enter your turnover qualifying for VAT relief and the amount of VAT.

You can calculate the turnover that qualifies for tax relief and the amount of VAT by using the VAT relief calculator. The calculator takes into account that some of your sales and VAT do not qualify for the relief.

If you are filing on paper, also remember to enter the amount of tax relief.

MyTax calculates the total VAT for the tax period. If the total VAT is negative, i.e. you qualify for a VAT refund, you can see this in your account balance in MyTax only after the Tax Administration has confirmed the refund.

If you are filing on paper, first add together

Then subtract the VAT deductible for the tax period and any tax relief you quality for (only on the accounting period’s or calendar year’s last VAT return).

If the total VAT is negative, i.e. if you qualify for a tax refund, enter the amount of refund at Negative tax that qualifies for refund. Add the negative sign (-) for the total VAT.

Note: passenger transport services provided in Finland, from 1 Jan 2023 to 30 Apr 2023 (including taxis, train, bus, air travel and maritime passenger transport)

Report here the supply of tax-exempt goods or services if you are entitled to deduct the VAT on associated purchases (in other words, the purchases have been made for business activities that are subject to VAT). Such supply includes

Also report here supply of new means of transport to private individuals in another EU country.

When you calculate your turnover subject to 0% VAT, do not include the following:

Report here the total value of your Intra-Community supply, i.e. the sales of goods to VAT-liable buyers in other EU countries. A condition for intra-Community supply is that the goods are transported from Finland to another EU country.

The value of sales is the price based on an agreement between the seller and the buyer, including all the surcharges charged from the buyer (for example, invoice fees, postage or other delivery costs). Also include any transport costs that your company has charged for the delivery.

Intra-Community supply also includes the movement of goods from one EU country to another EU country in order to be sold there. Report here, for example, the value of goods moved from Finland to Germany in order to be sold there. Note that the movement of goods to a call-off stock is not regarded as intra-Community supply and should not be reported here. It must always be reported separately.

In the case of triangulation, do not report the second sales transaction on your VAT return. Report it on the VAT Recapitulative Statement only.

If you sell goods to consumers, report the sales under “VAT on domestic sales by tax rate”. Exceptions include the supply of new means of transport to private individuals in other EU countries. Report such supply under “Turnover taxable at zero VAT rate”.

Note: Also remember to report intra-Community supply to another EU country on the VAT Recapitulative Statement.

Read more

Enter the total value of sales taxed in the buyer’s country in accordance with the general provision on sales between VAT-liable parties (buyer from an EU country other than Finland).

The buyer of the service pays the VAT based on the reverse charge mechanism in the EU country to which the service is supplied.

If the service supply is exempt from VAT in the other EU country, do not report it in this field. In such a case, report it under "Turnover taxable at zero VAT rate".

The provision on the country of service supply is that services sold to a small business are taxed in the country where the buyer is established. However, the general provision is not applied to the following services:

Supply of services that are not covered by the general provision to small businesses is taxed in the buyer’s country, so you should report it under “Turnover taxable at zero VAT rate”.

If you sell emission allowances to a business in another EU country, report these sales here.

Note: Also remember to report intra-Community supply to another EU country on the VAT Recapitulative Statement.

Read more

If you sell services to consumers, report the sales under “VAT on domestic sales by tax rate”.

Enter the total value of goods bought from EU countries other than Finland, i.e. your intra-Community acquisitions (enter the purchase price without VAT). Also report intra-Community acquisitions exempt from tax.

A condition for intra-Community acquisitions is that the goods are

Report VAT paid on the goods purchased under:

Read more: VAT and EU goods trade (available in Finnish and Swedish, link to Finnish)

Enter the total value of such services bought from other EU countries on which the VAT is paid to Finland based on the reverse charge mechanism in accordance with the general provision applied in the country of supply of services. According to the general provision, the sales to small businesses are taxed in the country where the buyer is established.

In addition, enter the total value of emission allowances bought in another EU country.

Report VAT paid on the services purchased under:

Do not report here the following information:

Enter the total value of goods imported from outside the EU, i.e. the taxable amount. You can calculate the taxable amount based on the information provided in the customs clearance decision. If the customs clearance decision changes such that the taxable amount and the information affecting the tax change, remember to correct your VAT return.

Report the information on the VAT return you file for the tax period during which the customs clearance decision was issued. The period is determined by the date printed on the decision.

Allocate the corresponding VAT deduction to the same month. Report VAT on imports under:

In some circumstances, imports operated in Finland are exempt from tax (§ 94 – § 96 and § 72h of the Value Added Tax Act). Even in that case, report the VAT for imports here.

Example: Imports of goods from outside the EU total €80,000. The goods imported are dentures, and their imports are exempt from VAT (§ 36, paragraph 3 and § 94–96 of the Value Added Tax Act). However, report the taxable amount for these imports under “Imports of goods from outside the EU”. Do not report anything under “Tax on imports of goods from outside the EU" and “Tax deductible for the tax period".

Read more:

Imports between the Åland Islands and mainland Finland. Read more: Åland Islands tax border and importing goods

When services are bought from a small business located outside the EU, the taxable amount is not entered in the VAT return. However, report the VAT on these purchases, specified by tax rate, under “Tax on domestic sales”. If the VAT is deductible, also report it under “Tax deductible for the tax period”. Whether or not the services are covered by the general provision is irrelevant.

Read more: Value added taxation of foreign service trade, chapter 9

Report here such supply of construction services to which the reverse charge mechanism is applied.

Also report the total value of scrap metal and metal waste to which the reverse charge mechanism is applied. However, if scrap metal has been sold to another EU country and the sale qualifies for intra-Community supply, do not report it here but under “Sales of goods to other EU Member States”.

Read more:

Report here such purchases of construction services, scrap metal and metal waste to which the reverse charge mechanism is applied.

Also report the following:

Note: If you have bought scrap metal in another EU country and the purchase qualifies for an intra-Community acquisition, do not report the purchase here. Report the purchase under “Purchases of goods from other EU Member States”.

Read more: