Reporting data to the Incomes Register: rewarding employees, payments made to an entrepreneur and other special circumstances

- Validity

- - 11/5/2018

These instructions are intended for payers of contributions. The instructions use examples to describe the reporting of data to the Incomes Register, when the data concerns

- rewarding an employee with, for example, an employee stock option;

- seafarer’s income;

- payments made to companies and entrepreneurs;

- compensation for use; or

- a payment based on a separate task, such as a payment made to an athlete or a performing artist.

The payments made must always be reported to the Incomes Register at least as a total amount (the minimum level of detail for reporting, or the so-called reporting method 1). If the payer wishes, it can report payments it has made more specifically than required by the mandatory reporting method, using the separate complementary income types intended for this purpose (the higher level of detail for reporting, or the so-called reporting method 2). Reporting methods 1 and 2 cannot be combined in the same report.

The examples in these instructions describe reporting data both as a total amount and in an itemised manner. The examples do not present all data whose submission is mandatory, only the data necessary to reporting the special circumstances described in these instructions. The reporting of withholding, for example, is not separately described. The monetary amounts used in the example are illustrative in nature, and the amount of social insurance contributions, the withholding rate and tax-exempt reimbursement of expenses must be checked annually. The withholding is determined based on the earner-specific withholding rate.

These instructions describe reporting in domestic situations. Reporting data to the Incomes Register in international situations is described in the instructions Reporting data to the Incomes Register: international situations. Questions related to substitute payers and wage security are discussed in the instructions Reporting data to the Incomes Register: payments made by substitute payer.

1 Rewarding an employee

1.1 Employee stock option

An employee stock option is a remuneration given in the form of the employer company's stock option. An employee stock option benefit is an employment-based right to receive or obtain shares in an organisation at a price lower than the market value. The benefit is based on a convertible bond, optional bond, right of option, or other such agreement or commitment equivalent to these.

In the case of an employee stock option, the data needed for insurance purposes and the data needed for taxation purposes differ from each other in some situations. For this reason, data related to employee stock options is reported using two different income types, if necessary: Employee stock option with a subscription price lower than the market price at the time of issue and Employee stock option.

1.1.1 Employee stock option with a subscription price lower than the market price at the time of issue

In this section, the time of issue means the time when the employer gives the employee stock option benefit to the employee, or the time when the employee receives the employee stock option.

A benefit may be created for the employee at the time of issue, and included in the earnings from work on which the pension is based. If the subscription price of the option at the time of issue is clearly lower than the market price of the share, the amount of benefit gained from the employee stock option is not primarily based on share price development in the future. Instead, the employee receives a benefit that can be clearly estimated and has monetary value at the time of issue. A benefit deemed earnings from work is created immediately when the employee receives the right of option, rather than when the right of option is exercised. The benefit is deemed remuneration for work, and it is taken into consideration in the earnings from work on which pension is based, as well as in the grounds for unemployment insurance contributions and accident and occupational disease insurance contributions.

The benefit is not taxable income, and no employer's health insurance contribution needs to be paid from it.

Example 1: An employee receives a right of option at a price of one euro. At the time the right of option was issued, the market price of the share is three euros. At the time the right of option was issued, the employee receives a benefit amounting to two euros, which is taken into account as earnings from work. Because it is not taxable, the two-euro benefit must be reported to the Incomes Register using the income type Employee stock option with a subscription price lower than the market price at the time of issue.

If the subscription price of the option at the time of issue matches the current market price of the share (or is higher), the possible benefit from the employee stock options is formed (entirely) based on the share's price development. The work input of the employee (or that of the entire staff of the company) does not have a direct impact on the amount of benefit received. For this reason, the possible benefit gained from the increase in share price is not deemed remuneration for work, and the benefit is not included in the earnings from work on which pension is based; neither does it serve as grounds for unemployment insurance contributions or accident and occupational disease insurance contributions. In such a case, no report needs to be submitted to the Incomes Register when the option is issued.

For more details, see the Employment Pension Legislation Service of the Finnish Centre for Pensions' application instructions Employee stock options and equivalent profit sharing arrangements (in Finnish).

1.1.2 Employee stock option

When the employee exercises the employee stock option, tax is withheld from the gained benefit. The benefit from an employee stock option is not subject to social insurance contributions.

The benefit gained from the employee stock option is reported to the Incomes Register using the Employee stock option income type. The value of the employee stock option is the market value of the share at the moment the employee stock option is exercised. The total price the employee pays for the share and the employee stock option is deducted from the value of the benefit. The employee stock option is reported in its entirety on the report for the pay period during which the employee has announced the exercising of the employee stock option.

Example 2: The employee exercises the employee stock option in February. The taxable value of the benefit is EUR 22,000. The benefit is taken into account in the prepayment of tax as equal instalments (EUR 2,000 x 11 months). A report for the employee stock option is submitted to the Incomes Register using the Employee stock option income type, with the amount reported as EUR 22,000.00.

For more information on employee stock options, see the Tax Administration's Guidelines Taxation of employee stock options (in Finnish). These guidelines also discuss the taxation of options accrued from work abroad.

1.2 Stock options and grants

Stock options and grants are a remuneration paid in shares of the employer company or, instead of the agreed remuneration, an amount paid in euros that equals the value of the shares. Stock options and grants are reported to the Incomes Register using the income type Stock options and grants. By default, this income type is not subject to social insurance contributions.

Tax is always withheld from stock options and grants. Social insurance contributions are not paid if the following conditions are met:

- Under the profit sharing system, the employee has the possibility of obtaining shares in the employer company, listed on a stock exchange. A company belonging to the same group or some other equivalent financial conglomerate is also considered to be an employer company.

- The value of the benefit depends on the development of the price of the shares in question over a time period following the promising of the remuneration, which is over one year in length.

Otherwise, the remuneration is income subject to social insurance contributions. For example, if the time between being promised the remuneration and receiving it is no more than one year, the remuneration is subject to social insurance contributions.

The employer reports the insurance information using the separate Insurance information type entry. For more information on insurance information, see the instructions Reporting data to the Incomes Register: insurance-related data.

For more information on stock options and grants, see the Tax Administration's Guidelines Taxation of employee stock options and the Employment Pension Legislation Service of the Finnish Centre for Pensions' application instructions Stock options and grants (both in Finnish).

1.3 Benefit arising from synthetic option

A synthetic option means a right of option based on which the employee receives a monetary remuneration determined on the basis of the development of the employer company's share price (net value settlement). The employee is not entitled to subscribe shares underlying the option. Instead of a synthetic option, this arrangement may be called a share-based bonus or reward system.

Tax is withheld from the benefit arising from a synthetic option, but no social insurance contributions are paid.

The benefit arising from a synthetic option can be reported to the Incomes Register either using the income type Total wages (reporting method 1) or the income type Benefit arising from synthetic option (reporting method 2). If the benefit arising from a synthetic option is reported using the income type Total wages, the Insurance information type entry must be used to separately report that the share of the synthetic option of the total amount is not subject to social insurance contributions. For more information on insurance information, see the instructions Reporting data to the Incomes Register: insurance-related data.

A dividend equivalent can be paid for synthetic options. The dividend equivalent is paid on the basis of a profit sharing system to a person who is employed by the employer company but is not a shareholder. When the shareholders are paid dividends, the beneficiaries covered by the synthetic option system are paid dividend equivalents. The amount of the dividend equivalent is based on the amount of dividends paid to the shareholders. The dividend equivalent is reported to the Incomes Register either using the income type Total wages or, for example, the income type Other compensation. The dividend equivalent is subject to social insurance contributions.

For more information on synthetic options, see the Finnish Centre for Pensions' application instructions Employee stock options and equivalent profit sharing arrangements and the Tax Administration's Guidelines Taxation of employee stock options (both in Finnish). The Tax Administration's guidelines also discuss the taxation of options accrued from work abroad.

1.4 Personnel funds, performance bonuses and profit-sharing bonuses

1.4.1 Transferring funds into a personnel fund

The personnel fund receives funds from the employer's performance bonus and profit sharing systems as personnel fund contributions or their supplements, and the returns from the investment of these contributions. A personnel fund may also receive funds as donations. Each member of the personnel fund holds a share in the assets in the fund (their own fund shares). Transfers to a personnel fund are not reported to the Incomes Register.

If an employer pays an employee in cash instead of transferring the amount to a personnel fund, the payment is reported as regular wages and social insurance contributions are collected from it.

1.4.2 Share of reserve and surplus drawn from personnel fund

An employee can withdraw fund units or contributions from the personnel fund in cash. 20% of a fund unit withdrawn from a personnel fund is tax-exempt income and 80% is taxable earned income. For taxation purposes, surplus withdrawn from a personnel fund is treated in the same way as a fund unit withdrawn from a personnel fund. For more information, see the Tax Administration's Guidelines Taxation of income from a personnel fund (in Finnish).

The taxable share withdrawn from a personnel fund is reported to the Incomes Register using the income type Share of reserve and surplus drawn from personnel fund (taxable 80%). Only items withdrawn from a fund as fund units or surplus are reported using this income type. Tax is withheld, but social insurance payments are not paid from the amount withdrawn from the fund. The tax-exempt part is not reported to the Incomes Register. If the payment was withdrawn in cash, it is reported to the Incomes Register as regular wages, for example using the income types Total wages, Time-rate pay or Other compensation.

1.4.3 Performance bonus

Performance bonus is a remuneration paid based on meeting or exceeding the organisation's performance target agreed in advance.

Tax is withheld and social insurance contributions paid from a performance bonus, unless the performance bonus is transferred to the personnel fund. The performance bonus is reported to the Incomes Register either using the income type Total wages (reporting method 1) or the income type Performance bonus (reporting method 2). If the performance bonus is transferred to a personnel fund, it is not reported to the Incomes Register (see Section 1.4.1).

1.4.4 Profit-sharing bonus

Profit-sharing bonus is a remuneration distributed among employees without an advance plan, by a decision of the annual general meeting and determined based on the company's profits.

Tax is withheld from all profit-sharing bonuses other than those transferred into a personnel fund. The profit-sharing bonus can be paid directly to the employee instead of being transferred into a personnel fund, in which case no social insurance contributions are paid from the bonus. If the company does not have a personnel fund as described in the Act on Personnel Funds, no social insurance contributions are paid from the profit-sharing bonus if it is paid as a distribution of profits or in cash. The exemption from social insurance contributions also requires that the cash profit-sharing bonus is paid to all personnel and is not an attempt to replace a system of remuneration required by the collective bargaining agreement or the employment contract. Furthermore, the basis for determining a cash bonus must be in accordance with the Employees' Pensions Act, the Workers' Compensation Act and the Act on Personnel Funds, and the amount of the company's free capital must be greater than the total amount of the cash-based profit-sharing bonus and the dividend paid to shareholders as decided by the annual general meeting.

The profit-sharing bonus is reported to the Incomes Register either using the income type Total wages (reporting method 1) or the income type Profit-sharing bonus (reporting method 2). If the profit-sharing bonus is transferred to a personnel fund, it is not reported to the Incomes Register (see Section 1.4.1).

1.5 Monetary gift for employees

A gift from the employer received as cash or a comparable payment is reported to the Incomes Register using the income type Monetary gift for employees.

A monetary gift is deemed taxable income subject to withholding. No social insurance contributions are paid from a monetary gift if the monetary gift was given due to the employee's anniversary or for some other personal reason of this kind. If the monetary gift was not given on the employee's anniversary, for example, if the employee was paid 13th month pay, a Christmas bonus, a monetary company anniversary gift, or a monetary retirement gift, social insurance contributions must be collected from the payment.

By default, this income type is subject to social insurance contributions.

If the monetary gift given is not subject to social insurance contributions, the employer must report this separately using the Insurance information type entry. For more information on insurance information, see the instructions Reporting data to the Incomes Register: insurance-related data.

1.6 Other taxable benefit for employees

A non-monetary taxable benefit collectively granted to personnel by the employer is reported to the Incomes Register using the income type Other taxable benefit for employees. An example of a benefit deemed taxable is a personnel benefit granted for voluntary exercise and cultural activities exceeding the statutory maximum annual amount of EUR 400.

If the benefit has been granted collectively to all personnel, it is not subject to social insurance contributions. By default, for this income type the benefit is not subject to social insurance contributions. Tax is withheld from the income.

If the benefit has only been granted to some personnel, it is taxable in its entirety and subject to social insurance contributions. In such a case, the employer reports the insurance information by using the Information insurance type entry. For more information on insurance information, see the instructions Reporting data to the Incomes Register: insurance-related data.

The income type Other taxable benefit for employees is also used in a situation where the employer pays a daily allowance to the employee on more lenient grounds than those specified in the decision by the Tax Administration. The Insurance information type entry can then be used to indicate that the employer is paying a daily allowance to the employee on more lenient grounds, based on a collective bargaining agreement, than those specified in the decision by the Tax Administration. The income is then not subject to earnings-related pension, unemployment, or accident and occupational disease insurance contributions.

1.7 Share issue for employees

A share issue for employees is a share issue targeted at the company's personnel. The income taxation of a share issue for employees is bound to the relationship between the share's subscription price and market price: If the subscription price matches the market value, no taxable benefit is created for the employee subscribing the shares. If, however, the subscription price is lower than the share's market value, it is a case of personnel benefit granted on the basis of employment, deemed earned income of the employee received at the time of subscription. The subscription benefit also applies to shares in an organisation.

However, no taxable benefit is created if the discount is no more than 10% and the benefit is available to a majority of the personnel. It is enough if the personnel have the opportunity to participate in the share issue if they so desire. In such a case, nothing needs to be reported to the Incomes Register. If the benefit is available to the majority of personnel, but the effective discount is over 10%, the income type Share issue for employees is used to report only the amount exceeding the 10% discount to the Incomes Register. If the benefit is not available to the majority of personnel, the entire discount received is regarded as wages. In such a case, the payment is reported using other income types for the wages.

Tax is withheld from the income reported with the income type Share issue for employees, but by default, the income is not subject to social insurance contributions.

If the share issue for employees is subject to social insurance contributions, the employer reports the insurance information using the Insurance information type entry. For more information on insurance information, see the instructions Reporting data to the Incomes Register: insurance-related data.

2 Seafarer's income

Seafarer's income is wage income paid for work performed on board a vessel, related to the maritime traffic of the vessel. The vessel must have a gross capacity of no less than 100 register tons. The work is performed while in the employment of the shipowner, and must meet the requirements laid down in the income tax act (tuloverolaki 1535/1992). The wage income can be paid as a monetary remuneration or as a benefit worth money. This provision applies to both Finnish and foreign vessels. For more information, see the Tax Administration's Guidelines Taxation of seafarer's income (in Finnish).

Seafarer's income is reported to the Incomes Register just like regular wage income, with the addition of the Payment is seafarer's income and, if necessary, Time of cross trade and Withdrawal period entries.

If the employee works on board a vessel that does not visit Finnish territory during the month in question, the employee is entitled to a cross trade deduction in their taxation. The shipowner paying the seafarer's income reports the time of cross trade as full months for the purpose of granting the cross trade deduction. If the pay period is not a calendar month, information on the time of cross trade is not submitted on an earnings payment report until the payer knows that the grounds for the cross trade deduction have been fulfilled for the month in question. The time of cross trade is reported by specifying the number of months for which the employee is entitled to the cross trade deduction.

Example 3: The employer's pay period is two weeks. Three pay periods end in April: weeks 12–13, weeks 14–15 and weeks 16–17. The employer cannot be sure that the time of cross trade condition has been fulfilled for April until reporting the wage payment for weeks 16–17 to the Incomes Register. The employer has also been entitled to a cross trade deduction in March, but not in January or February. In the earnings payment report for weeks 16–17, the employer reports 2 as the value of the Time of cross trade entry.

Seafarer's income is income for the year during which it was paid or recorded in the employee's account, regardless of during which calendar year the wages were earned or from which period it was accrued. Seafarer's income is reported to the Incomes Register as earnings from the date on which it has been actually paid to the employee monetarily.

- If, however, the income has been available for withdrawal under maritime labour legislation and an agreement complementing it prior to the actual payment date, the withdrawal period details must be reported for the payment: Withdrawal period, start date and Withdrawal period, end date.

- If the income has not been available for withdrawal under maritime labour legislation and an agreement complementing it prior to the actual payment date, the withdrawal period is not specified for the payment.

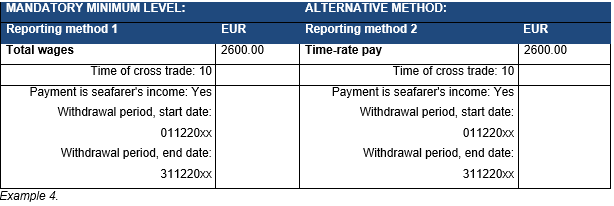

Example 4: An employee works on board a vessel for December and January. The maritime employer's pay period is one calendar month, and the wages are available for withdrawal on the last day of the wage payment month. The employee is offshore for December, due to which the December wages of EUR 2,600 are not paid to the employee's account until January. Because the income could have been withdrawn on the last day of December, it is taxable income for the year in which it could have been withdrawn. The maritime employer enters the first day of December as the start date of the withdrawal period and the last day of December, and the year as the end date. The employee's right to a cross trade deduction for March to December is also reported on the earnings payment report.

A separate report is submitted for January (not depicted here).

3 Payments made to companies and entrepreneurs

3.1 Non-wage compensation for work

Non-wage compensation for work is remuneration for work, a task or service not paid as wages.

The work is performed based on a commission relationship, i.e., the employee is not in an employment relationship with the payer. Non-wage compensation for work is taxable income, and tax is withheld from it if the recipient is not registered in the prepayment register.

Only payments made to a worker not registered in the prepayment register must be reported to the Incomes Register, so tax must be withheld from them. These payments are reported using the income type Non-wage compensation for work. A report must be submitted even if the recipient of the non-wage compensation for work is not a natural person – for example, a limited liability company, general partnership or a limited partnership. The Type of additional income earner data: Organisation information is submitted to the Incomes Register if the income earner is a general partnership, limited partnership, limited liability company, cooperative, association, foundation, or some other legal person governed by civil law.

The share of value added tax included in the non-wage compensation for work is not reported to the Incomes Register. In other words, the amount paid VAT excluded is reported in the earnings payment report.

As a rule, no social insurance contributions are paid from non-wage compensation for work. By default, this income type is not subject to social insurance contributions.

A payer covered by the public sector pensions act (julkisten alojen eläkelaki 81/2016) must pay the employer's earnings-related pension insurance contribution based on a private person's commissioning agreement if the income earner is not insured in accordance with the self-employed persons' pensions act (yrittäjän eläkelaki 1272/2006). The payer of the non-wage compensation for work collects the employee's earnings-related pension insurance contribution from the non-wage compensation for work. The employee's earnings-related pension insurance contribution is not reported to the Incomes Register at all. This is regardless of the entrepreneur not being registered in the prepayment register, and the non-wage compensation for work and the tax withheld from it being reported to the Incomes Register. The entrepreneur can report the collected earnings-related pension insurance contribution in his or her accounting, or request a deduction in his or her own taxation.

Example 5: A limited partnership that is not registered in the prepayment register has invoiced EUR 12,000 for a renovation it has completed (incl. VAT EUR 2,322.58). In accordance with the decision of the Tax Administration, 13% tax must be withheld from an amount from which value added tax has first been deducted, or EUR 9,677.42. The employer's health insurance contribution does not need to be paid from the payment. The payer will report EUR 9,677.42 to the Incomes Register using the income type Non-wage compensation for work, and also reports the EUR 1,258.06 withheld using the income type Withholding tax.

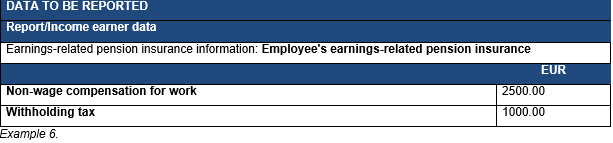

Example 6: A person completes a consulting commission for a Ministry. The person does not have a YEL insurance due to the small number of commissions. The person is not registered in the prepayment register and has provided the payer with a tax card on which the withholding rate is 40%. The Ministry reports the non-wage compensation for work to the Incomes Register using the income type Non-wage compensation for work and the tax it withheld using the income type Withholding tax. The Ministry does not report the employee's earnings-related pension insurance contribution it collected from the person.

For more information on insurance information, see the instructions Reporting data to the Incomes Register: insurance-related data.

Non-wage compensation for work paid to a company with a limited tax liability must be reported, if the payer has collected tax at source from the payment. Non-wage compensation for work paid to a natural person with a limited tax liability must always be reported regardless of whether or not tax at source has been collected.

3.1.1 Reimbursement of expenses related to non-wage compensation for work

If the remuneration or other payment was paid as a non-wage compensation for work, no tax-exempt reimbursements of expenses can be paid to the recipient (with the exception of an athlete's and competition judge's fees; for more information, see Section 5.1.2, Athlete's fees and 5.11, Reimbursement paid by a non-profit organisation). Reimbursements of expenses related to non-wage compensation for work are added to the amount of income as a total sum with the other remuneration and then reported to the Incomes Register.

Reimbursements of expenses related to work cannot usually be deducted from the non-wage compensation for work before tax is withheld. The only exception is the reimbursement of travel expenses paid to natural persons with no Business ID. Tax does not need to be withheld from this reimbursement of expenses if the grounds and amounts of the travel expenses are in accordance with the tax-exempt allowances for business travel laid down in the annual decision issued by the Tax Administration. These allowances are not tax-exempt either, so they are reported in the total amount of the non-wage compensation for work. Reimbursement of expenses is not reported using the income type Deduction before withholding.

Recipients of non-wage compensation for work can request that travel expenses be deducted in their taxation. However, business operators must deduct travel expenses in their accounting.

3.1.2 Dividends/profit surplus based on work effort (non-wage)

Dividend or profit surplus based on work effort can be wages or non-wage compensation for work, depending on whether or not the recipient is in an employment relationship with the payer company. This section discusses a situation where a dividend/profit surplus based on work effort is paid to a person who is not in an employment relationship with the payer company. The payment is non-wage compensation for work. If the payment is considered wages, it is reported to the Incomes Register using the income type Dividends/profit surplus based on work effort (wages) (see Section 3.2.2).

The income type Dividends/profit surplus based on work effort (non-wage) is used to report the dividend or profit surplus paid to an income earner as non-wage compensation for work, the distributive basis of which is the work effort of the recipient of the dividends or of a person within their sphere of interest. The data is also reported to the Incomes Register when the income earner is registered in the prepayment register.

The person on whose work effort the distribution of the dividends or profit surplus is based is reported to the Incomes Register as the recipient of the dividends/profit surplus based on work effort (name and personal identity code). This also applies to a situation where the actual recipient of the dividends or profit surplus is a holding company owned by the taxpayer. When the holding company further distributes the dividends to a shareholder, the holding company submits the annual information return 7812 for the dividends paid during the distribution. The dividends paid are not reported to the Incomes Register.

Tax is withheld from the dividends based on work effort (non-wage), unless the recipient is registered in the prepayment register. If tax has not been withheld from the dividends based on work effort because the recipient is a person other than the one in whose taxation the work effort dividends are deemed income, nothing is reported with the income type Withholding tax.

No social insurance contributions are paid from the payment.

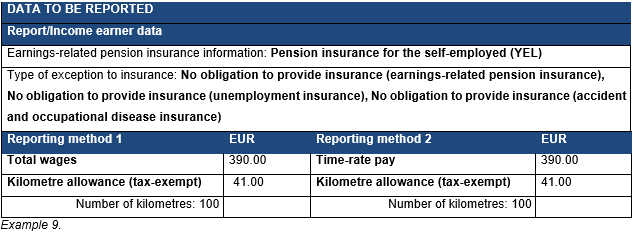

3.2 Wages of a YEL/MYEL insured self-employed person

A self-employed person must report to the Incomes Register any wages he or she has withdrawn from his or her company, as well as information on the applicable earnings-related pension insurance.

- Pension insurance for farmers (MYEL) is selected, if the income earner is insured in accordance with the farmers' pensions act (maatalousyrittäjän eläkelaki 1280/2006). Insurance under the farmers' pensions act is the earnings-related pension insurance for farmers, forest owners, fishers and reindeer breeders, and their family members. Scholarship recipients are also covered by earnings-related pension provision under MYEL.

- Pension insurance for the self-employed (YEL) is selected if the income earner is insured in accordance with the self-employed persons' pensions act (yrittäjän eläkelaki 1272/2006). The insurance is mandatory when the self-employed person fulfils the requirements for being covered by the self-employed persons' pensions act. The insurance must be taken out within six months of the beginning of the period of self-employment.

Self-employed persons covered by the self-employed persons' pensions act (YEL) include:

- a partner in a general partnership and a general partner in a limited partnership;

- a shareholder in a limited liability company acting in a leadership position, individually holding over 30% of the company or its votes, and a shareholder who, together with family members, holds over 50% of the company or its votes. The calculation of the ownership share also takes account of indirect ownership via other organisations or conglomerates, if a person alone or together with family members owns over 50% of said other organisation or conglomerate, or has an equivalent dominant influence.

Additionally, Type of exception to insurance: No obligation to provide insurance (earnings-related pension, health, unemployment or accident and occupational disease insurance) must be reported to the Incomes Register.

If the information in question is not used to report the wages of the self-employed person, the social insurance contributions may be levied twice.

The self-employed person's earnings-related pension and health insurance contributions are determined based on the confirmed YEL or MYEL income from work. The YEL and MYEL income from work confirmed by the pension provider is the income on which earnings-related pension insurance and health insurance contributions are based, and replaces the wages received by the self-employed person as the basis for the earnings-related pension and health insurance contributions. Income from work data is not reported to the Incomes Register, but the wages received by the self-employed person are reported for taxation purposes.

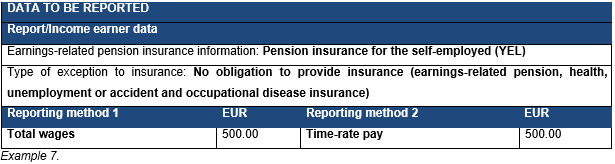

Example 7: A shareholder working for his own company withdraws EUR 500 in wages. The person is the only shareholder in the company, and has taken out a mandatory insurance policy under the self-employed persons' pensions act.

3.2.1 Partial owner

Partial owners of a company pay a lower employee's unemployment insurance contribution than employees. The concept of a partial owner is defined in the unemployment security act (työttömyysturvalaki 1290/2002).

A person's status as a partial owner or an employee of the company is affected by the ownership share, votes or other dominant influence of the person and their family members, as well as the person's position in the company.

Self-employed persons are not obligated to pay unemployment insurance contributions, and they are also not partial owners with respect to an unemployment insurance. A person is deemed a self-employed person or a farmer if he or she fulfils the conditions laid down in the self-employed persons' pensions act (yrittäjän eläkelaki 1272/2006) or the farmers' pensions act (maatalousyrittäjän eläkelaki 1280/2006).

Information on partial ownership is submitted to the Incomes Register by reporting Type of additional income earner data: Partial owner.

For more information on partial ownership, see: tvr.fi.

3.2.2 Dividends/profit surplus based on work effort (wages)

This income type is used to report dividends paid to a shareholder as wages, the distribution basis of which is the work effort of the recipient of the dividends or of a person in their sphere of interest.

The person on whose work effort the distribution of the dividends or profit surplus is based is reported to the Incomes Register as the recipient of the dividends/profit surplus based on work effort (name and personal identity code). This also applies to a situation where the actual recipient of the dividends or profit surplus is a holding company owned by the taxpayer. When the holding company further divides the dividends to a shareholder, the holding company submits the annual information return 7812 for the dividends paid during the distribution. The dividends paid are not reported to the Incomes Register.

Tax is withheld from dividends based on work effort. No earnings-related pension insurance, unemployment insurance or accident and occupational disease insurance contributions are paid from dividends paid to a company shareholder, even if the dividend is considered to be wages for taxation purposes, based on special regulations on dividends relating to work effort. The employer's health insurance contribution is paid from dividends based on work effort.

If tax has not been withheld from the dividends based on work effort because the recipient is a person other than the one in whose taxation the work effort dividends are deemed income, nothing is reported with the income type Withholding tax.

If the income earner is a YEL/MYEL-insured self-employed person, the insurance information described in Section 3.2 related to the wages of a YEL/MYEL-insured self-employed person must also be reported to the Incomes Register.

3.3 Invoicing service

In recent years, several service providers have been established, so-called invoicing services who are committed to handling the invoicing, tax withholding and insurance contributions of their clients (performers of the work) for a fee. These companies use different names for the service they provide, such as an invoicing service, invoicing channel or remuneration service.

In an invoicing service, the performer of the work and the invoicing service company can specifically agree on the establishment of an employment relationship between them with respect to taxation. The amount paid to the invoicing service company by the party that commissioned the work is then non-wage compensation for work, and the payment made by the invoicing service company to the performer of the work is deemed wages from the perspective of the Tax Administration. The invoicing service company will then have normal employer obligations with respect to the Tax Administration, i.e. it must withhold taxes from the wages it pays and pay the employer's health insurance contribution.

However, from the perspective of earnings-related pension providers, unemployment insurance policies and accident and occupational disease insurance policies, it is not an employment relationship. From the perspective of the insurers, the work invoiced through an invoicing service company is performed as a self-employed person, and the work must be insured according to the self-employed persons' pensions act.

Reimbursements of travel expenses, decreed tax-exempt in the income tax act (tuloverolaki 1535/1992) and paid in addition to the agreed wages, are the only tax-exempt reimbursements of expenses. In an invoicing service, the common procedure is that the party who commissioned the work and the performer of the work agree on an overall payment that the commissioning party pays to the invoicing service company. The invoicing service company deducts its own fee and other expenses from the amount, and pays the rest to the performer of the work. Under this arrangement, travel expenses are not reimbursed in addition to the agreed wages, so they are not tax-exempt. Tax does not need to be withheld from reimbursements of travel expenses paid to a natural person (no Business ID), but they are still taxable income to the performer of the work. The travel expenses are reported to the Incomes Register using the income type Deduction before withholding. The performer of the work must request that the expenses be deducted in his or her taxation. For more information, see the Guidelines Reporting data to the Incomes Register: fringe benefits and reimbursements of expenses, Section 2.5, Deduction before withholding.

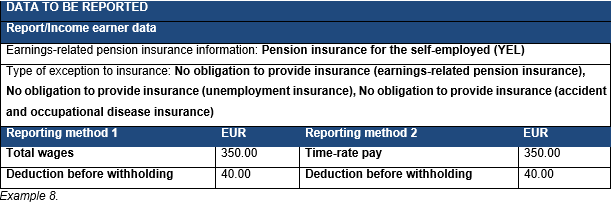

Example 8: A person has performed work for a client worth EUR 500, invoiced by the invoicing service from the client. The person and the invoicing service have agreed that the person is in an employment relationship with the invoicing service. The person has taken out YEL insurance, because the earnings-related pension provider has deemed that there is no employment relationship between the person and the invoicing service with respect to labour legislation. Based on the agreement between the invoicing service and the performer of the work, the invoicing service deducts its own fee and the employer's social insurance contributions from the EUR 500. The invoicing service pays EUR 350 in wages to the person. The pay also includes EUR 40 in travel expenses. Because an overall remuneration has been agreed, the invoicing service does not reimburse the travel expenses in addition to the wages; instead, the payer deducts the amount of travel expenses before withholding tax. The travel expenses are taxable income of the recipient. The total amount of wages and travel expenses are reported as the amount of wages.

If the performer of the work and the client have agreed that reimbursements of travel expenses are paid in addition to invoiced remuneration, the invoicing service company will submit a report to the Incomes Register using the income types of tax-exempt travel expenses: Daily allowance, Meal allowance, Kilometre allowance (tax-exempt). This requires that the travel expenses are in accordance with the Tax Administration's decision on tax-exempt reimbursements of travel expenses. If reimbursements have been paid against the time and kilometre limits set by the decision of the Tax Administration, they are wages. For more information, see the Guidelines Reporting data to the Incomes Register: fringe benefits and reimbursements of expenses, Section 2 Reimbursement of expenses.

Example 9: A person has performed work for a client worth EUR 500, invoiced by the invoicing service from the client. The person has agreed with the client that the client will also be invoiced for the travel expenses in addition to the remuneration. A kilometre allowance of EUR 41 (100 km) is itemised on the invoice. The total amount on the invoice is EUR 541.

The person and the invoicing service have agreed that the person is in an employment relationship with the invoicing service. The person has taken out a YEL insurance, because the earnings-related pension provider has deemed that there was no employment relationship between the person and the invoicing service with respect to labour legislation. The invoicing service pays the person EUR 390 in wages and EUR 41 in tax-exempt kilometre allowance.

If the performer of the work and the invoicing service company have not made an agreement on an employment relationship, the amount paid to the performer of the work is non-wage compensation for work, see Section 3.1, Non-wage compensation for work.

4 Compensation for use

Compensation for use is compensation laid down in the tax prepayment act (ennakkoperintälaki 1118/1996), paid for the use, right of use or sale of the right of use of a copyright, photograph-related right or an industrial property right such as a patent or trademark.

The compensation for use can be taxable earned income or taxable capital income. If a copyright has been transferred as an inheritance or through a will, or it has been bought, the compensation received from its use is taxable capital income. Tax is withheld at the capital income rate. Otherwise, the compensation for use is taxable earned income, and tax is withheld in the same manner as from non-wage compensation for work. Tax is not withheld if the payment recipient is registered in the prepayment register.

The payer must report all compensations for use, from which tax has been withheld, to the Incomes Register. Compensation for use paid to natural persons must be reported, even if tax has not been withheld from it. Compensation for use paid to natural persons registered in the prepayment register must also be reported. Compensations for use paid to a general partnership, limited partnership, limited liability company, cooperative or joint venture must be reported to the Incomes Register if the recipient is not registered in the prepayment register. The data is reported to the Incomes Register using the income type Compensation for use, earned income. Type of additional income earner data: Organisation must also be reported.

No social insurance contributions are paid on compensation for use.

Compensation for use that is earned income is reported using the income type Compensation for use, earned income. Compensation for use that is capital income is reported using the income type Compensation for use, capital income. Any value added tax or reimbursement of expenses are not deducted from the amount of compensations for use reported.

4.1 Reimbursement of expenses related to compensation for use

The reimbursement of expenses related to compensations for use are included in the amounts of the income types Compensation for use, earned income and Compensation for use, capital income, and they are not separately reported. This is because reimbursement of expenses paid by parties other than the employer is not tax-exempt.

Recipients of compensation for use can request that travel expenses be deducted in their taxation. However, business operators must deduct travel expenses in their accounting.

Reimbursement of expenses related to work cannot usually be deducted from compensation for use before tax is withheld. The only exception to this is the reimbursement of travel expenses paid to natural persons. Tax does not need to be withheld from this reimbursement if the grounds and amounts of the travel expenses are in accordance with the tax-exempt allowances for business travel laid down in the annual decision issued by the Tax Administration. These allowances are not tax-exempt either, so they are reported in the total amount of the compensation for use.

5 Other payments based on separate tasks

5.1 Athlete

5.1.1 Athlete's wages

Wages paid to an athlete mean wages paid for sports activities based on an athlete contract. An athlete contract is equivalent to an employment contract. The athlete's wages are typically wages paid to a member of a sports team based on a player contract. The amount of the wages does not include wages transferred to an athletes' special fund.

The athlete's statutory insurance premium is based on the athlete's wages in accordance with the act on athletes' accident and pension insurance (laki urheilijan tapaturma- ja eläketurvasta 276/2009). The act lays down provisions on the athlete's minimum level of earnings. Once this minimum level has been reached, the sports employer must take out accident and pension insurance for the athlete. An athlete's pension contribution is not paid for the same pension insurance as other wage earners. However, athlete's pension contributions are also reported to the Incomes Register using the income type Employee's earnings-related pension insurance contribution, so that the payment data is relayed to taxation.

The income is subject to employer's health insurance contribution.

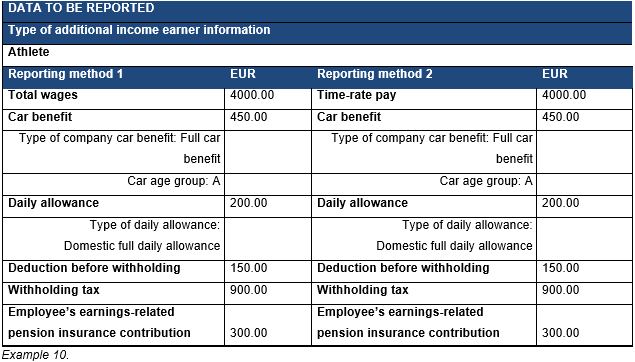

Type of additional income earner data: Athlete is reported for the wages paid to an athlete. Otherwise, the wages are reported using wage income types, such as the income types Total wages or Time-rate pay. The wage income types are used to report only the wages directly paid to the athlete. If the payment is made into an athletes' special fund, see Section 5.1.3, Wages transferred to athletes' special fund.

If the payment is made from athletes' special fund, see Section 5.1.4, Wages paid from athletes' special fund.

Example 10: An athlete has been paid EUR 4,000 in wages. In addition to the monetary wages, the athlete has a full car benefit, age group A, which is EUR 450 in value. The athlete has been paid EUR 200 in daily allowances. The athlete has paid EUR 150 of direct costs incurred in sports activities (equipment). EUR 300 of pension insurance contributions have been collected from the athlete in accordance with the act on athletes' accident and pension insurance.

5.1.2 Athlete's fees

Fees paid to athletes include competition prizes, fees based on advertising and sponsorship agreements, participation fees and other fees based on their status as an athlete, where the recipient is not in an employment relationship with the payer. Athlete's fees are typically paid to athletes involved in individual sports. Fees paid to an athlete that are not based on an employment relationship are payments treated in taxation in the same way as non-wage compensation for work. When reporting these fees to the Incomes Register, specify Type of additional income earner data: Athlete. Athlete's fees are reported using the income type Non-wage compensation for work.

Tax must always be withheld from an athlete's fee if the payment is made to a natural person. International situations are described in the Guidelines Reporting data to the Incomes Register: international situations.

Reimbursements of travel expenses paid to a recipient of athlete's fees have not been decreed to be tax-exempt (however, see Section 5.11, Reimbursement paid by a non-profit organisation). In taxation practice, however, it has been established that reimbursements of travel expenses paid to recipients of athlete's fees are accepted as tax-exempt on the same conditions as those of wage earners. If a kilometre allowance is paid to an athlete, the amount of tax-exempt kilometre allowance is reported using the income type Kilometre allowance (tax-exempt). Also specify the Number of kilometres. For more information, see Sections 2.1.1, Kilometre allowance (tax-exempt), 2.1.3, Daily allowance, and 2.1.4, Meal allowance, of the Guidelines Reporting data to the Incomes Register: fringe benefits and reimbursements of expenses.

If an athlete's fee is paid from an athletes' special fund, this is also reported using the income type Non-wage compensation for work and by specifying Type of additional income earner data: Athlete. If an athlete withdraws funds from a training fund without receipts, the training fund will report the payment using the income type Non-wage compensation for work and by specifying Type of additional income earner data: Athlete.

5.1.3 Wages transferred to athletes' special fund

An athlete can transfer his or her income from sports to a national training fund or athletes' special fund linked to a foundation appointed by the Ministry of Finance. The transfer to the athletes' special fund is intended to secure the athlete's post-career livelihood.

Income from sports can comprise the athlete's wages or fees. The income type Wages transferred to athletes' special fund is used to report to the Incomes Register only the wages transferred to the fund. Additionally, specify Type of additional income earner data: Athlete. If an athlete's fee is transferred to the athletes' special fund, this is not reported to the Incomes Register.

The employer's health insurance contribution is paid from the athlete's wages transferred to the fund. The athlete does not pay tax for the income until the income is paid out from the fund. Tax is not withheld from the funded wages until the wages are paid to the athlete from the fund.

The funding of income from sports does not affect the payment of the insurance premiums specified in the act on athletes' accident and pension insurance.

5.1.4 Withdrawals from athletes' special fund

The fund withholds tax from the athlete's wages and fees withdrawn from the athletes' special fund when the athlete makes a withdrawal.

Items withdrawn from the fund must be itemised into wages and fees, because they are subject to different deductions in taxation. The income type Wages paid from athletes' special fund is only used to report to the Incomes Register the wages paid from the fund. An athlete's fee paid from the fund is reported using the income type Non-wage compensation for work. All payments must also include Type of additional income earner data: Athlete.

Tax is withheld from the funded wages and the employee's health insurance daily allowance contribution is paid when wages are paid to the athlete from the fund. The employer's health insurance contribution is paid when the income is transferred to the athletes' special fund.

5.1.5 Training fund

Athlete's fees can be transferred to a training fund. During a tax year, tax-exempt funds can be drawn from the fund against a receipt to cover sports and training expenses. Such withdrawals are not reported to the Incomes Register.

The part of funds transferred to a training fund during a certain tax year, and not used during the same tax year, is transferred as the recipient's income for the tax year. This income is reported to the Incomes Register using the income type Non-wage compensation for work, also specifying the Type of additional income earner data: Athlete. Similarly, the taxable payments drawn during the tax year are also reported.

According to a decision by the Tax Administration, the training fund must report the tax-exempt training costs paid to athletes during the year. These mean tax-exempt reimbursements of travel expenses paid from the training fund against a travel invoice, reported to the Incomes Register in the manner described in Section 5.1.2, Athlete's fees.

Funds can also be transferred from the training fund to the athletes' special fund. These transfers are not reported to the Incomes Register. The reporting of an athlete's fee drawn from the athletes' special fund is described in Section 5.1.4, Withdrawals from athletes' special fund.

An athlete can draw funds from the training fund based on the wages he or she pays to a trainer or on a non-wage compensation for work (invoice). The training fund does not report these payments to the Incomes Register; instead, the athlete submits the report, because he or she acts as the trainer's employer (wages) or service recipient (non-wage compensation for work).

5.2 Performing artist

Performing artists include stage and film actors, radio and television performers, and musicians.

When payments made to a performing artist for work in this role are reported to the Incomes Register, also specify Type of additional income earner data: Performing artist.

If the payment of a performing artist's remuneration is based on an employment relationship, and the remuneration is related to duties agreed in the employment contract, such remuneration is treated as wages, i.e., tax is withheld and social insurance contributions are paid from it. The income is reported using wage income types, for example Total wages or Contract pay.

If a performing artist performs based on a commission relationship, the remuneration paid to the artist is reported using the income type Non-wage compensation for work. Tax must be withheld from such compensation, if the recipient is not registered in the prepayment register. No social insurance contributions are paid from the income unless the payer is a public sector payer and the income earner is not insured in accordance with the self-employed persons' pensions act. For more information, see Section 3.1, Non-wage compensation for work. Non-wage compensation for work, paid to a performing artist, is not reported to the Incomes Register if the income earner is registered in the prepayment register.

5.3 Compensation for the Managing Director and for membership of a governing body

Compensation paid for work performed in an employment relationship is deemed wages. Additionally, certain payments listed in the tax prepayment act (ennakkoperintälaki 1118/1996) are deemed wages even if an employment relationship is not established:

- meeting fee

- personal lecture and presentation fee

- compensation for membership of a governing body

- Managing Director's compensation

- wages drawn by a partner in a general or limited partnership

- compensation for acting in a position of trust.

In addition to monetary wages, the payer can grant fringe benefits deemed wages to the Managing Director and a member of a governing body (such as company car, meal and telephone benefit) and pay tax-exempt reimbursement of travel expenses.

Social insurance contributions must be paid from the Managing Director's compensation. The compensation is reported to the Incomes Register either using the income type Total wages (reporting method 1) or one of the income types of reporting method 2, for example the income type Time-rate pay.

Compensation paid for membership of a governing body is reported to the Incomes Register using the income type Compensation for membership of a governing body. The default for this income type is that the recipient is in an employment relationship with the payer and the income is thus subject to social insurance contributions.

If the employee's earnings-related pension insurance contribution does not need to be paid from the compensation under the employment pension act applicable to the member of a governing body, neither are other social insurance contributions paid from the compensation. In such a situation, the payer reports the insurance information using the separate Insurance information type entry, specifying Subject to social insurance contributions: No. If, in this kind of a situation, voluntary earnings-related pension insurance has been taken out for a member of a governing body, no other social insurance contributions need to be paid. In such a case, the Insurance information type entry is reported as Subject to health insurance contribution: No, Subject to unemployment insurance contribution: No and Subject to accident and occupational disease insurance contribution: No.

If compensation for membership of a governing body is paid by a public sector organisation, the earnings-related pension insurance contribution and the employer's health insurance contribution are paid. In such a situation, the payer reports the insurance information using the separate Insurance information type entry, specifying Subject to accident and occupational disease insurance contributions: No and Subject to unemployment insurance contribution: No.

5.4 Family day care provider's wages and reimbursement of expenses

The wages paid to a family day care provider are reported to the Incomes Register in the same way as any other wages. The income type is Family day care provider's wages. The entire amount of the monetary wages is reported as the wages, and no deductions are made from it before tax withholding.

The income type Reimbursement of family day care provider's expenses is used to report the taxable reimbursement to the Incomes Register of expenses paid to a family day care provider to cover the direct expenses incurred by childminding. The reimbursement of expenses paid to a family arranging three-family day care is also reported using the income type Reimbursement of family day care provider's expenses. Reimbursed expenses include, for example, expenses incurred from meals. Each year, the Association of Finnish Local and Regional Authorities issues a recommendation on the reimbursement of family day care providers' expenses to municipalities.

No tax is withheld or social insurance contributions are paid from the reimbursement of expenses paid to a family day care provider.

5.5 Private caretaker's fee and reimbursement of expenses

A municipality uses the income type Private caretaker's fee to report to the Incomes Register the fee paid to a private caretaker for arranging treatment, upbringing or other around-the-clock care in the caretaker's private home or in the home of the person cared for.

The private caretaker's fee is based on a commissioning contract between the municipality and the private caretaker. An earnings-related pension insurance contribution is paid from the private caretaker's fee, but no other social insurance contributions are paid. However, the municipality must insure the carer for accidents in such work. Provisions on a private caretaker's accident insurance are laid down in the separate legislation on private caretakers.

The private caretaker's fee is handled as non-wage compensation for work from which tax is withheld, if the recipient of the fee is not registered in the prepayment register.

The income type Reimbursement of private caretaker's expenses is used to report to the Incomes Register the taxable reimbursement of expenses paid to a private caretaker to cover the expenses incurred by the care and upkeep of foster home care patients. Reimbursement of a private caretaker's expenses is based on a commissioning contract between the municipality and the private caretaker. Such reimbursement covers items such as meal, accommodation and health care expenses, as well as start-up expenses.

No tax is withheld or social insurance contributions are paid from the reimbursement of expenses.

5.6 Kinship carer's fee

The income type Kinship carer's fee is used to report to the Incomes Register a fee paid by the municipality to a kinship carer for arranging treatment and care for an elderly, disabled or ill person at home. The kinship carer's fee is based on a commissioning contract between the municipality and the kinship carer, and its amount is determined by how binding and demanding the care is.

The kinship carer's fee is handled as non-wage compensation for work from which tax is withheld if the recipient of the fee is not registered in the prepayment register. An earnings-related pension insurance contribution is paid from the kinship carer's fee, but other social insurance contributions are not. However, the municipality must insure the carer for accidents during such work, under the special law applied.

5.7 Lay helper

Lay helper activities can be voluntary work for which a fee, reimbursement of expenses, or both can be paid. The purpose of the lay helper is to support the growth and development of a child. The lay helper can also provide support to the entire family. A fee paid to a lay helper for voluntary work is reported to the Incomes Register using the income type Non-wage compensation for work. For the reimbursement of expenses related to the fee, see Section 3.1.1, Reimbursement of expenses related to non-wage compensation for work.

5.8 Elected official fee

The elected official fee is collected from the meeting fees of elected municipal officials to be paid to political parties. The elected official fee may only be reported by municipalities and joint municipal authorities.

The remuneration paid to a person in a position of trust is reported using the Meeting fee, Compensation for acting in position of trust or Total wages income types, depending on the grounds of the payment.

If the income earner acting in a position of trust has paid the elected official fee directly to a political party, the fee is not reported to the Incomes Register. The political party reports the fee to the Tax Administration on its annual return.

Compensation for acting in a position of trust is not reported if it has been collected for a position other than a municipal position of trust, such as a membership of a board of directors of a limited liability company or another civil law corporation.

5.9 Reimbursement of costs, paid to conciliator

The income type Reimbursement of costs, paid to conciliator is used to report to the Incomes Register a taxable reimbursement of costs paid to a voluntary conciliator to cover the costs incurred from the conciliation process. Conciliator means a conciliator as defined by the Act on Conciliation in Criminal and Certain Civil Cases.

No tax is withheld or social insurance contributions are paid from the reimbursement of costs.

5.10 Allowance to witness

An allowance to witness is paid for appearing in court as a witness. The allowance is a non-wage compensation for work, unless an agreement has been made to pay it as wages. Tax is withheld from such compensation if the recipient is not registered in the prepayment register. No other social insurance contributions are paid. The allowance to witness is reported to the Incomes Register using the income type Non-wage compensation for work; for more information, see Section 3.1, Non-wage compensation for work.

The reimbursements of expenses paid in connection with non-wage compensations for work are taxable. No tax is withheld or social insurance contributions are paid from these compensations. The reporting of the compensations to the Incomes Register is described in Section 3.1.1, Reimbursements of expenses related to non-wage compensation for work. Reimbursements for the costs of taking evidence, paid from State funds, are tax-exempt. They are not reported to the Incomes Register.

If an allowance to witness is paid as wages, it is reported to the Incomes Register using, for example, the income type Total wages.

5.11 Reimbursement paid by a non-profit organisation

Non-profit organisations include labour market organisations, youth associations, sports clubs, and organisations supporting science and arts.

A non-profit organisation can pay certain compensations to a person who volunteers for unpaid work without an employment relationship. The organisation can pay a tax-exempt kilometre allowance equivalent to commuting for the use of a car that is owned by the person or is in his or her possession, and a domestic full or partial daily allowance or an international daily allowance. However, a meal allowance is not tax-exempt. For the reimbursement of travel expenses to be tax-exempt, the requirement is that the trip was made for the benefit of the organisation at its commission and it was properly agreed in advance. For example, an instructor's trips on training locations, representative missions to congresses, trips to pick up goods for a sale and an athlete's competition and training trips can entitle a person to a tax-exempt reimbursement. The reimbursed trip can begin from the recipient's home. Membership of the organisation is not a requirement for payment.

There are recipient-specific limits to tax-exempt reimbursements. In one calendar year, a person may receive a tax-exempt daily allowance for no more than twenty days and a tax-exempt kilometre allowance of no more than EUR 2,000. These limitations do not apply to reimbursements of accommodation expenses or travelling on public transport. The grounds for paying the daily allowance and the kilometre allowance are determined according to the annual decision of the Tax Administration on the tax-exempt reimbursements of travel expenses.

Tax-exempt reimbursements of travel expenses can be paid to recipients of an athlete's or competition judge's fees based on the above-mentioned grounds and limitations, even if they also receive a separate fee as a non-wage compensation for work. The competition or event must be related to the activities of the non-profit organisation.

The payer only keeps track of the amounts it has paid. It cannot know the reimbursements possibly paid by other non-profit organisations. If a non-profit organisation pays more reimbursements of travel expenses than decreed in the income tax act (tuloverolaki 1535/1992) or on grounds more lenient than those subject to the decision of the Tax Administration, the excess part is reported as non-wage compensation for work. However, no tax is withheld from this amount if the recipient is a natural person.

Social insurance contributions are not paid for tax-exempt or taxable reimbursements.

The amount of tax-exempt kilometre allowances paid by a non-profit organisation is reported to the Incomes Register using the income type Kilometre allowance paid by non-profit organisation.

The amount of tax-exempt daily allowances paid by a non-profit organisation is reported to the Incomes Register using the income type Daily allowance paid by non-profit organisation.

The taxable amount exceeding the tax-exempt kilometre allowance or daily allowance paid by a non-profit organisation is reported to the Incomes Register as non-wage compensation for work using the income type Non-wage compensation for work.

Additionally, a non-profit organisation can pay reimbursements for travel expenses against a receipt from a transport operator. These reimbursements are not reported to the Incomes Register.

Example 11: As agreed in advance, a non-profit organisation paid EUR 150 of tax-exempt kilometre allowances to its voluntary instructor for running children's exercise sessions. The instructor also represented the organisation at a general assembly, with the organisation paying one tax-exempt daily allowance and one partial daily allowance (totalling EUR 45) for the trip, as well as train tickets and accommodation in a hotel. The organisation reports the kilometre allowance and the daily allowances to the Incomes Register. The public transport ticket and reimbursement of accommodation expenses are not reported.

Example 12: Early in the year, a sports club has paid EUR 1,800 of tax-exempt kilometre allowances to an athlete representing the club. These have already been reported to the Incomes Register.

In November, EUR 600 more in kilometre allowance is paid to the same athlete for a competition trip. In November, the sports club reports EUR 200 using the income type Kilometre allowance paid by non-profit organisation and the taxable part exceeding EUR 2,000, EUR 400, using the income type Non-wage compensation for work.

If a recipient of a kilometre allowance or a daily allowance is in an employment relationship with a non-profit organisation, or is otherwise paid wages or other taxable remuneration by the organisation, the kilometre allowance and daily allowance are reported in connection with the payments in question according to the relevant instructions (Reporting data to the Incomes Register: fringe benefits and reimbursements of expenses, Section 2.1, Tax-exempt reimbursement of travel expenses paid to an employee).

For the reimbursement of travel expenses paid by a non-profit organisation, see the Tax Administration's Guidelines Prepayment questions for the volunteering of non-profit organisations and public sector organisations (in Finnish).

5.12 Voluntary perquisite

Voluntary perquisites include perquisites paid to waiters or restaurant doormen (tip, extra) by their customers.

If the perquisite is based on work performed in an employment relationship, the employer reports the perquisite to the Incomes Register using the income type Total wages or, for example, the income type Other compensation. The employer does not need to withhold tax from the income, because the income is subject to pre-assessment. However, the employer must pay the employer's social insurance contributions.

If the recipient of the perquisite is not in an employment relationship and is not registered in the prepayment register, the service recipient reports the voluntary perquisites to the Incomes Register using the income type Non-wage compensation for work and the amount of tax withheld using the income type Withholding tax. A payment made to someone registered in the prepayment register is not reported to the Incomes Register.

5.13 Other taxable income deemed earned income

The income type Other taxable income deemed earned income is used to report taxable occasional remunerations and rewards, when the recipient is not in an employment relationship with the payer and the payment is not compensation for work. These include, for example, a competition prize not based on an employment relationship, a benefit granted to a member of a customer company's personnel or otherwise based on a customer relationship (e.g. a trip, gift voucher or object), a finder's fee, a so-called vigilance fee paid by a bank, a prize from an art competition, and travel compensation paid by a municipality to its residents.

Other taxable income deemed as earned income is subject to withholding but not to social insurance contributions. From the perspective of reporting, it does not matter whether or not tax could be withheld from the income.