When you log in to MyTax, your tax-related letters will change from paper to electronic form automatically. Read more about the changes.

This is an unofficial translation. The official guidance is drafted in Finnish (Osingonsaajan itse antaman ilmoituksen sisältö, voimassaolo ja luotettavuuden todentaminen, record numer VH/2706/00.01.00/2022) and Swedish (Innehåll, giltighet och verifiering av tillförlitlighet av dividendtagarens självdeklaration, record number VH/2706/00.01.00/2022) languages.

This guidance concerns the Investor Self-Declaration and the procedure with which a non-resident dividend beneficiary can be granted tax treaty benefits when paying dividends from a publicly listed company (Section 10b of the Act on the Taxation of Nonresidents' Income (627/1978)).

This guidance concerns the procedure with which a tax at source benefit can be granted based on Investor Self-Declaration when paying the dividend. The taxation on nonresident taxpayers’ dividends is discussed in the guidance Payments of dividends, interest and royalties to nonresidents.

This guidance has been updated 26.9.2022, when

- the structure and the form of the guidance have been clarified, and speficiations, that do not change the requirements or tighten interpretations, have been added to the guidance.

- a new Chapter 6 has been added to the guidance, to which the parts concerning Authorised Intermediary's tax liability that were previously in Chapter 5 have been transferred for the purpose of clarification.

- guidance on situations, where an Authorised Intermediary uses a service provider to carry out their obligations, has been added to Chapter 7.

- practical examples have been added to the guidance.

- the part concerning the dividend payor has been removed from the guidance insofar the payor's obligations are discussed in the guidance Withholding tax at source on dividends, interest and royalties, and the payor’s obligations.

Explanatory note for the English version

In this guidance, the term 'dividend beneficiary' refers to the shareholder, i.e. the owner of the shares, who has the right to the dividend on the record date in accordance with the Finnish Companies Act (624/2006). The term 'beneficial owner' is used when referred specifically to the beneficiary entitled to the dividend in accordance with the tax treaty between Finland and the beneficiary's country of residence.

1 Foreword

According to Section 10b(2) of the Act on the Taxation of Nonresidents' Income (627/1978, Tax at Source Act), the dividend provisions of an international tax treaty may be applied if the payor or the Authorised Intermediary (hereinafter also AI) has taken reasonable measures to determine the beneficiary's country of residence and to verify that the criteria for the applicability of the tax treaty are fulfilled. The provision is applied when paying dividends from a publicly listed company, as referred to in article 33 a of the Income Tax Act, to nominee registered shares (section 10 b(1) of the Tax at Source Act)

According to Section 10b(4) of the Tax at Source Act, the following can be deemed as reasonable measure to ascertain the facts about the beneficiary’s country of residence: a tax-at-source card issued by the Finnish Tax Administration, a certificate issued by the tax authority of the beneficiary’s country of residence, or an Investor Self-Declaration, which contains the necessary information for taxation at source. The Investor Self-Declaration (hereinafter ISD) must be sufficiently reliably documented and consistent with the information in the possession of the AI on the dividend beneficiary.

According to the legislative materials (HE 282/2018 vp, pp. 37-38), the ISD means an Investor Self-Declaration in accordance with the OECD's Treaty Relief and Compliance Enhancement (hereinafter TRACE) system. The ISD forms in accordance with the TRACE system and their contents are described in the OECD's TRACE Implementation Package (hereinafter TRACE IP) document. TRACE IP and other documents concerning the TRACE system are available on the website of the OECD.

The Tax Administration has issued further provisions under Section 10b(4) with its decision on the contents and period of validity of the Investor Self-Declaration, and the procedure with which its reliability is verified (dnro VH/4332/00.01.00/2020, hereinafter 'ISD decision'). An ISD, which the payor or an AI has verified to be reliable as defined in the Tax Administration’s ISD decision, is also evidence on the requirements for applying a tax treaty.

Instead of the ISD, the beneficiary's country of residence can alternatively be ascertained based on a tax at source card or a certificate of residence. The procedure to be followed in these situations is discussed in Chapter 10 of this guidance.

The ISD decision is applied only in situations where tax treaty benefits are granted to a non-resident dividend beneficiary. The ISD decision can nevertheless be utilised in situations, where tax at source relief is granted based on national legislation. The requirements for applying tax at source relief based on national legislation are discussed in Chapter 8 of the guidance.

If no tax treaty is applied when paying the dividend or the dividend is not exempt from tax at source under national legislation, tax at source is 20 % on dividend paid to a corporate entity and 30 % on dividend paid to a beneficiary other than a corporate entity (Section 7(1)(2 and 4) of the Tax at Source Act). If the payor or the AI cannot cannot report the identifying information of the dividend beneficiary to the Tax Administration on an annual information return, tax at source of 35 % must be withheld on the dividend paid to nominee registered shares (Section 7(2) of the Tax at Source Act). The requirements for applying the tax at source rates in accordance with Section 7 of the Tax at Source Act are discussed in more detail in the guidance Withholding tax at source on dividends, interest and royalties, and the payor’s obligations (Chapters 1.3 and 2.2).

This guidance discusses the responsibilities of the dividend beneficiary and the responsibilities of the AI, when the procedure in accordance with the ISD decision is applied for investigating and identifying a dividend beneficiary who is a non-resident taxpayer. Otherwise, the responsibilities and liabilities of the AI are discussed in the guidance Authorised Intermediary's responsibilities and liabilities.

The dividend payor may follow the procedure described in this guidance when identifying a nonresident dividend in a situation where there is no AI in the chain, who would have assumed responsibility for the dividend payment information. In this case, the payor is responsible for investigating the beneficiary's country of residence and ascertaining that the provisions on dividends of an international treaty can be applied to the dividend beneficiary. The dividend payor's obligations and liabilities when paying dividend to a nonresident taxpayer is discussed in more detail in the guidance Withholding tax at source on dividends, interest and royalties, and the payor’s obligations.

2 Investor Self-Declaration

2.1 Dividend beneficiary's responsibility to provide the correct information

The ISD concerns dividend income received from Finland and paid by a publicly listed company. It refers to the declaration provided by an account holder who is a customer of an AI, i.e. the dividend beneficiary, which certifies the dividend beneficiary's country of residence for tax purposes and that they are the beneficial owner of the dividend in accordance with the applicable tax treaty. In the ISD, the dividend beneficiary also provides the additional information relevant to determining the appropriate rate of withholding to be applied.

The dividend beneficiary must provide the AI with the information referred to in Section 1 of the ISD decision and confirm the information to be correct. The contents required on the ISD depend partly on whether the beneficiary is a natural person or other than natural person. It is the dividend beneficiary's responsibility to provide the correct information in the ISD and inform the AI of changes in their circumstances without undue delay. The contents of the ISD is discussed in more detail in Chapter 3.

In the ISD, the dividend beneficiary certifies that they are a resident for tax purposes in their country of residence and the beneficial owner of the dividend income as referred to in the tax treaty between their country of residence and Finland with respect to the dividend to which the ISD relates. When providing the certifications, the dividend beneficiary must verify the fulfilment of the criteria necessary to apply tax treaty benefits in accordance with the tax treaty between their country of residence and Finland with respect to the dividend to which the ISD is related. If necessary, the dividend beneficiary must verify the applicability of the tax treaty from the tax authority of their country of residence or the Finnish Tax Administration. The taxation on nonresident taxpayers’ dividends and the concept of the beneficial owner is discussed in the guidance Payments of dividends, interest and royalties to nonresidents.

If the dividend beneficiary submits incorrect information for taxation, submitting such information may result in the imposition of tax, tax increase or late fees. If the incorrect information was submitted with the intention to avoid taxes, this may result in criminal punishment (tax fraud).

2.2 Authorised Intermediary's responsibilities

The dividend provisions of an international treaty can be applied if the dividend payor or the intermediary closest to the beneficiary, who at the time of the dividend distribution is registered in the Register of Authorised Intermediaries referred to in Section 10d, has taken reasonable measures to determine the beneficiary's country of residence as well as verified that the provisions on dividends of an international treaty can be applied to the beneficiary (Section 10b(2) of the Tax at Source Act).

It is the AI's responsibility to make sure that the dividend beneficiary has in the ISD provided the information referred to in Section 1 of the ISD decision and confirmed the information to be correct. The requirement for granting tax treaty benefits is that the AI has verified the reliability of the ISD in accordance with the procedure referred to in Section 3 of the ISD decision. The procedure, with which the reliability of the ISD is verified, is discussed in more detail in Chapter 5.

The AI must ensure that the dividend beneficiary understands the intended use for which information is submitted and collected. The AI must also inform the dividend beneficiary that it is the beneficiary’s reponsibility to ensure that the information given in the ISD are up-to-date and correct.

The AI shall inform the dividend beneficiary to pay attention to the certifications that are given in the ISD and advise the beneficiary to contact the tax authority of their country of residence or the Finnish Tax Administration insofar as the tax treaty definition is unclear to the beneficiary. Tax treaty benefits should not be granted, if the applicability of the tax treaty is unclear and the dividend beneficiary does not provide the AI with evidence supporting its applicability.

Among other things, the application of tax treaties' dividend articles usually require that the person resident in the other Contracting State is the beneficial owner of the income as referred to in the tax treaty. According to the OECD Commentary for Model Tax Convention, the income recipient is the beneficial owner of the income when they have the right to use and enjoy the income unconstrained by a contractual or legal obligation to pass on the payment received to another person. In the Finnish legal and tax practice, it is deemed that in the interpretation of the provisions of tax treaties in accordance with the OECD Model Tax Convention in Finland, it is reasonable to give significance to what is stated in the OECD Commentary of the Model Tax Convention about the interpretation of the treaty regardless of whether the other party of the treaty is an OECD member state (Supreme Administrative Court ruling KHO:2011:11).

When verifying the reliability of the ISD, the AI may evaluate the reliability of the dividend beneficiary's certifications based on the beneficial owner concept in accordance with the most recent OECD Commentary on the Model Tax Convention. Therefore, it is not required for the AI to separately identify whether there are specific grounds for an interpretation to deviate from the commentary or be in line with a certain commentary version with regard to a single tax treaty. The interpretation of the OECD Model Tax Convention, including the concept of the beneficial owner of dividend, is discussed in more detail in the guidance Payments of dividends, interest and royalties to nonresidents and Articles of tax treaties

The AI's responsibilities and liabilities are otherwise discussed in the guidance Authorised Intermediary's responsibilities and liabilities.

3 Contents of the ISD

3.1 The dividend beneficiary is a natural person

3.1.1 Information on the dividend beneficiary

In accordance with Section 1(1) of the ISD decision, a dividend beneficiary who is a natural person must in the Investor Self-Declaration declare and confirm to be correct the following information:

- the number of the account where the shares are held;

- country of residence for tax purposes as referred to in the tax treaty between the dividend beneficiary's country of residence and Finland;

- tax identification number issued by the country of residence;

- as identifying information the natural person’s name, date of birth and address.

The ISD must specify the account that the ISD relates to, and where the shares based on which the dividend is paid are held. The account number is sufficient as the account's identifying information. If the ISD relates to several accounts, these are all specified in the ISD.

In the ISD, the dividend beneficiary must specify their country of residence for tax purposes referred to in the tax treaty between the beneficiary's country of residence and Finland. It is not required to specify particularly the tax treaty between beneficiary's country of residence and Finland, instead the information on the country of residence for tax purposes can be general like in the ISD in the TRACE IP (ISD-Individuals, hereinafter ISD-I, TRACE IP p. 43). However, the dividend beneficiary must then ensure, that their country of residence is their country of residence also when applying the tax treaty between the country in question and Finland.

The ISD must also specify the beneficiary's Tax Identification Number (TIN) issued by their country of residence for tax purposes. If the beneficiary's country of residence does not issue TINs, the ISD must state this.

The ISD must specify the full name of the dividend beneficiary, including the first and last name, and date of birth. Additionally, the ISD must specify the beneficiary's permanent address in the country of residence, and the mailing address if it is different from the permanent address. The address information must include the street name, property number, possible suite number, postal code, city and country.

3.1.2 Certifications concerning the applicable tax treaty

In the ISD, the dividend beneficiary must certify that they are a resident for tax purposes in their country of residence as referred to in the tax treaty between Finland and the country in question. Additionally, the dividend beneficiary must certify that they are the beneficial owner of the dividend income from Finland in the manner referred to in the applicable tax treaty, and therefore eligible for tax treaty benefits.

The dividend beneficiary's certification must comprise of the following certifications in accordance with Section 1(2) in the ISD decision:

- I certify that I am a resident of my country of residence for tax purposes as referred to in the tax treaty between my country of residence and Finland.

- I certify that I am not acting as an agent, nominee or conduit with respect to the income to which this declaration relates.

- I certify that I am the beneficial owner of the dividend as referred to in the tax treaty between my country of residence and Finland, and that I meet the criteria for tax at source benefits of the applicable tax treaty with respect to the dividend to which this declaration relates.

- I certify that the dividend, to which this declaration relates, is not attributable to a permanent establishment.

- I undertake to inform the intermediary of changes in my circumstances without undue delay.

The certification in accordance with Section 1(2)(3) of the ISD decision, that the dividend beneficiary is a resident of their country of residence for tax purposes as referred to in the tax treaty between Finland and their country of residence, can be part of a general certification regarding the country of residence for tax purposes like in the ISD-form in the TRACE IP (ISD-I, TRACE IP p. 43). However, the dividend beneficiary must then ensure, that they are resident for tax purposes in their country of residence as referred in the tax treaty between their country of residence and Finland so that the ISD can be applied to the dividend received from Finland.

3.2 The dividend beneficiary is other than a natural person

3.2.1 Information on the dividend beneficiary

In accordance with Section 1(1) of the ISD decision, a dividend beneficiary who is other than a natural person must in the Investor Self-Declaration declare and confirm to be correct the following information:

- the number of the account where the shares are held;

- country of residence for tax purposes as referred to in the tax treaty between the dividend beneficiary's country of residence and Finland;

- tax identification number issued by the country of residence;

- as identifying information name, address, legal form, and country of registration or the country under whose laws it is established.

Other than a natural person referred to in Section 1 of the ISD decision refers to a company, i.e. body corporate or entity, that is treated as a body corporate for tax purposes in accordance with the applicable tax treaty (hereinafter entity).

The ISD must specify the account that the ISD relates to, and where the shares based on which the dividend is paid are held. The account number is sufficient as the account's identifying information. If the ISD relates to several accounts, these are all specified in the ISD.

In the ISD, the dividend beneficiary must specify their country of residence for tax purposes referred to in the tax treaty between the dividend beneficiary's country of residence and Finland. It is not required to specify particularly the tax treaty between beneficiary's country of residence and Finland, instead the information on the country of residence for tax purposes can be general like in the ISD in the TRACE IP (ISD-Entities, hereinafter ISD-E, TRACE IP p. 46). However, the dividend beneficiary must then ensure, that their country of residence is their country of residence also when applying the tax treaty between the country in question and Finland.

The ISD must also specify the beneficiary's Tax Identification Number (TIN) issued by their country of residence for tax purposes. If the beneficiary's country of residence does not issue TINs, the ISD must state this.

The ISD must specify the entity submitting the ISD. The official name of the entity is specified in the ISD as it is recorded in the entity's constitutive documents. If the name has been changed at a later date, the official name is specified as it is valid at the time the ISD is given. The ISD does not need to specify the beneficiaries of the entity if the entity providing the ISD is a resident of their country of residence for tax purposes and the beneficial owner as referred to in the tax treaty, and thus entitled to tax benefits on its own behalf.

The ISD must specify the beneficiary's statutory address in its country of residence, as well as the mailing address if it is different from the statutory address. The address information must include the street name, property number, possible suite number, postal code, city and country.

The ISD must specify the legal form of the entity being the beneficiary that submits the ISD. The options are the following:

- Body Corporate

- Government (including central bank of issue, agency or instrumentality)

- International organisation

- Pension institution or fund

- Charity (non-profit organisation)

- Collective investment vehicle

- Partnership

- Trust

- Estate

- Other (must be described what)

The ISD must specify the country where the entity is registered or the country, under whose laws it is established.

3.2.2 Certifications concerning the applicable tax treaty

In the ISD, the dividend beneficiary must certify that they are a resident for tax purposes in their country of residence as referred to in the tax treaty between Finland and the country in question. Additionally, the dividend beneficiary must certify that they are the beneficial owner of the dividend income from Finland in the manner referred to in the applicable tax treaty, and therefore eligible for tax treaty benefits.

The dividend beneficiary's certification must comprise of the following certifications in accordance with Section 1(2) in the ISD decision:

- I certify that I am a resident of my country of residence for tax purposes as referred to in the tax treaty between my country of residence and Finland.

- I certify that I am not acting as an agent, nominee or conduit with respect to the dividend to which this declaration relates.

- I certify that I am the beneficial owner of the dividend as referred to in the tax treaty between my country of residence and Finland, and that I meet the criteria for tax at source benefits of the applicable tax treaty with respect to the dividend to which this declaration relates.

- I certify that the dividend to which this declaration relates, is not attributable to a permanent establishment.

- I undertake to inform the intermediary of changes in my circumstances without undue delay.

The certification in accordance with Section 1(2)(3) of the ISD decision, that the dividend beneficiary is a resident of their country of residence for tax purposes as referred to in the tax treaty between Finland and their country of residence, can be part of a general certification regarding the country of residence for tax purposes like in the ISD-form in the TRACE IP (ISD-E, TRACE IP p. 46). However, the dividend beneficiary must then ensure, that they are resident for tax purposes in their country of residence as referred in the tax treaty between their country of residence and Finland so that the ISD can be applied to the dividend received from Finland.

According to Section 1(3) of the ISD decision, if a dividend beneficiary other than a natural person claims a tax at source rate lower than the general tax at source rate in the tax treaty to be applied, they must specify the applicable tax rate, certify that they are eligible for the tax treaty benefit in question and specify the grounds for their claim. This kind of certification must be provided, for example, if a dividend beneficiary who is a pension fund claims a special tax provision in the tax treaty to be applied. The dividend beneficiary must then, if necessary, present further clarification that is required for applying the special tax provision.

3.3 Authorisation to disclose information

Pursuant to Section 1(4) in the ISD decision, the dividend beneficiary must authorise the AI to provide the Tax Administration with the information required to verify the correctness of tax at source and the reliability of the Investor Self-Declaration, if other applicable legislation requires this kind of authorisation.

The information referred in the provision is the information that the dividend beneficiary provides in the ISD and the information based on which the AI verifies the reliability of the ISD. The requirement for granting tax at source benefits is that the AI can provide the Tax Administration with the referred information. The AI must report the identifying information of the dividend beneficiary in the annual information return to the Tax Administration and, if necessary, provide additional information and documentation at the Tax Administration's request. Thus, the AI must ensure that it can submit the information on the dividend beneficiary to the Tax Administration, other legislation notwithstanding. If, for example, data privacy, bank secrecy, personal data privacy or other legislation prevents the AI to provide the Tax Administration with information that the AI has collected and that is required for taxation at source, tax treaty benefits can not be granted.

For more details on the information submitted on the AI's annual information return, see Authorised Intermediary's annual information return, technical guidance (pdf).

3.4 The format of the ISD and confirmation of the information

In Finland, the ISD does not have a specific format requirement. It is essential that the ISD contains the beneficiary's information and certifications referred to in Section 1 of the ISD decision. The information must be available in a compiled manner and confirmed to be correct by the dividend beneficiary. The ISD may also comprise of several different pieces of information and contain several documents and files.

The AI may collect the information referred to in Section 1 of the ISD decision by using the forms in accordance with the TRACE IP (ISD-I and ISD-E, TRACE IP pp. 43-49), which are attached to this guidance. The information referred to in Section 1 of the ISD decision are the mandatory information required of the ISD. The AI may collect the information referred to in Section 1 of the ISD decision also by using some other form that contains the required information, or collect the information by other means.

The AI is not required to collect the ISD from the dividend beneficiary in Finland's official language, i.e in Finnish or Swedish. If the ISD has not been made in Finnish, Swedish or English, the AI must provide also a translation in one of the previous mentioned languages attached to the ISD at the request of the Tax Administration.

The AI can apply information and certifications collected for other purposes as an ISD. In this case, the AI must verify that the information and certifications cover the information and certifications required under Section 1 of the ISD decision, and, if necessary, obtain further information from the dividend beneficiary. Amongst other things, the information collected on the customer based on the legislation concerning prevention of money laundering and terrorist financing and know your customer rules (Anti-Money Laundering/Know Your Customer, hereinafter AML/KYC), as well as a declaration that the customer has provided for some other purpose may be utilised as an ISD. Such a declaration provided for another purpose may be, for example, a Self-Certification in accordance with the CRS/DAC2 requirements submitted to a financial institution by the account holder, or a certificate collected for the Qualified Intermediary systems of the United States, Ireland or Japan.

Example 1: The AI has obtained a Self-Certification in accordance with the CRS standard from a dividend beneficiary who is a Swedish natural person. In the Self-Certification, the beneficiary has certified that their country of residence for tax purposes is Sweden and that they do not have any other country of tax residence. The beneficiary has also provided the AI with the information required under the AML/KYC (Anti Money Laundering/Know Your Customer) legislation.

The AI has received the following information of the dividend beneficiary regarding the custodial account in which the shares are being held: country of residence for tax purposes, tax identification number issued by the country of residence, name, date of birth and address in the country of residence. While providing the above referred information, the beneficiary has verified the information to be correct in the manner required by the common information exchange standards (FATCA, CRS/DAC2). Attached to the contractual agreement made between the AI and the dividend beneficiary, the beneficiary has given a certification that they are the beneficial owner of the custodial account. Furthermore, the AI has verified that the certification is applicable for relief of taxation at source of dividend income from Finland in accordance with the tax treaty between Nordic countries. The contractual agreements between the AI and dividend beneficiary do not allow share lending or other agreements that could affect the interpretation of tax treaty with regard to the shares held in the custodial account. The beneficiary has undertaken to inform the AI of changes in their circumstances.

The information and certifications that the dividend beneficiary has provided fulfil the content requirements as referred to in the ISD decision. Therefore, the AI does not need to collect a separate ISD from the dividend beneficiary. Instead, it is sufficient that the AI verifies that the information and certification it has received along with the agreements cover the content requirements in accordance with the ISD decision. However, the AI must receive from the beneficiary an authorization to submit the information to the Tax Administration, if other applicable legislation requires this kind of authorization (ISD decision, § 1(4)).

Example 2: The dividend beneficiary has provided the AI with a Self-Certification in accordance with the CRS standard. In the Self-Certification, the beneficiary has certified that their country of residence for tax purposes is Denmark and that they do not have any other country of tax residence. The beneficiary has also provided the AI with the information required under the AML/KYC legislation. The AI has received the following information of the dividend beneficiary regarding the custodial account in which the shares are being held: country of residence for tax purposes, tax identification number issued by the country of residence, name, address in the country of residence, legal form and country of registration or the country, under whose laws it is established. While providing the above referred information, the beneficiary has verified the information to be correct in the manner required by the common information exchange standards (FATCA, CRS/DAC2). Attached to the contractual agreement made between the AI and the dividend beneficiary, the beneficiary has given a certification that they are the beneficial owner of the custodial account. The beneficiary is a limited company registered in Denmark and established under its laws. The beneficiary does not have permanent establishments outside Denmark. The beneficiary has undertaken to inform the AI of changes in their circumstances.

The information that the dividend beneficiary has provided fulfil the information required under the ISD decision. The certifications that the dividend beneficiary has provided do not cover all the certifications in accordance with the ISD decision. Additionally, the dividend beneficiary must certify that they are the beneficial owner of the dividend as referred to in the tax treaty between their country of residence and Finland, and that they meet the criteria for tax at source benefits of the applicable tax treaty with respect to dividends paid to shares that are held in the custodial account in question. If the dividend beneficiary claims a tax rate lower than the general tax at source rate in the tax treaty to be applied, they must also specify the applicable tax rate, certify that they are eligible for the tax treaty benefit in question, and specify the grounds for their claim. The AI must also receive from the beneficiary an authorization to submit the information to the Tax Administration, if other applicable legislation requires this kind of authorization.

Principally, an ISD is account-specific, but it can also be customer-specific when the customer's information has been confirmed to be correct and it has been verified that the circumstances are in accordance with the ISD on all accounts that the ISD covers. When the dividend beneficiary opens a new account, they do not have to provide a new ISD, if they confirm that the original ISD is applicable also to dividend that is paid to shares held in the new account, and the AI verifies the reliability of the ISD also on in respect of the new account.

The AI may advise the dividend beneficiary in the submittal of the information and prefill the ISD on behalf of the beneficiary. However, the ISD must always be certified to be correct by the beneficiary in a documented manner. The beneficiary must certify the correctness of the information in the ISD with a signature, an electronic signature or some other certification given by the beneficiary (such as a recording or a digital footprint). The certification must indicate the time of the certification of the correctness of the information. In these respects, the AI can utilise similar principles as described in the OECD's CRS standard and its commentaries.

When the beneficiary is an entity, in connection with the certification must be provided a clarification, that the person who certified the document has authority to sign on behalf of the entity, or a power of attorney.

4 Period of validity of the ISD

Pursuant to Section 2 of the ISD decision, an Investor Self-Declaration is valid no more than the year it is signed and the following five years. If the dividend beneficiary is a government or other public entity, or an international organisation, the declaration is valid until further notice.

Consequently, an ISD is principally valid the year it is signed and the following five years. If an ISD, that is verified to be reliable, indicates that the dividend beneficiary is a government or other public entity, or an international organisation, the ISD will remain valid until further notice. A public entity in accordance with the provision, refers to an entity that by reference to the national legislation of the contracting state concerned, have been incorporated or formed as public entity in that state. Such public entities are, for example, the state, its agency or instrumentality, or a central bank.

However, the ISD remains valid at most until the AI receives information of a change in the account holder's circumstances, due to which the original ISD is incorrect or unreliable. The AI must monitor the correctness of the information submitted in the ISD during the validity period of the ISD in the manner described in Chapter 5.3.

The validity period of the ISD is counted from the moment when the dividend beneficiary has provided the declaration and certified it to be correct.

Example 3:The customer has signed an ISD on 22 November 2020, certifying that the customer lives in Spain in the manner referred to in the tax treaty between Finland and Spain, and that the customer is the beneficial owner of the dividend. The validity of the ISD ends on 31 December 2025 unless there is a change in circumstances.

Example 4: On 20 April 2021, in the situation described in Example 3, the customer notifies the AI of a new permanent mailing address located in Germany. The AI must react to the change of the mailing address, because the mailing address is now in a different country than the one where the customer certified as the country of residence for tax purposes. The AI may not apply the tax treaty between Finland and Spain, nor any other tax treaty, before it has received an explanation from the customer on the customer's country of residence for tax purposes.

If the dividend beneficiary provides the ISD after the dividend payment, and at the same time certifies that the ISD also applies to the dividend in question, the ISD can be applied in pursuance of a correction made during the payment year, if the AI has verified the reliability of the ISD also concerning the dividend payment in question. The correction made during the payment year (quick refund procedure) is discussed in more detail in the guidance Authorised Intermediary's responsibilities and liabilities.

The AI can apply previously collected information and certifications as an ISD (see Chapter 3.4, examples 1 and 2). In this case, the validity period of the ISD, that the AI has verified to be reliable, is counted from the moment the dividend beneficiary has provided the information and certifications in question and verified them to be correct. If the dividend beneficiary certifies the information and the certifications it has previously provided to be correct and certifies their applicability as an ISD, the validity period is counted from the moment the dividend beneficiary has provided this latest certification.

Example 5:The dividend beneficiary has signed a contractual agreement concerning a custodial account and provided the information required under AML/KYC legislation in March 2015, and provided a Self-Certification in accordance with the CRS standard in February 2016. In addition to the previously provided information, the dividend beneficiary has on the 29 May 2021 provided the required certifications and certified the previously provided information to still be correct. The AI verifies the reliability of the ISD in the manner required by the ISD decision.

The ISD is valid no more than the year it is signed and the following five years. The validity period of the ISD begins from 29 May 2021 and ends on 31 December 2026, unless there is a change in the dividend beneficiary's circumstances that affects the reliability of the ISD.

5 Procedure to verify the reliability of the ISD

5.1 General on verifying the reliability

Pursuant to Section 10b(4) of the Tax at Source Act, an ISD must be sufficiently reliably documented and consistent with the other information on the dividend beneficiary in the possession of the AI.

Pursuant to Section 3(1) of the ISD decision, the payor or the AI referred to in Section 10d of the Tax at Source Act must make sure, that the dividend beneficiary has in the ISD provided the information referred to in Section 1 of the decision and confirmed the information to be correct. The reliability of the ISD must be verified based on the information required by the common information exchange standards, and anti-money laundering and know your customer legislation, as well as the information otherwise available to the payor or the Authorised Intermediary on the dividend beneficiary. The AI has to verify the reliability of the ISD in the manner referred to in Section 3 of the ISD decision when the dividend beneficiary submits the ISD for the first time. The procedure, with which the reliability of the ISD is verified and the information based on which its reliability is verified, is described in Chapter 5.2 of this guidance.

Pursuant to Section 3(2) of the ISD decision, the reliability of the ISD must then be verified again, if the payor or the AI receives information on changes in the dividend beneficiary's circumstances. Consequently, it is the AI's responsibility to monitor, whether such changes in the dividend beneficiary's circumstances that affect the reliability and validity of the ISD take place. Dividend beneficiary's responsibility is to ensure that the information they have provided in the ISD are up-to-date as well as inform the AI of changes in their circmumstances. Changes in circumstances that affect the reliability of the ISD are discussed in Chapter 5.3 of this guidance.

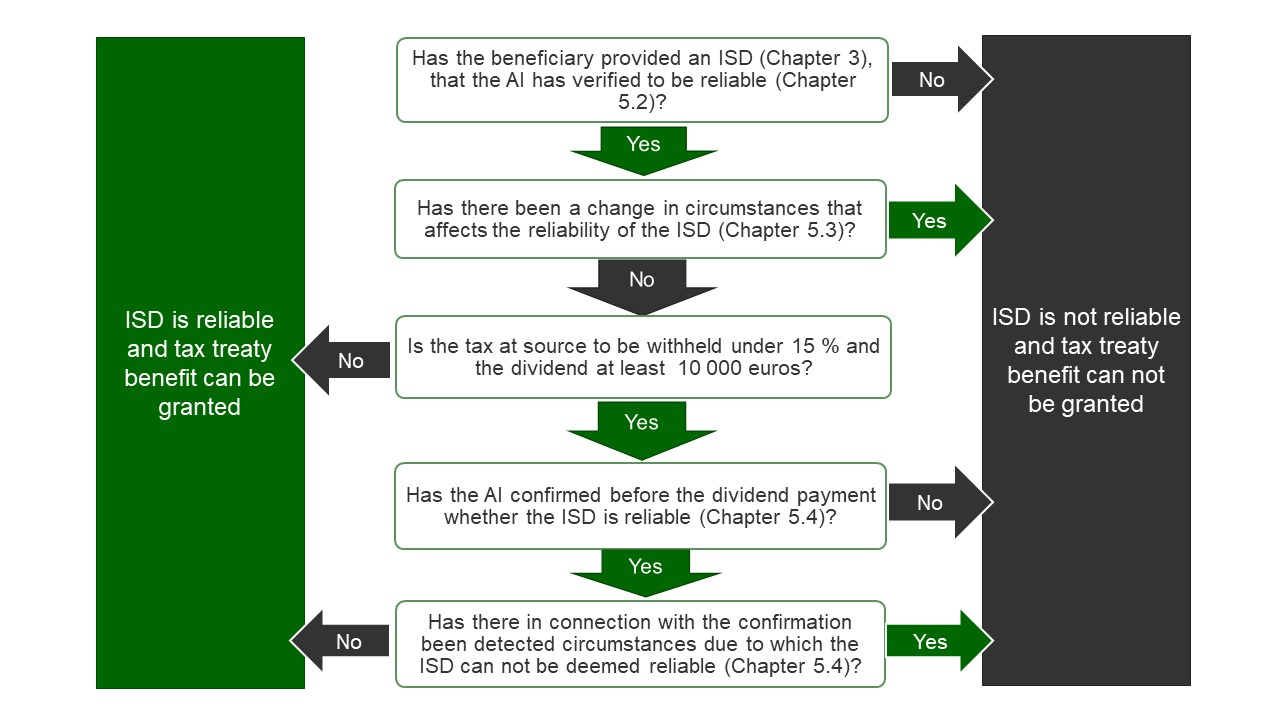

Pursuant to Section 3(3) of the ISD decision, the payor or the AI must, based on the information available to them, confirm before the dividend payment whether the declaration is reliable. Pursuant to Section 3(4) of the decision, the confirmation referred to in subsection 3 is not required, if the tax at source withheld from the dividend is at least 15 per cent or the dividend amount is under 10 000 euros.

If the AI has taken reasonable measures to verify the reliability of the ISD when receiving the ISD and there has been no changes in beneficiary's circumstances that affect the reliability of the ISD, the reliability of the ISD is not required to be verified separately before dividend payment when applying tax treaty provisions, if the tax at source withheld from the dividend is at least 15 per cent or the dividend amount is under 10 000 euros. However, the AI can always verify the reliability of the ISD per dividend payment, if they wish to do so.

The AI must confirm before the dividend payment whether the declaration is reliable, if the tax at souce withheld from the dividend is under 15 per cent and the dividend amount is at least 10 000 euros (ISD decision, Section 3(3) and (4)). The procedure to be followed in these situations, is described in Chapter 5.4.

The AI may follow the procedure in accordance with Chapters 5.2 and 5.3 and apply a general tax at source rate of 15 per cent under the tax treaty between the dividend beneficiary's country of residence and Finland, even though based on a special provision in the applicable tax treaty it could also be possible to apply a lower tax rate to the dividend. In this case the reliability of the ISD is not required to be verified additionally per dividend payment unless the AI knows or has reason to know that there has been a change in beneficiary's circumstances that affects the reliability of the ISD.

The procedure in accordance with Section 3 of the ISD decision, with which the reliability of the ISD is verified, is described in the diagram below.

5.2 Procedure to verify the reliability of the ISD when it is provided

The AI must verify that the ISD is sufficiently reliably documented and consistent with the other information the AI has in its possession on the dividend beneficiary as required in Section 10b(4) of the Tax at Source Act.

The reliability of the ISD is verified when the dividend beneficiary provides the ISD. The AI must take reasonable measures to verify the validity of the ISD. Reasonable measures mean that the AI compares the information received from the dividend beneficiary in the ISD to other information the AI has in its possession on the dividend beneficiary, in order to verify whether the information and certifications in the ISD are reliable.

In Section 3 of the ISD decision further provisions have been issued on the procedure with which reliability of the ISD is verified. Pursuant to subsection 1 of the section, the payor or the AI must ensure that the dividend beneficiary has in the ISD provided the information referred to in Section 1 of the decision and confirmed the information to be correct. The reliability of the ISD must be verified based on the information required by the common information exchange standards, and anti-money laundering and know your customer legislation, as well as the information otherwise available to the payor or the AI on the dividend beneficiary. In accordance with subsection 5 of the same section, the information referred to in subsection 1 must be available to the payor or the AI when verifying the reliability of the ISD.

Based on section 10b(4) of the Tax at Source Act, while verifying the relibiality of the ISD the AI must use the information in the AI's possession that affects the reliability of the ISD and that the AI has received on its customer in its ordinary course of business, including information collected on the basis of FATCA, CRS/DAC2 and AML/KYC requirements. The AI is not required to search information only for this purpose from public sources, such as the internet, public registries or commercial databases. The AI can use a service provider, such as an Contractual Intermediary (hereinafter CI) whose customer the beneficiary is, to collect the information and to verify the reliability of the ISD. In this case, the information collected by the service provider is comparable with the information in the possession of the AI itself as referred by the law. This information must be available to the AI. The indirect customers of the AI are discussed in more detail in Chapter 7.

Based on Section 3(5) of the ISD decision, at least the information required by the common information exchange standards, and anti-money laundering and know your customer legislation must be available to the AI when verifying the reliability of the ISD. The information required by the common information exchange standards are the information collected based on CRS/DAC2 standards and FATCA agreements. Information related to anti-money laundering and know your customer legislation refers to the information that the AI must collect of its customer obligated by the legislation concerning prevention of money laundering and terrorist financing and know your customer, i.e. AML/KYC legislation, and that is applied to the AI. The AI cannot thus refer to the fact that it did not know of information affecting the reliability of the ISD on the grounds of neglecting its requirements to collect information under other legislation that it is obligated by, such as FATCA, CRS/DAC2 and AML/KYC.

If based on the information in the possession of the AI, the ISD can not be deemed to be reliable, the requirement for granting tax treaty benefits is that the AI receives documentation from the dividend beneficiary that confirms the reliability of the ISD or the AI verifies the reliability of the ISD based on publicly available information.

Example 6: A customer of an AI has a permanent address in Sweden, and in a ISD, they have reported being a resident of Sweden for tax purposes. However, the customer has reported a mailing address in Finland. The AI may not treat the customer as a resident of Sweden unless the customer provides documentation that proves that they are resident of Sweden in accordance with the tax treaty between Sweden and Finland. The customer provides the AI with a certificate of residence issued by the Swedish tax authority, proving that they have tax liability to Sweden, and a certificate of being a nonresident taxpayer issued by the Finnish Tax Administration. Based on the received explanation, the AI may treat the customer as a resident of Sweden.

If the dividend beneficiary claims a tax at source rate lower than the general rate in the tax treaty between their country of residence and Finland to be applied based on a special provision of the tax treaty in question, the dividend beneficiary must provide a certification in accordance with Section 1(3) of the ISD decision on the fulfilment of the requirements for application. If the AI cannot verify the reliability of this certification based on the information in its possession, the AI must request a documented additional explanation from the dividend beneficiary that proves the beneficiary's eligibility for the benefit. When the dividend beneficiary claims a preferential tax rate to be applied based on its legal form, the requirement for granting the tax treaty benefit is a further clarification that confirms the beneficiary's legal form to be as referred to in the special provision in question, such as constitutive documents, a public registry extract or a certificate issued by an authority of the country of residence.

Example 7: A dividend beneficiary who is an US pension fund provides the AI with an ISD, in which it claims a zero tax rate to be applied on the dividend under the tax treaty between Finland and the United States. The AI requests a further clarification from the beneficiary on the applicability of the special provision. Based on the information in the AI's possession, it is not clear, whether the beneficiary is an US pension fund and the AI thus cannot verify the reliability of the certification. The pension fund provides the AI with its constitutive documents that indicates that they are a pension fund as referred to in the tax treaty. The AI verifies the reliability of the ISD as required in Section 3 of the ISD decision. The further clarification provided by the beneficiary is sufficient and the tax treaty benefit may be granted.

The tax rate in accordance with the tax treaty can be applied only based on a valid ISD. An ISD is valid if the AI has taken reasonable measures to verify the reliability of the ISD in the manner referred to above, and thus does not know or have reason to know that the ISD is unreliable or incorrect. The reliability or incorrectness of the ISD is determined based on the above referred information that is in the possession of the AI. If based on this information the ISD is unreliable or incorrect, tax treaty benefits cannot be granted based on the ISD. Examples of situations where the AI is deemed to know or have reason to know that the information or certifications that the beneficiary has provided in the ISD are unreliable or incorrect are discussed in Chapter 5.5.

5.3 Following changes in the dividend beneficiary's circumstances during the validity period of the ISD

An ISD is valid unless the AI has received information that there has been a change in the account holder's circumstances that affects the reliability of the ISD. If the AI receives information on changes in the dividend beneficiary's circumstances, it must verify the reliability of the ISD again (Section 3(2) of the ISD decision).

Thus the AI must monitor the correctness of the information that the dividend beneficiary has provided in the ISD during the validity period of the ISD. In practice, the AI must have a procedure in place for ensuring that any changes detected in the account holder's circumstances that may affect the reliability of the ISD also lead to a reassessment of the ISD's correctness and, if necessary, to its updating. A change in circumstances refers to situations where the AI receives new or changed information related to the beneficiary's taxational status, which is in conflict with the country of residence for tax purposes or applicable tax treaty that the beneficiary has declared.

An AI is deemed to be informed of a change in circumstances if

- the dividend beneficiary reports a change in their circumstances or submits a new ISD;

- the AI receives information on a change in the dividend beneficiary's circumstances by other means, such as from a public address information system;

- the AI detects a change in the dividend beneficiary's circumstances in its AML/KYC, FATCA, CRS/DAC2 or other procedure; or

- changes affecting the reliability of the ISD are made concerning the custodial accont, such as adding or replacing an account holder

If the AI has received information on a change in the dividend beneficiary's circumstances that affects the reliability of the ISD, tax treaty benefits can not be granted based on the original ISD. However, tax treaty benefits may be granted if the dividend beneficiary provides a new reliable ISD, that the AI verifies to be reliable. Alternatively, the AI may collect a reliable explanation and the necessary documentation from the dividend beneficiary with which the reliability of the original ISD is verified. The AI must retain all original and new documents, such as copies and notes, proving the verification of reliability.

Example 8: The dividend beneficiary has provided an ISD, which the AI has verified to be reliable. According to the ISD, the dividend beneficiary's country of residence for tax purposes is Sweden and their permanent address is in Sweden. The dividend beneficiary moves from the address that is given in the ISD to a new address and informs the AI of the new address in Sweden.

Because the dividend beneficiary's new address is within the country of residence referred to in the original ISD and there are no other changes in the dividend beneficiary's circumstances, the original ISD that is completed with the new address can still be deemed reliable.

Example 9: The dividend beneficiary has provided an ISD, which the AI has verified to be reliable. According to the ISD, the dividend beneficiary's country of residence for tax purposes is France and their permanent address is in France. The dividend beneficiary moves from the address that is given in the ISD to a new address and informs the AI of the new address in Germany.

Because the dividend beneficiary's new address is outside the country of residence referred to in the original ISD, the ISD can not be deemed reliable. The AI must request a new ISD from the dividend beneficiary.

The AI does not need to verify the reliability separately for a specific dividend payment, if in its operations it has monitored changes in dividend beneficiary's circumstances and the tax at source to be withheld from the dividend is at least 15 per cent or the dividend amount under 10 000 euros.

5.4 Verifying reliability per dividend payment when the tax at source withheld is under 15 % and the amount of the dividend at least 10 000 euros

The AI must confirm the reliability of the ISD before the dividend payment in accordance with Section 3(3) of the ISD decision based on the information available to the AI, if

- the tax at source to be withheld from the dividend is less than 15 per cent, and

- the amount of dividend is at least 10 000 euros.

In the provision, the dividend amount of 10 000 euros refers to a dividend that the dividend beneficiary has received from one dividend payor per payment.

If the above described requirements are fulfilled, the AI must, before the dividend payment, verify the reliability of the ISD based on the information in its possession that it has in its ordinary course of business collected on its client (for the information, see Chapter 5.2). In pursuance of the confirmation, the AI must also go through the information on possible changes in share ownership that it has in its possession, including trading information. If the AI uses a service provider, such as a CI whose customer the beneficiary is, to collect the information and to verify the reliability of the ISD, this information refers to the corresponding information that the service provider has collected.

The purpose of the confirmation in accordance with Section 3(4) of the ISD decision is that a tax treaty rate lower than 15 per cent would not be used for tax evasion purposes or aggressive tax planning. The AI must obtain a further clarification that ensures the reliability of the ISD, if in pursuance of the confirmation referred to above, the AI learns that

- the shares have been acquired no more than 30 days before the dividend payment,

- arrangements related to share ownership or derivatives are linked to the dividend payment, or

- there has been a change in the dividend beneficiary's circumstances that affects the reliability of the ISD (see Chapter 5.3).

If none of the above referred circumstances are fulfilled, the ISD can be deemed reliable and the tax traty benefit granted.

Example 10: B has provided an ISD, which the AI has verified to be reliable. The AI has monitored changes in B's circumstances during the validity period of the ISD. In the dividend distribution by X Oyj, B receives 10 000 euros of dividend, on which the tax at source to be withheld in accordance with the applicable tax treaty is 0 %.

The AI confirms the reliability of the ISD before the dividend payment. In accordance with the information in the AI's possession there are no arrangements related to share ownership or derivatives linked to the dividend payment and B has owned the shares, based on which the dividend is paid, for over 30 days. Neither have there been changes in B's circumstances after the ISD was provided. The tax treaty can be applied on dividend paid to dividend beneficiary B and the tax at source be left unwithheld based on the ISD.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Cras laoreet dolor tortor, ac viverra nibh vehicula quis.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Cras laoreet dolor tortor, ac viverra nibh vehicula quis.

The ISD can not be deemed reliable without a further clarification, if the shares were acquired no more than 30 days before the dividend payment. The shareholder who owns the share on the record date that is decided in the dividend distribution decision, has the right to the dividend that is paid based on the share in question. Thus the time period of 30 days is counted from the record date of the dividend. The effect of changes in ownership on the reliability of the information submitted by the dividend beneficiary in the ISD is assessed based on whether the changes affect the dividend beneficiary's eligibility for the tax treaty benefit. The ISD can be deemed reliable and the tax treaty benefit granted, if the AI receives a reliable explanation from the dividend beneficiary according to which there is no arrangements or circumstances related to the share acquisition that would affect the reliability of the ISD.

Example 11: A has provided an ISD that the AI has verified to be reliable. A receives 10 000 euros of dividend in the dividend distribution by X Oyj and the tax at source is 0 % in accordance with the applicable tax treaty, The AI confirms the reliability of the ISD before the dividend payment and detects that A has bought the shares on 1 April 2021. According to the dividend distribution decision of company X Oyj, the dividend payment date is 4 May 2021 and the record date 21 April 2021.

The AI requests a further clarification from dividend beneficiary A ensuring the reliability of the ISD, because the dividend beneficiary has acquired the shares less than 30 days before the record date. Dividend beneficiary A provides a further explanation, according to which the share acquisition is based on purchase, to which no arrangements that could affect dividend beneficiary A's right to tax treaty benefits are related. The AI does not know of any circumstances that would be contradictory with the explanation provided by dividend beneficiary A. The tax at source can be left unwithheld based on the ISD.

The ISD can not be deemed reliable without further explanation, if pursuant to the confirmation the AI learns that there is an arrangement related to share ownership or derivatives, that may have an effect on the reliability of the ISD, linked to the dividend payment. This kind of arrangement can be, for example, stock lending arrangement or other agreement based on which a third party is compensated for the dividend. In this case, the requirement for granting tax treaty benefits is that the AI receives a reliable explanation and documentation that the beneficiary is eligible for the tax treaty benefit regardless of the arrangement in question. If it is a question of a stock lending arrangement, the AI must request the documents concerning the stock lending and determine the contents of the lending agreement. Concerning possible derivatives, such as synthetic financing arrangements, other derivative contracts or swap arrangements, the AI must determine the purpose of the arrangement and the related documentation as well as the beneficial owner of the dividend on the record date of the dividend.

The ISD can be deemed reliable and the tax treaty benefit granted if the AI receives a reliable explanation and related documentation that proves, that the share transaction or ownership arrangements does not affect the interpretation of the tax treaty. If the AI can not ensure the reliability of the ISD and the dividend beneficiary's eligibility for tax treaty benefits remains ambiguous, tax treaty benefits can not be granted. In these kinds of situations the requirement for granting tax treaty benefits is a Tax Administration's decision in pursuance of which the matter has specifically been decided, such as an advance ruling. The beneficiary may alternatively apply for a refund of tax at source after the payment year, in which case the Tax Administration determines the dividend beneficiary's eligibility for the tax treaty benefit.

Example 12: B has provided an ISD that the AI has verified to be reliable at the time it was provided. According to the ISD, the tax treaty between Finland and UK can be applied to the dividend B receives and based on the tax treaty the tax at source is 0 %. B receives 10 000 euros of dividend in the dividend distribution by Y Oyj. According to the dividend distribution decision of company X Oyj, the dividend payment date is 15 May 2022 and the record date 2 May 2022. Dividend beneficiary B has acquired the shares 27 April 2022 and 30 % tax at source has been withheld on the dividend at the time of dividend payment.

The AI confirms the reliability of the ISD provided by B after the dividend payment. In pursuance of the confirmation, the AI detects that dividend beneficiary B has bought the shares just before the time of the dividend distribution and has given up the shares right after the dividend distribution. The AI requests a further clarification from dividend beneficiary B ensuring the reliability of the ISD, because the dividend beneficiary has acquired the shares less than 30 days before the record date. The AI requests a further explanation from the dividend beneficiary on whether the transactions involved arrangements that affect the interpretation of the tax treaty, and requests the related documentation. The dividend beneficiary provides the AI with an explanation that it is a question of a normal share purchase to which no arrangements are related. The AI does not have information on circumstances that would be contradictory with the explanation provided by the beneficiary. The tax at source withheld from the dividend can be corrected to 0 % in accordance with the tax treaty when making a correction during the payment year.

Example 13: C has provided an ISD that the AI has verified to be reliable at the time it was provided. According to the ISD, the tax treaty between Finland and UK can be applied to the dividend C receives and based on the tax treaty the tax at source is 0 %. C receives 10 000 euros of dividend in the dividend distribution by Y Oyj.

The AI confirms the reliability of the ISD provided by C after the dividend payment. In pursuance of the confirmation, the AI detects a stock lending arrangement is linked to the dividend payment that could affect whether C is deemed to be the beneficial owner in accordance with the tax treaty. The AI requests C to provide the documents concerning the stock lending and to explain the contents of the lending agreement.

Dividend beneficiary C provides the documentation that the AI has requested and an advance ruling issued by the Tax Administration, which expressly determines that C can be considered the beneficial owner as referred to in the tax treaty, regardless of the arrangement in question. The AI can apply the tax at source rate set in the tax treaty on the basis of the advance ruling if the actual circumstances correspond to the situation described in the advance ruling.

5.5 Examples of situations where the Investor Self-Declaration is unreliable or incorrect

The ISD cannot be deemed reliable nor can tax treaty benefits be granted based on the ISD, if the AI knows or has reason to know that the information or certifications that the dividend beneficiary has provided in the ISD are unreliable or incorrect.

See below for a list of examples of situations where the AI is considered to have reason to know that the ISD is unreliable or incorrect (TRACE IP, pp. 31-32). The list is not exhaustive.

- The beneficiary is a natural person, and the AI has examined, in order to comply with applicable Know Your Customer Rules, the passport of the beneficiary and the photograph in the passport does not match the appearance of the person presenting the passport.

- The AI may not rely on an ISD to reduce the withholding rate that would otherwise apply if the ISD is incomplete, contains information that is inconsistent with the beneficiary’s claim, or the AI has other information that is inconsistent with the beneficiary’s claim.

- The AI shall not treat a beneficiary as a resident of a country other than the Source Country if the permanent residence address on the ISD is outside the Source Country but the AI has a mailing or residence address for the beneficiary inside the Source Country, i.e., Finland. The AI nevertheless may treat the beneficiary as a resident of a country other than the Source Country if the AI has in its possession or obtains additional corroborative documentation that supports the beneficiary’s claim not to be a resident of the Source Country.

- The AI shall not treat a beneficiary as a resident of a country under an income tax treaty if the permanent residence address on the ISD is not in the applicable treaty country. The AI nevertheless may treat the beneficiary as a resident of the applicable treaty country if the AI has in its possession or obtains additional corroborative documentation that supports the beneficiary’s claim that it a resident of the applicable treaty country.

- The AI shall not treat a beneficiary as a resident of a country under an income tax treaty if the permanent residence address on the ISD is in the applicable treaty country but the AI has a mailing or other address for the beneficiary outside the applicable treaty country. The AI may nevertheless treat the beneficiary as a resident of the applicable treaty country if the AI has has in its possession or obtains additional corroborative documentation that supports the beneficiary’s claim that it is a resident of the applicable treaty country.

- The AI may not rely on the ISD to reduce the withholding rate on a dividend payment if

- the AI has been involved in arranging or structuring a transaction pursuant to which the person that provided the ISD obtained from the AI the security which generates the dividend payment; and

- under the law of the Source Country, that person is not entitled to a reduced rate with respect to income on securities received pursuant to such transaction.

- The AI shall not treat a beneficiary as a resident of a country under an income tax treaty if the only residence or mailing address it has for the beneficiary in that country is an in-care-of address or a P.O. Box. The AI may nevertheless treat the beneficiary as a resident of the applicable treaty country if the AI has in its possession or obtains additional corroborative documentation that supports the beneficiary’s claim that it is a resident of the applicable treaty country.

- The AI will be considered to know that the information contained in the ISD is incorrect if it has been informed by the beneficiary, the competent authority, the payor or another intermediary that the information contained in the ISD is unreliable.

6 Authorised Intermediary's tax liability

According to Section 10c(2) of the Tax at Source Act, if an AI has for the purpose of paying out dividend reported tax to be withheld from the dividend at a rate lower than the tax at source referred to in Section 7(2), the AI shall be liable for said tax, left unwithheld from the taxpayer due to erroneous reporting, as if it were its own tax. Consequently, the AI is then liable for the tax at source that was not withheld due to its negligence.

The AI is released from the liability referred to in Section 10c(2) of the Tax at Source Act by proving that it has followed the procedure in accordance with the Tax Administration’s ISD decision when investigating and identifying the dividend beneficiary while granting treaty benefits. In such a case, it is not a question of the AI´s neglicence, instead the liability for the tax left unwithheld lies solely on the dividend beneficiary (Section 16(2) of the Tax at Source Act).

The AI must be able to present proof at the request of the Tax Administration that it has received the information and certifications required in the ISD from the dividend beneficiary and verified the ISD to be reliable, and thus did not know or have reason to know that the ISD would be unreliable. In the assessment of whether the AI knew or had reason to known that the ISD is unreliable or incorrect, the information based on which the reliability should have been verified in accordance with Section 3 of the ISD decision is taken into account. The AI is also responsible for tax left unwithheld if it has applied a lower tax at source rate based on the ISD even though it has known or had reason to know, based on their own operations, that the ISD is ureliable or incorrect. If the AI or its employee certifies the correctness of an ISD on behalf of the beneficiary with a power of attorney, the AI is not released from liability if the information certified by the AI itself prove to be incorrect. The procedure to verify the reliability of the ISD and the information used in the procedure are discussed in more detail in Chapter 5.

The neglicence is also attributable to the AI, if it has granted tax treaty benefits to the beneficiary in situations where the AI or its related entity has been planning, marketing, organising, making available, giving support or advice, or been a party in an arrangement due to which the provision concerning the prevention of tax evasion in the tax treaty i.e. Principal Purpose Test provision applies to the dividend payment in question. An entity is a related entity of another entity, if either the other entity controls the other entity, or two entities are under mutual control. In this respect, control means direct or indirect ownership of the votes or value of the entity that exceeds 50 per cent. The AI is not required to check the information in the possession of its related entities, but the liability is based on the role of the AI or its related entity in the arrangement. If the AI shows proof that the error is caused by the negligence of the dividend beneficiary alone, the beneficiary has the liability for the tax left unwithheld (Section 16(2) of the Tax at Source Act). More information on the applicability of the Principal Purpose Test provision in the Tax Administration's guidance Articles of tax treaties.

Example 14: AI A has verified the reliability of the ISD that dividend beneficiary Y has provided based on the information the AI has collected based on CRS/DAC2, FATCA and AML/KYC procedures and the information otherwise in its possession on the dividend beneficiary. According to the ISD Y's country of residence for tax purposes is Ireland. Under the tax treaty between Finland and Ireland the applicable tax at source rate is 0 %. Y receives 10 000 euros of dividend from a Finnish publicly listed company. AI A confirms the reliability of the ISD before the dividend payment and reports for the purpose of paying out dividend that the tax at source rate to be applied on the dividend is 0 %.

After the payment year, the Tax Administration discovers that an arrangement was carried out relating to the payment of dividends, to which the provision concerning the prevention of tax evasion in the tax treaty (PPT provision) is applied and as a result beneficiary Y wouldn't have been entitled to the tax treaty benefit that was granted. The dividend beneficiary has carried out the arrangement by using a outside service provider and AI A or its related entity did not participate in the planning or implementation of the arrangement. Dividend beneficiary Y has not informed AI A of the arrangement nor has AI A received any information on the arrangement. Because the neglect is attributable to the dividend beneficiary alone, the Tax Administration imposes the unwithheld tax on the dividend beneficiary in accordance with section 16, subsection 2 of the Tax at Source Act.

Example 15: AI B has verified the reliability of the ISD that dividend beneficiary Z has provided based on the information the AI has collected based on CRS/DAC2, FATCA and AML/KYC procedures and the information otherwise in its possession on the dividend beneficiary. According to the ISD Z's country of residence for tax purposes is the UK. Under the tax treaty between Finland and the UK the applicable tax at source rate is 0 %. Z receives 8 000 euros of dividend from a Finnish publicly listed company. AI B confirms the reliability of the ISD before the dividend payment and reports for the purpose of paying out dividend that the tax at source rate to be applied on the dividend is 0 %.

After the payment year, the Tax Administration discovers that an arrangement was carried out relating to the payment of dividends, to which the provision concerning the prevention of tax evasion in the tax treaty (PPT provision) is applied and as a result beneficiary Z wouldn't have been entitled to the tax treaty benefit that was granted. Also, AI B has planned the arrangement in question and marketed the arrangement to dividend beneficiary Z. Because the tax has been left unwithheld due to the neglect of AI B, AI B is liable for the unwithheld tax.

In a situation where the AI detects after the dividend payment that the ISD has not been reliable, and there has been an under-withholding of tax at source, the AI must contact the Tax Administration without undue delay in order to correct the error. Also in a situation, where the AI receives information from the competent authority, another intermediary or the payor that the information contained in the ISD is unreliable the AI must contact the Tax Administration in order to correct the error. After the AI has received information of the error, the AI cannot grant tax treaty benefits based on the ISD in question and it has to obtain a new reliable ISD from the dividend beneficiary.

An AI's tax liability and the correction of an error are discussed in more detail in the guidance Authorised Intermediary's responsibilities and liabilities.

7 Indirect customers of an Authorised Intermediary

An AI can use a service provider to carry out their obligations that are based on the tax legislation. However, the obligations and liabilities based on the tax legislation belong to the AI that has assumed responsibility of the dividends, regardless of whether the AI uses a service provider or not.

The AI can use a service provider, such as the CI whose direct customer the dividend beneficiary is, to collect the information and to verify the reliability of the ISD. The AI must then make sure that the information in accordance with Section 3 of the ISD decision, is available to the AI, including the information related to the account as well as information required under CRS/DAC2, FATCA and AML/KYC procedures. The AI must also make sure that this information covers also the information on changes in the dividend beneficiary's circumstances. Therefore, the AI must in practice make sure that the CI follows changes in the dividend beneficiary's circumstances in the manner described in Chapter 5.3.

If the CI verifies the reliability of the ISD on behalf of the AI, the AI must be able to present and deliver the information to the Tax Administration if necessary. If instead the AI verifies the reliability of the ISD based on the information that the CI has collected, the AI must make sure that the required information is available to the AI when verifying the reliability. With respect to the documentation collected by other persons, the AI can apply similar principles as in the procedures in accordance with the CRS standard.

Example 16: AI A has assumed responsibility for granting tax treaty benefits on dividends paid to X who is a customer of CI B. After the payment year, the Tax Administration requests the AI to provide an explanation on how the dividend beneficiary's right to tax treaty benefits has been verified.

According to the explanation provided by AI A, it has verified the reliability of the ISD by using documentation that CI B has collected. AI A has made an agreement with CI B that AI A shall receive the required information and the documentation from CI B in order to carry out its obligations. CI B retains the information it has collected on its customer, including ISD's, information related to the account and the information required under CRS/DAC2, FATCA and AML/KYC procedures, as part of an information system so that AI A may easily access the information as well as the information regarding the nature of the documentation and its reliability. Also, CI B transmits the new or changed information it receives regarding the facts that affect the reliability of the ISD such as a change in the dividend beneficiary's circumstances, to the information system.

AI A provides the Tax Administration with the ISD and other information on dividend beneficiary X that has been stored in the information system in question and based on which the reliability of the ISD has been verified. The documentation shows also, how and when CI B has transmitted new or changed information that it has received and that may affect the reliability of the ISD.

Example 17: AI A has assumed responsibility for granting tax treaty benefits on dividends paid to Y who is a customer of CI B. After the payment year, the Tax Administration requests the AI to provide an explanation on how the dividend beneficiary's right to tax treaty benefits has been verified.

According to the explanafion provided by AI A, CI B whose customer dividend beneficiary Y is, has verified the reliability on behalf of AI A. Before the dividend payment, CI B has notified AI A that tax at source of 15 % should be withheld on the dividend while providing AI A with the identifying information of dividend beneficiary Y. AI A has made agreement with CI B that the CI B collects Investor Self-Declarations from the dividend beneficiaries and verifies their reliability as required in the Tax Administration’s ISD decision and guidance. Furthermore, CI B has undertaken to provide AI A with evidence and documentation (including the ISDs) indicating how the beneficiaries’ rights to tax treaty benefits has been verified.

AI A provides the Tax Administration with the evidence indicating how the beneficiary's’ right to the tax treaty benefit has been verified, as well as the ISD and other information based on which CI B has verified the reliability of the ISD.

More on the responsibilities and liabilities of the AI in situations where the AI uses a service provider, in the guidance Authorised Intermediary's responsibilities and liabilities.