Reporting data to the Incomes Register: insurance-related data

- Date of issue

- 2/13/2019

- Record no.

- VH/693/00.01.00/2019

- Validity

- 2/13/2019 - 12/22/2019

The instructions describe how to report employer's and employee's social insurance contributions to the Incomes Register with an earnings payment report. These instructions are intended to be used by payers. They also describe how to report information when

- the income earner is not subject to Finnish social security

- the payer is not under an obligation to insure the income earner, for example if the amount of income paid falls below the threshold for insurance

- the type of income paid is not subject to social insurance contributions.

The instructions include examples of how to report different insurance information.

These instructions replace the earlier instructions titled Reporting data to the Incomes Register: insurance-related data. The texts and examples in the instructions have been clarified. The list of earnings-related pension providers in Section 3 has been updated. A text and an example concerning the topic of 'Reporting Reimbursement collected for other fringe benefits' have been added to Section 1.3. Otherwise the instructions are similar in outline to the earlier instructions.

1 Reporting of insurance details

1.1 Employer's and employee's social insurance contributions

The employer must pay social insurance contributions for the wages paid and other payments made to employees. The employer's social insurance contributions are

- the employer's health insurance contribution

- the employer's unemployment insurance contribution

- the employer's earnings-related pension insurance contribution

- the accident and occupational disease insurance contribution

- the group life insurance premium required by the employment or public-sector employment contract.

The employee's social insurance contributions are

- the daily allowance contribution of health insurance

- the health care contribution of health insurance

- the employee's unemployment insurance contribution

- the employee's earnings-related pension insurance contribution.

The employer is obliged to pay both the employee's and the employer's social insurance contributions. The employer collects the employee's share of the contributions from the wages paid to the employee and forwards the contributions to the party in charge of managing the social insurance. The employer need not pay and collect these contributions only if the income earner is not subject to social security in Finland, the payer is not under an obligation to insure the income earner, or the type of income paid is not subject to social insurance contributions.

The payer is obliged to withhold tax from all income items subject to withholding. If the employee is insured in Finland, the withholding includes the employee's health insurance contribution.

The insurance process in situations involving a substitute payer is described in the instructions Reporting data to the Incomes Register: payments made by substitute payer.

1.2 Social insurance contributions may vary between income types

The employer reports the payments made to the Incomes Register based on the income types. Each income type has a default for the payment of social insurance contributions. If the income is paid according to the default, the employer will not have to specially determine the social insurance contributions when submitting the report.

For certain income types, depending on the situation, the basis for social insurance contributions may be different even if the payer is the same. For example, the basis for the payment of social insurance contribution may be whether the recipient of the payment is in an employment relationship or not. The social insurance contributions may vary for the following income types:

- initiative fee (202)

- compensation for membership of a governing body (308)

- monetary gift for employees (310)

- meeting fee (210)

- lecture fee (214)

- compensation for acting in a position of trust (215)

- reimbursement collected for other fringe benefits (407)

- other taxable benefit for employees (315)

- other fringe benefit (317)

- total wages (101)

- compensation for employee invention (326)

- stock options and grants (320)

- partial pay during sick leave (219)

- share issue for employees (226)

- profit-sharing bonus (233)

- wages for insurance purposes (352)

The default for the listed income types is that they are subject to some or all of the social insurance contributions, or that they are not subject to any social insurance contributions. The page Income types has information on which social insurance contributions are the default for which income type. In the instruction Descriptions of income types and items deducted from income on the Documentation page, the situations in which the social insurance contributions for the above income types may vary are described separately for each income type.

If the payment made under the income type differs from the default, the employer selects Yes or No for Type of insurance information, according to which type of income is the grounds for the insurance contribution. The employer may use all the types of insurance information listed in Section 1.3. If the income is paid according to the default, the information on social insurance contributions does not need to be separately confirmed.

1.3 Type of insurance information

When the insurance information for the income type differs from the default, the payer must report the Type of insurance information. The Type of insurance information is given separately for all the income types concerned.

The types of insurance information to be reported to the Incomes Register:

- Subject to social insurance contributions (all social insurance contributions)

- Subject to earnings-related pension insurance contribution

- Subject to health insurance contribution

- Subject to unemployment insurance contribution

- Subject to accident insurance and occupational disease insurance contribution

The alternative 'Subject to social insurance contribution' covers all social insurance contributions of both the employer and the employee. The alternatives 'Subject to earnings-related pension insurance contribution', 'Subject to health insurance contribution', and 'Subject to unemployment insurance contribution' cover both the employer's and the employee's contributions.

If the payment is made according to the default income type, the payer does not have to report any information on social insurance contributions.

If the income type is by default not subject to social insurance contributions but the payment to be made is subject to all social insurance contributions:

- Use the Type of insurance information 'Subject to social insurance contributions – Grounds for insurance contribution: Yes'.

- This eliminates the need to separately confirm the information for all of the different social insurance contributions.

If the income type is by default subject to social insurance contribution but the payment to be made has no parts that are subject to social insurance contributions:

- Use the Type of insurance information 'Subject to social insurance contributions – Grounds for insurance contribution: No’.

- This eliminates the need to separately confirm the information for all of the different social insurance contributions.

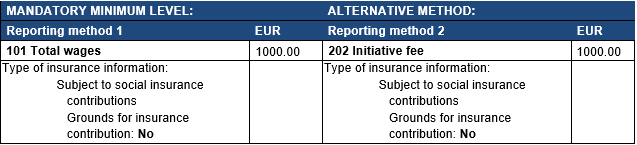

Example 1: The employer pays the income earner an initiative fee of EUR 1,000. The employer can report the income under the 'Total wages' income type (reporting method 1) or alternatively under the supplementary 'Initiative fee' income type (reporting method 2).

The default value of both the 'Total wages' income type and the 'Initiative fee' income type under reporting method 2 is that the payment is subject to social insurance contributions. However, the initiative for which the fee is paid to the income earner is not connected to the duties agreed in the employee's employment contract, for which reason the income is not subject to social insurance contributions in these situations.

Reported in either way, the payer must use the Type of insurance information data to specify that the income is not subject to social insurance contributions.

The payer reports the income by using either reporting method 1 or reporting method 2:

Based on the Type of insurance information given, no social insurance contributions are payable on the payment.

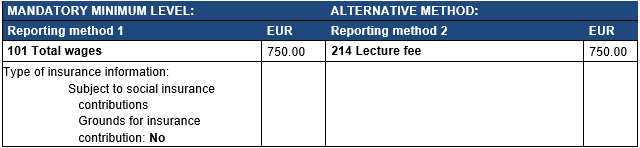

Example 2: The income earner has given a lecture at an event arranged by a private training company. He is not employed by the training company. The lecture fee has been agreed to be EUR 750. By default, the 'Lecture fee' income type under reporting method 2 is not subject to social insurance contributions. Because, in the case in question, the recipient of the lecture fee is not in an employment relationship with the payer, and the payer is subject to employee's pension insurance under TyEL, the fee is not subject to social insurance contributions (earnings-related pension insurance contribution, unemployment insurance contribution, health insurance contribution, or accident and occupational disease insurance).

The payer can also report the paid income as a total amount as per reporting method 1. When the reporting method 1 'Total wages' income type is used, the Type of insurance information must be separately used to confirm that the income reported in accordance with reporting method 1 is not subject to social insurance contributions.

The payer reports the income by using either reporting method 1 or reporting method 2:

If only one of the payment's social insurance contributions differs from the default, the Type of insurance information of the social insurance contribution concerned must be used.

For example, if the payment to be made is not subject to a health insurance contribution in contrast to the default of the income type, but the other contributions are in accordance with the default:

- With the income type, use the Type of insurance information 'Subject to health insurance contributions – Grounds for insurance contribution: No’.

Correspondingly, if the payment to be made is, for example, subject to earnings-related pension insurance contribution and the income type is, by default, not subject to earnings-related pension insurance contributions, but the other contributions are in accordance with the default:

- With the income type, use the Type of insurance information 'Subject to earnings-related pension insurance contributions – Grounds for insurance contribution: Yes'.

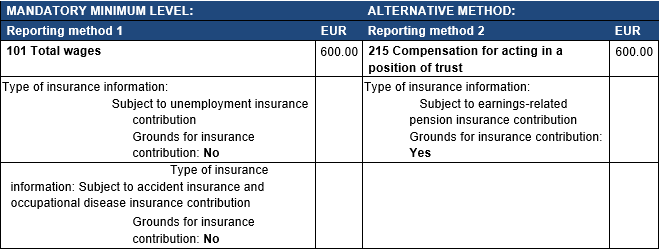

Example 3: The income earner is paid EUR 600 compensation for acting in a position of trust. The default of the 'Compensation for acting in a position of trust' income type as per reporting method 2 is that it is not subject to pension, unemployment or accident and occupational disease insurance contributions. However, the income type is subject to a health insurance contribution.

The payer has, however, taken out voluntary earnings-related pension insurance for the person acting in a position of trust, due to which the pension is based on the income.

The payer reports the income by using either reporting method 1 or reporting method 2:

Based on this information, the health insurance contribution and earnings-related pension insurance contribution are collected from the payment, but the unemployment insurance contribution or the accident and occupational disease insurance contribution is not.

If the payer uses the 'Compensation for acting in a position of trust' income type and the reporting method 2, the default payments do not need to be confirmed. When reporting method 1 is used, by default the income is subject to social insurance contributions and, therefore, when reporting compensation for acting in a position of trust, the payer must use the Type of insurance information to confirm that the income is not subject to unemployment or accident and occupational disease insurance contributions.

If only a certain portion of the payment is made in contrast to the default income type, the data must be given separately for the income types for which social insurance contributions are paid according to the default and those income types which differ from the default.

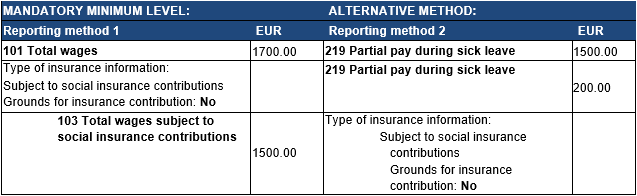

Example 4: The employer pays EUR 1,700 in partial pay during sick leave to the income earner. Both the 'Total wages' income type and 'Partial pay during sick leave' income type are income that is subject to social insurance contributions by default. The paid amount includes EUR 200 that is not subject to social insurance

The payer reports the income by using either reporting method 1 or reporting method 2:

Based on the data submitted, social insurance contributions are paid on EUR 1,500, but not on the separately reported EUR 200, which includes the separate Type of insurance information 'Subject to social insurance contributions – Grounds for insurance contribution: No'.

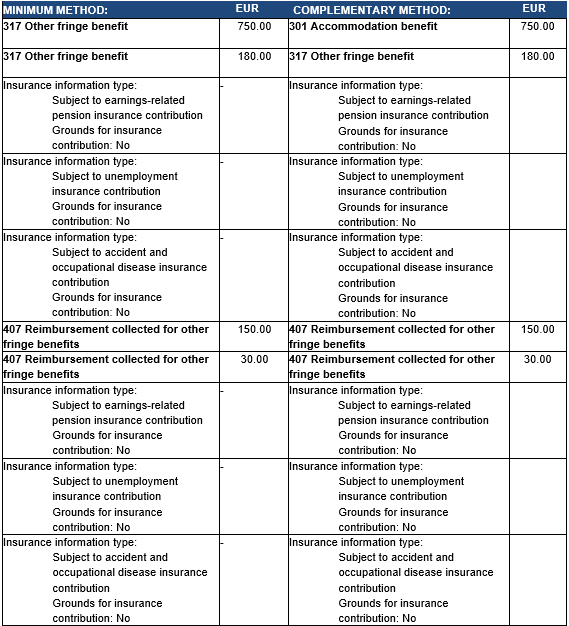

Reporting Reimbursement collected for other fringe benefits

The share of the value of a fringe benefit, which is collected from the employee, is reported using the income type Reimbursement collected for other fringe benefits (407). In this section, report the amount collected from the employee for fringe benefits other than a car benefit or employer-subsidised commuter ticket benefit.

The amount of the fringe benefit is reported in full using the appropriate income type. The deductible collected from an employee is reported using the income type Reimbursement collected for other fringe benefits. If the reimbursement collected for a meal benefit equals the taxable value, the collected reimbursement is not reported using the income type Reimbursement collected for other fringe benefits. In this case, only the data Reimbursement for meal benefit corresponds to the taxable value – Yes is reported. The employer may collect the reimbursement for fringe benefits from the net wages of the employee.

If the fringe benefit reported with the income type Other fringe benefit (317) is not subject to social insurance contributions and the payer has reported this by using the Type of insurance information data group, the equivalent Type of insurance information data must also be added to the income type Reimbursement collected for other fringe benefits, insofar as the collected reimbursement concerns the share of the benefit which is not subject to social insurance contributions.

Even though the income type, by default, is not subject to social insurance contributions, the payer must confirm the data in the report as described above. This ensures that the Income Register's data users will obtain the correct data.

Example: An income earner receives an accommodation benefit of EUR 750, from which the payer has collected EUR 150 as reimbursement. Social insurance contributions are paid from the accommodation benefit. In addition, the employer issues a benefit of EUR 180, which is not subject to earnings-related pension, unemployment or accident and occupational disease insurance contributions. The payer has collected EUR 30 as reimbursement from this benefit.

The payer reports the data in the following manner:

2 Reporting of health insurance details

Employee's health insurance contribution

The employee's health insurance contribution includes the health insurance daily allowance contribution and the health insurance medical care contribution. By paying the daily allowance contribution, the employee participates in financing the earned income insurance and by paying the health care contribution to financing the health insurance.

The employee's health insurance contribution is included in the income earner's withholding tax or, alternatively, the Tax Administration collects it in connection with tax prepayment on the basis of the income types reported to the Incomes Register. In the above cases, the employer does not separately report the employee's health insurance contribution to the Incomes Register.

If the employee is a non-resident for tax purposes in Finland and the wage income they earn is subject to tax at source, the employer must collect the health insurance contribution from the pay and report it to the Incomes Register separately under the income type 'Employee's health insurance contribution' in addition to tax at source. The employer makes the payment to the Tax Administration. These types of situations are described in more detail in the instructions Reporting data to the Incomes Register: international situations, in Section 2.6.1.2.

The Tax Administration forwards the payments to the health insurance fund administered by Kela. The amounts of the contributions are confirmed annually by Government decree.

Employer's health insurance contribution

The employer's health insurance contribution is determined based on the pay subject to health insurance contributions paid to insured employees. By paying the contribution, the employer participates in financing the compensations paid from the health insurance fund. The employer reports the total amount of the employer's health insurance contribution the employer has calculated and the deductions to be made on the employer's health insurance contribution to the Incomes Register on the employer's separate report. The employer makes the payment to the Tax Administration.

The Tax Administration forwards the employer's health insurance contribution to the health insurance fund administered by Kela. The amount of the contribution is confirmed annually by Government decree.

The employee's and employer's health insurance contributions are determined on the basis of the income types reported to the Incomes Register. Section 1.3 has a list of the income types in which the payer can change the control rule for the social insurance contribution.

The exceptions to insurance are described in Section 6.

3 Reporting of earnings-related pension insurance details

The employee's and employer's earnings-related pension insurance contributions are determined based on the wages subject to the earnings-related pension insurance contribution. By paying earnings-related pension insurance contributions, the employee and the employer participate in financing the earnings-related pension insurance.

The employer pays the authorised earnings-related pension provider a total amount which includes both the employer's earnings-related pension insurance contribution and the employee's earnings-related pension insurance contribution. Of these, only the employee's share is reported to the Incomes Register as an item deductible from pay (a separately reported income type 413). The employer's contributions are calculated by the insurance provider based on the reported income types.

Income earner's earnings-related pension insurance information

The payer must report the earnings-related pension insurance under which the income earner is insured:

- Employee's earnings-related pension insurance

- Pension insurance for farmers (MYEL)

- Pension insurance for the self-employed (YEL).

Only one earnings-related pension insurance information can be reported for the income earner in the same earnings payment report.

Employee's earnings-related pension insurance is selected if the income earner is insured under the following legislation

- Employees Pensions Act (TyEL 395/2006)

- public sector pensions act (julkisten alojen eläkelaki (JuEL) 81/2016)

- seafarers' pensions act (merimieseläkelaki (MEL) 1290/2006)

- act on the Orthodox Church (laki ortodoksisesta kirkosta 985/2006)

- a pension rule in accordance with the act on the Bank of Finland (laki Suomen Pankista 214/1998)

- a pension rule in accordance with the provincial law of the Åland Islands (ÅFS 54/2007).

MYEL is selected if the income earner is insured under the farmers' pensions act (maatalousyrittäjän eläkelaki 1280/2006).

YEL is selected if the income earner is insured under the self-employed persons' pensions act (yrittäjän eläkelaki 1272/2006).

If the income earner is insured under MYEL or YEL the payer must report 'MYEL' or 'YEL' on each earnings payment report. No other earnings-related pension insurance information must be given, otherwise the data users of the Incomes Register will handle the income data twice and this may result in double payments being imposed.

Pension provider code

If the income earner has earnings-related pension insurance, the payer must provide the pension provider code on the earnings payment report. Codes for authorised earnings-related pension providers:

10 Finnish Centre for Pensions

16 Ortodoksisen kirkon papiston eläkekassa

20 Keva's member corporations

24 Keva - Åland landskapsregerings pensionssystem

25 Keva - Church

27 Bank of Finland

29 Keva - Kela employment pensions

30 Keva - State

34 Seafarer's Pension Fund

35 Farmers' Social Insurance Institution (Mela)

46 Ilmarinen Mutual Pension Insurance Company

54 Elo Mutual Pension Insurance Company

55 Varma Mutual Pension Insurance Company

56 Veritas Pension Insurance Company

70014 UPM Sellutehtaiden eläkesäätiö

70047 Sanoman Eläkesäätiö

70072 Sandvik Eläkesäätiö

70074 Maataloustuottajain eläkesäätiö

70076 Kontinon yhteiseläkesäätiö

70077 Eläkesäätiö Polaris Pensionsstiftelse

70078 Yleisradion eläkesäätiö

70088 ABB Eläkesäätiö

70093 L-Fashion Group Oy:n eläkesäätiö

70109 Honeywell Oy:n Henkilökunnan Eläkesäätiö

70199 Telian eläkesäätiö

70200 Yara Suomen Eläkesäätiö

70202 Orionin Eläkesäätiö

80001Valion Eläkekassa

80005 OP-Eläkekassa

80008 Eläkekassa Verso

80009 Apteekkien Eläkekassa

80014 Liikennepalvelualojen Eläkekassa Viabek

80014 Reka Eläkekassa

Pension policy number

If the income earner has earnings-related pension insurance, the payer must give the pension policy number in the earnings payment report. Do not report the pension policy number if the income earner has pension insurance under the farmers' pensions act (MYEL) or the self-employed persons' pensions act (YEL).

The pension policy number is 11 characters long and must be reported in full. If there are less than 11 characters, the required number of zeros must be added after the hyphen (e.g. 46-00123456).

3.1 Employees Pensions Act (TyEL)

According to the Employees Pensions Act, the employer is obligated to insure all of its employees between 17 and 68 years of age, whose income exceeds the threshold set for the obligation to insure (in 2019: EUR 59.36/month). The employer may also insure an employee whose income falls below the threshold. Information on earnings-related pension insurance contributions is available on the website of the Finnish Pension Alliance TELA at tela.fi. The upper age limit of the insurance obligation increases in steps. For persons born in 1957 or earlier, the upper age limit of the insurance obligation is 68 years, for persons born in 1958–61 it is 69 years, and for persons born after that it is 70 years.

The payer enters 'Employee's earnings-related pension insurance (TyEL)' as the pension insurance data on the Incomes Register's earnings payment report.

The pension insurance data is not reported, if the income earner is not insured in Finland. In such a case, the Type of exception to insurance information of the 'Other insurance details' data group that must be used is: 'Not subject to Finnish social security (earnings-related pension insurance)'. Exceptions are described in more detail in Section 6.1.

The income types of payments to be reported to the Incomes Register are described in a separate list of codes on the Documentation page, which can be used to check whether the income type concerned is subject to earnings-related pension insurance contribution by default (Yes). If the income type is subject to earnings-related pension insurance contribution, information on the earnings-related pension insurance, such as the pension policy number, must also always be reported.

3.2 Public sector pensions act

According to the public sector pensions act (julkisten alojen eläkelaki 81/2016), the employer is obligated to insure all of its employees between 17 and 68 years of age. In addition to employment and public-service employment relationships, assignments, positions of trust, and the tasks of carers and family carers are also employment relationships under the public sector pensions act. No lower wage limit (in euros) has been set in the public sector pensions act for the insurance obligation; all income earners must be insured irrespective of how much they earn and, as a result, the reporting obligation also applies to all income. The upper age limit of the insurance obligation increases in steps under the public sector pensions act in the same way it does under the Employees Pensions Act (see Section 3.1).

The payer enters 'Employee's earnings-related pension insurance' as pension insurance data on the Incomes Register's earnings payment report.

The pension insurance data is not reported, if the income earner is not insured in Finland. In such a case, the Type of exception to insurance information of the 'Insurance exceptions' data group that must be used is: 'Not subject to Finnish social security (earnings-related pension insurance)'. Exceptions are described in more detail in Section 6.2.

Although the insurance obligation usually ends at age 68, the employment relationships details and insurance details of employees aged over 68 are also reported to the Incomes Register in the following cases:

- The income earner is a minister, a member of the parliament, or a member of the European Parliament.

- The employment relationships of persons born before 1 January 1940, who are covered by the municipal pension coverage under the public sector pensions act, are entitled to pension without the 68 years age limit for as long as the employment relationship continues uninterrupted. Another condition is that the uninterrupted period of employment began before the person's 65th birthday.

The income types of payments to be reported to the Incomes Register are described in a separate list of codes on the Documentation page, which can be used to check whether the income type concerned is subject to earnings-related pension insurance contribution by default (Yes). If the income type is subject to an earnings-related pension insurance contribution, information on the data group 'Earnings-related pension insurance', such as the pension policy number, must also always be reported.

There are differences between the earnings-related pension insurance practices of the public sector pensions act and the Employees Pensions Act, for example, with regard to meeting fees, lecture fees, and positions of trust.

3.3 Self-employed person's pensions act (YEL)

A self-employed person is a person who is gainfully employed without being in an employment relationship, thus meeting the criteria for the gainful employment in question referred to in the relevant legislation. Self-employed persons are responsible for arranging their own pension insurance. Self-employed persons insure their operations under the self-employed persons' pensions act (yrittäjän eläkelaki (YEL) 1272/2006). YEL pension insurance is mandatory when the self-employed person meets the conditions of insuring referred to in the self-employed persons’ pensions act. YEL pension insurance must be taken out within six months of setting up a business. More information on the insurance obligation of self-employed persons is available in Finnish on the following website, on matters relating to earnings-related pensions legislation: tyoelakelakipalvelu.fi.

The pension provider confirms the self-employed person's earned income under YEL, which must correspond to the self-employed person's work input. The minimum limit for earned income under YEL is EUR 7,799.37 a year (in 2019) and the maximum limit is EUR 177,125 a year (in 2019). More information on the limits for pension contributions is provided on TELA's website at tela.fi.

Self-employment can also be a secondary occupation. Self-employment is a secondary occupation when the self-employed person repeatedly earns income from self-employment alongside earning an income through employment or pension. When self-employment is a secondary occupation, the self-employed person must have self-employed person’s pension insurance if their earned income under YEL is estimated to be at least above the minimum limit laid down in an act and they meet the act's criteria for a self-employed person.

If a self-employed person continues to run a business after retirement on old-age pension, they are not obligated to have YEL pension insurance. However, voluntary YEL pension insurance is also a possibility. If the self-employed person earns any income alongside retirement on old age pension, insurance must be taken out for the self-employment if the conditions of insuring are met.

The payer enters 'Pension insurance for the self-employed (YEL)' as the pension insurance data on the Incomes Register's earnings payment report.

3.4 Farmers' pensions act (MYEL)

Insurance under the farmers' pensions act (maatalousyrittäjän eläkelaki (MYEL) 1280/2006) is the earnings-related pension insurance for farmers, forest owners, fishers and reindeer breeders, and their family members. Recipients of subsidies are also insured under MYEL. The earnings-related pension insurances of Finnish farmers under MYEL are handled by the Farmers' Social Insurance Institution Mela.

When the company pays wages to an employee who is insured under the farmers' pensions act, the 'Pension insurance for farmers (MYEL)' is entered as the pension insurance data on the Incomes Register's earnings payment report. At this stage, the payer of wages does not collect any social insurance contributions from the pay. The pension insurance for farmers is obtained from Mela. In most cases, the insurance concerns the farmer's family member. If a farmer's estate or farm partnership pays wages to a shareholder insured under MYEL, the same reporting process applies to the pay.

More information on the insurance obligations of farmers is available on Mela's website at mela.fi.

Specific requirements for reporting MYEL and YEL wages

The MYEL and YEL income from work confirmed by the insurance company is the income on which pension insurance and health insurance contributions are based, and replaces the wages received by the self-employed person in determining the health insurance contribution. The pension provider reports the amounts of confirmed MYEL and YEL income to the Tax Administration on a separate report.

If wages are paid to a self-employed person insured under MYEL or YEL, the wages must be reported to the Incomes Register for the Tax Administration's use. However, the wages paid are not used for social insurance purposes.

If MYEL wages are paid to the self-employed person's family members, the wages must be reported to the Incomes Register for the Tax Administration's use.

A private trader cannot pay himself/herself or his/her spouse any tax deductible wages. The operating result of business operations is not reported to the Incomes Register, but to the Tax Administration on a business tax return.

When the payer reports earnings payment data to the Incomes Register, it is important to use the 'MYEL' or 'YEL' information. If this information is not provided on the earnings payment report, double payments may be imposed by mistake.

4 Reporting of accident and occupational disease insurance details

The employer must take out accident and occupational disease insurance for those employees who are employed by the employer in a contractual employment relationship, a public-service employment relationship, or another type of legal relationship between an employer and employee, as defined by law. The term 'employment relationship' means the type of employment relationship referred to in the Employment Contracts Act. The insurance must be taken out in advance so that the insurance is valid at the time when the employee starts the job.

The employer must take out the accident and occupational disease insurance if the total amount of earnings from work paid to all employees during the calendar year exceeds EUR 1,300 (in 2019). The limit is indexed annually and adjusted accordingly by rounding to the nearest hundred euros.

The limit applies to all payments made by the employer. All earnings from work during the calendar year paid, or agreed to be paid by the employer to employees who are in an employment relationship with the employer, must be added together. The time of payment is irrelevant.

The employer pays the insurance contribution according to the pension provider's invoices and the payment is not reported to the Incomes Register.

Unlike with pension insurance, accident and occupational disease insurance does not have any age limits and no earnings limits have been set for individual employees.

Example 5: A 15-year-old summer worker is covered by the employer's accident and occupational disease insurance and the wages paid to the summer worker (EUR 1,800) are reported as subject to accident and occupational disease insurance contribution, even though the summer worker does not have earnings-related pension insurance and the wages are therefore not subject to an earnings-related pension insurance contribution.

The example's income paid is not subject to earnings-related pension, unemployment or health insurance contributions.

The obligation to take out accident and occupational disease insurance also applies to executive-level working shareholders if their ownership percentage does not exceed the limits referred to in an act. The limits concerning employment relationships and self-employment are set in the same manner as the limits concerning earnings-related pension insurance contributions for employees and self-employed persons (see Section 3.3). The insurance obligation also applies to the shareholder's family members who work in the company under an employment relationship.

A self-employed person's family member who works for the self-employed person in the type of employment relationship referred to in the Employment Contracts Act is covered by the company's accident and occupational disease insurance if the amount of wages paid by the company exceeds the threshold set for insuring.

Self-employed persons subject to insuring under YEL do not have to take out accident and occupational disease insurance. If the self-employed person has mandatory or voluntary YEL pension insurance, they can voluntarily take out insurance for accidents and occupational diseases arising from self-employment referred to in the Workers' Compensation Act (self-employed persons' voluntary insurance for working time).

The accident and occupational disease insurance for farmers, fishermen, and reindeer breeders, as well as recipients of subsidies, are handled via the Farmers' Social Insurance Institution Mela. The farmers' accident and occupational disease insurance (MATA) is automatically valid alongside the mandatory MYEL pension insurance. If the person is not obliged to have insurance under MYEL, they nevertheless have the option of taking out MATA insurance via Mela.

Insurance company identifier and insurance policy number

The occupational accident insurance company identifier and insurance policy number of the earnings-related pension provider must be entered in the earnings payment report, if the payer has taken out more than one accident and occupational disease insurance for the employees. In other situations, the pension provider code and pension policy number are voluntarily submitted details.

5 Reporting of unemployment insurance details

The employee's and employer's unemployment insurance contributions are determined on the basis of the wages subject to unemployment insurance contribution. The unemployment insurance contributions are primarily used to finance earnings-related unemployment benefits.

The employer pays the Employment Fund a total amount which includes both the employer's unemployment insurance contribution and the employee's unemployment insurance contribution. Of these, only the employee's share is reported to the Incomes Register as an item that is deductible from pay (a separately reported income type 414). The employer's contributions are calculated based on the reported income types.

The employer is obligated to pay the unemployment insurance contribution if the total amount of wages paid to the employees during the calendar year exceeds EUR 1,300 (in 2019). The limit is indexed annually and adjusted accordingly by rounding to the nearest hundred euros. Irrespective of the payment obligation arising only after the amount of wages exceeds EUR 1,300 (in 2019), each contribution paid must be entered in the earnings payment report as payments made under the unemployment insurance contribution obligation if the other criteria for the payment obligation are met.

The limit applies to all wages that the employer has paid during the calendar year, which are subject to unemployment insurance contribution.

The employer must always withhold the employee's unemployment insurance contribution from the pay of an employee who is obligated to pay the contribution even if the total sum of wages is less than EUR 1,300. In such a case, the employer keeps the unemployment insurance contribution collected from the employee but the employee gets to deduct the contribution for tax purposes.

The payer does not withhold the employee's unemployment insurance contribution if the income earner is

- a self-employed person (self-employed persons' pension act, section 3)

- a farmer or a farmer’s family member (farmers' pensions act, sections 3–5)

- less than 17 years old (payment obligation starts at the beginning of the month following the month of the birthday)

- 65 years or older (payment obligation ends at the beginning of the month following the month of the birthday).

The obligation to pay unemployment insurance contributions is reviewed separately for each employment or public-service employment relationship. If a self-employed person, farmer or farmer's family member is employed by someone else alongside the business operations carried out as an entrepreneur, the payment obligation applies to the wages earned from that work.

Partial owners

Partial owners of a company pay a lower employee's unemployment insurance contribution than employees. The concept of 'partial owner' is defined in the unemployment security act (työttömyysturvalaki 1290/2002).

Whether a person is a partial owner or an employee is affected by the ownership share, voting power and other control of the person and their family members, as well as the person's position in the company. More information on partial ownership is available at www.tyollisyysrahasto.fi/en/

The data on partial ownership is reported to the Incomes Register under the 'Type of additional income earner data: Partial owner'.

6 Exceptions to insurance

If the income earner is not subject to Finnish social security or the payer is not obligated to insure the income earner, the situation qualifies as an exception to insurance. The Type of exception to insurance data concerns the entire report, which means that the data cannot be reported separately for an individual income type in the same manner as the Type of insurance information described in Section 1.3.

The following are examples of exceptions to insurance:

- No obligation to provide insurance (earnings-related pension, health, unemployment or accident and occupational disease insurance)

- No obligation to provide insurance (earnings-related pension insurance)

- No obligation to provide insurance (accident and occupational disease insurance)

- No obligation to provide insurance (unemployment insurance)

- No obligation to provide insurance (health insurance)

- Not subject to Finnish social security (earnings-related pension, health, unemployment or accident and occupational disease insurance)

- Not subject to Finnish social security (earnings-related pension insurance)

- Not subject to Finnish social security (accident and occupational disease insurance)

- Not subject to Finnish social security (unemployment insurance)

- Not subject to Finnish social security (health insurance)

- Voluntary insurance in Finland (earnings-related pension insurance)

The Type of exception to insurance data concerns the entire earnings payment report. This means that if a 'Not subject to Finnish social security' entry or a 'No obligation to provide insurance' entry has been included in the report, none of the income types in the report are subject to the social insurance contribution which the Type of exception to insurance concerns. Furthermore, this means that if the insurance information changes during a pay period, two separate reports must be submitted for the income earner. This has to be done if, for example, the income earner was not subject to Finnish social security at the beginning of the pay period, but becomes insured in Finland in the middle of the pay period. In such a case, the payer must submit two separate reports, providing data on the income with regard to which the income earner was not insured in Finland, and on the income paid to the income earner while they were insured in Finland.

If no Type of exception to insurance data is provided, the income earner is deemed to be insured in Finland, and the income paid to them is, as a rule, subject to social insurance contributions.

6.1 Income earner is not subject to Finnish social security

Social insurance contributions are not paid in Finland if the income earner is not subject to Finnish social security. Different social insurance contributions may be covered by different rules on who is subject to Finnish social security. If the income earner is not subject to Finnish social security, the payer reports the data on different insurances.

If the person is not subject to Finnish social security with regard to any social insurance, the payer must use the 'Not subject to Finnish social security (earnings-related pension, health, unemployment or accident and occupational disease insurance)' data.

For example, an income earner working in Finland is not subject to Finnish social security if

- the income earner is covered by another country's legislation under the EU provisions on social security and the income earner has an A1 certificate

- the income earner is covered by another country’s legislation based on a social security agreement and they have a certificate on the applicable provisions.

In certain situations, an income earner working abroad may be subject to Finnish social security if, for example, they have an A1 certificate issued by the Finnish Centre for Pensions.

These types of situations are described in more detail in the instruction Reporting data to the Incomes Register: international situations.

Example 6: A Belgian employee comes to Finland to work in the employment of a Finnish employer for eight months. The employee is paid a monthly wage of EUR 6,000. The employee has an A1 certificate, based on which he is covered by Belgian social security during his work. Because the employee is insured in the home country, no social insurance contributions need to be paid to Finland for the income that the employee earns.

The payer reports:

- Type of exception to insurance: Not subject to Finnish social security (earnings-related pension, health, unemployment or accident and occupational disease insurance)

- Social security certificate: To Finland A1 certificate. The data on the certificate concerning social security is voluntary complementary additional data.

Based on the submitted data, no social insurance contributions are determined for the employee's income in Finland.

Example 7: If the income earner is not subject to Finnish social security with regard to earnings-related pension insurance only, the information must be entered in every report in the 'Other insurance details' data group as the Type of exception to insurance 'Not subject to Finnish social security (earnings-related pension insurance)'.

In this situation, details concerning the data group 'Earnings-related pension insurance', such as the pension provider code or pension policy number, are also not reported.

6.2 No obligation to provide insurance

In certain situations, the payer is not obligated to insure the income earner, for example, due to the threshold for insuring (in euros), the income earner's age or the income earner being self-employed. In these situations, the payer reports the information 'No obligation to provide insurance' in the income earner's earnings payment report. The payer can use this information to itemise the social insurance contributions for which there is no obligation to provide insurance.

Even if the payment made falls below the threshold set for the obligation to insure, the payment must be entered as covered by unemployment insurance contribution obligation if the other conditions of the payment obligation are met. The Employment Fund determines an unemployment insurance contribution when the limit set for wages paid is exceeded.

If the income earner is not subject to earnings-related pension insurance due to their age or their income falls below the threshold for the obligation to provide insurance (earnings-related pension insurance), the payer must enter this in the report by using the Type of exception to insurance ‘No obligation to provide insurance (earnings-related pension insurance)’.

In this situation, earnings-related pension insurance information, such as the pension provider code or pension policy number, need not be reported.

The government as an employer must report the data 'No obligation to provide insurance (accident and occupational disease insurance)'

If the income paid during the month later exceeds the threshold, the payer must cancel the report they submitted and delete the 'No obligation to provide insurance' data. After this, the payer must submit a new report with the correct information. If corrections need to be made to several reports, each submitted report must be cancelled after which a new report must be submitted for each of the reports individually. In addition to the corrections, the submitter must enter the earnings-related pension insurance information in the new report, including the pension policy number.

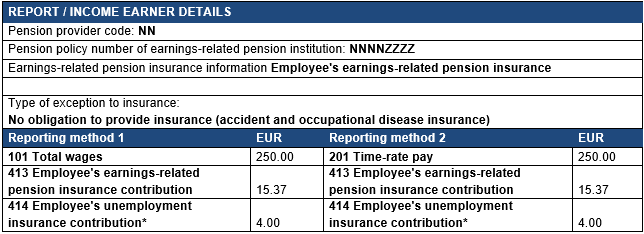

Example 8: The employer pays EUR 250 in wages to the income earner. The amount of wages paid by the employer is below the annual wage sum threshold for accident and occupational disease insurance and unemployment insurance contribution (EUR 1,300). The payer is obligated to pay the earnings-related pension contributions and health insurance contributions, as well as to withhold the employee's unemployment insurance contribution from the income earner's wages.

The payer has arranged the employee's pension provision without taking out an insurance policy; in other words, the payer is a temporary employer with regard to the earnings-related pension insurance.

The payer reports:

*The employee's unemployment insurance contribution is collected from the income earner, even if the employer did not have an obligation to pay the contribution because the employee is paid wages EUR 1,300 or less in a year. In such a case, the employer keeps the collected payment. The income earner receives the collected amount as a deduction from their own taxation. The Employment Fund will impose a payment for the employer when the wage sum threshold is exceeded.

Based on the submitted report, the paid income is deemed to be subject to earnings-related pension and health insurance contributions and the unemployment insurance contribution. However, the income is not subject to the accident and occupational disease insurance contribution.

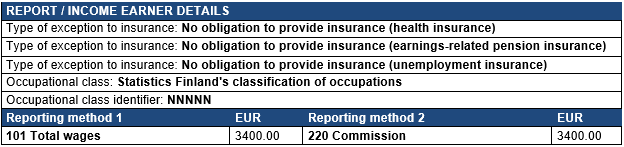

Example 9: The lower age limit for health insurance is 16 years and for earnings-related pension insurance 17 years. The obligation to provide these insurances ceases when the income earner turns 68. Correspondingly, the obligation to pay unemployment insurance contribution begins when the income earner turns 17 and ceases when they turn 65. There are no age limits for accident and occupational disease insurance.

An income earner who is 72 years old is paid EUR 3,400 as a commission. Because the income earner is older than the above-mentioned age limits for the different insurances, no social insurance contributions other than the accident and occupational disease insurance contribution are paid from the income he receives.

The payer reports:

Based on the submitted data, the income earner's income is not subject to earnings-related pension, health or unemployment insurance contributions. However, the income is subject to the accident and occupational disease insurance contribution, due to which the occupational class data must also be provided (type and identifier of the occupational class) and accident and occupational disease insurance must be taken out before starting on the job.

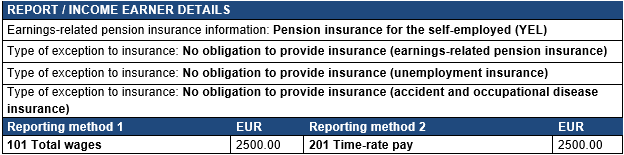

Example 10: A shareholder working for his own company withdraws EUR 1,500 in wages. The shareholder is the only shareholder in the company, and has taken out a mandatory insurance policy under the self-employed persons' pensions act (YEL).

The payer reports:

Based on the information provided, no other social insurance contributions, except for the employer's health insurance contribution, are levied from the self-employed person's wages. The self-employed person's pension insurance contribution is determined based on the confirmed income from work. Similarly, the income earner's health care and daily allowance contributions are levied based on income from work. The self-employed person can voluntarily take out insurance against occupational accidents and unemployment.

If the person is not subject to YEL pension insurance due to their business operations carried out as an entrepreneur being very small-scale operations, the information 'No obligation to provide insurance' is reported, and no earnings-related pension insurance details need to be given.

6.3 Voluntary provision of insurance in Finland

Even if the income earner is not subject to Finnish social security or the employer has no obligation to provide insurance for the income earner, the employer may take out voluntary pension insurance for the income earner. In this situation, the voluntary insurance taken out separately for the person in question is reported with the information 'Voluntary insurance in Finland (earnings-related pension insurance)' under Type of exception to insurance.

If the insurance has been taken out by the employer voluntarily, the earnings-related pension provider code and the pension policy number must be entered in the report. The ‘Voluntary insurance in Finland’ information applies to the insurance of an employee working abroad.